Key Points

- The Bank of Japan’s stimulus program is Godzilla-sized.

- The program to grow the monetary base has had little lasting success, with economic growth remaining soft.

- The policy poses a rising risk of becoming a monster that wreaks havoc on the country as the Bank of Japan becomes the biggest owner of Japanese bonds and stocks.

Godzilla Resurgence, the latest version of Japan’s King of Monsters, is the highest grossing domestic film of the year in Japan and will be released in the United States this month. Lately, sequels seem to win out over new ideas; the same could be said for central bank policies in recent years. The Bank of Japan faces a rising risk that their policy has created a monster that may be getting harder to control.

On September 21, amidst talk of “helicopter money” and an increasingly difficult to manage policy, the Bank of Japan (BOJ) announced changes to extend their long-running economic stimulus program, already by far the largest in the world as a percentage of GDP. In fact, you could say the BOJ’s stimulus program is Godzilla-sized and may begin to pose an increasing risk to investors.

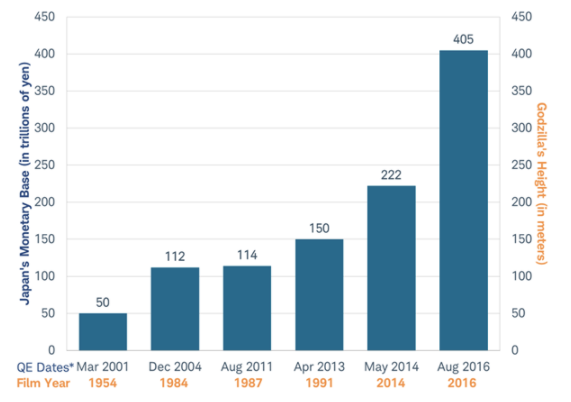

When we say Godzilla-sized, were not referring to 1954’s Godzilla—but 2016's Godzilla. As depicted in the chart below, the BOJ’s growth of Japan’s monetary base, the amount of currency directly supplied to the economy, has been proportional to the growing size of Godzilla as he appeared in various films over the past 52 years, culminating in 2016’s towering monster.

Godzilla-sized stimulus: Japan’s monetary base has grown like Godzilla over the years

Source: Charles Schwab, Bloomberg data as of 10/2/2016.

*Dates of changes in BOJ’s quantitative easing program

Monetary base is the amount of currency directly supplied to an economy.

Nearly as tall as San Francisco’s Transamerica Pyramid in the 2014 film at over 200 meters, in 2016’s incarnation Godzilla has grown to over 400 meters, or about two-thirds of the height of the tallest building in Tokyo (the Skytree at 634 meters). Godzilla’s ever increasing size mirrors the monster growth seen in Japan’s monetary base.

The making of a monster

Increasing the monetary base is intended to make more cash available, encouraging lending to drive growth and generate inflation.

The BOJ was the first central bank to enact asset purchases, now widely-referred to as QE. The first round took place in March 2001 and ended December 2004, growing the monetary base from 66 trillion to 112 trillion yen.

Although the second round came in 2010 and 2011, the monetary base did not materially expand again until April 2013, when the current QE program was implemented. Having increased the monetary base to 150 trillion yen, the BOJ announced that it would expand the program even more aggressively.

In May 2014, about a year after it began, it grew to 222 trillion yen.

In September 2016, with the monetary base at 405 trillion yen, the BOJ announced its intent to expand the monetary base until growth in core inflation “overshoots” its 2% target.

To put the monetary base in Japan in a more real-world perspective, it is equivalent in size to the monetary base in the United States, even though the U.S. economy is four times larger than the Japanese economy.

So is it working? Not really. With Japan’s aging population well past their peak borrowing and spending years, growth in Japanese bank lending has been barely 2% in the past three years despite the 35% annualized growth in the monetary base.

King of the markets

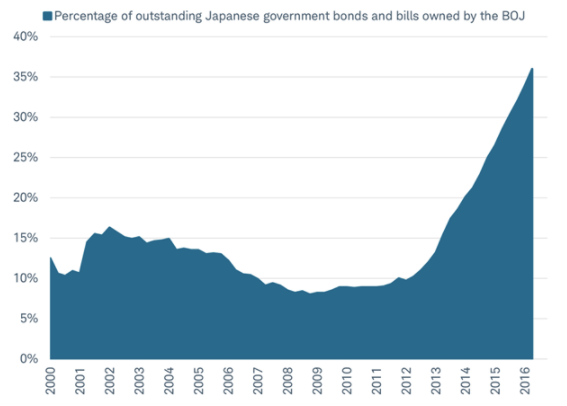

The growing monetary base seems to have had little in the way of lasting success, with growth remaining soft, but poses rising risks of becoming a monster that wreaks havoc on the country by becoming the biggest owner of Japanese bonds and stocks. A sign of the growing danger can be seen in that more than one-third of all Japanese government debt is now owned by the Bank of Japan—having gone from about 10% to 35% in just the past four years.

Bank of Japan is buying up Japanese government bonds at a rapid pace

Source: Charles Schwab, Bloomberg data as of 9/29/2016.

At the current pace, the BOJ could own more than half of all Japanese government bonds and run out of bonds to buy from banks by the end of 2017. Addressing the scarcity issue, the BOJ announced a change to the program, in late September. Purchasing will be determined by whatever amount is necessary to stabilize longer-term bond yields around zero, rather than buy a preset amount each month.

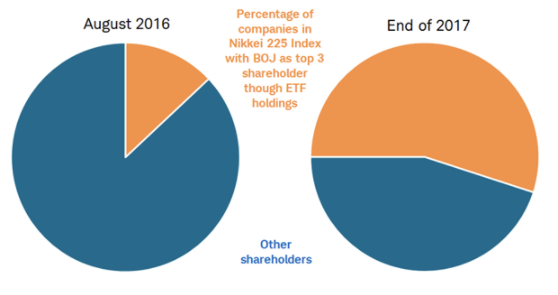

The BOJ is also buying stocks, and is on track to become the largest stockholder in the world’s third largest stock market. The BOJ doesn’t acquire shares of companies directly, rather it buys them through Exchange Traded Funds (ETFs). Estimates of the underlying stock holdings of the ETFs owned by the BOJ reveal that the central bank is among the top three holders of more than 10% of Japanese stocks. By the end of 2017, the BOJ will be a top shareholder of more than half of all Japanese companies in the Nikkei 225 Index, according to Bloomberg.

Bank of Japan on track to become a top shareholder in more than half of Japanese stocks

Source: Bloomberg, data as of 8/14/2016.

The Bank of Japan increasingly risks becoming a “king of the markets,” the ultimate owner of most of the government bonds and corporate stocks in the country. This could pose several risks:

- Trading in Japanese government bonds has plunged, raising questions about the functional limits of QE.

- Market volatility may rise as the assets owned by the private sector decline. Companies that have a smaller percent of shares available to the public have historically tended to be more volatile.

- If, in the future, the BOJ chooses to promote social or economic goals and not simply act as a passive investor, sudden changes that could take place at companies may not be in the interests of other shareholders.

The upside for investors may seem to be the enormous buying that could push up asset prices. But, despite all the buying of Japanese stocks by the BOJ this year, it has not been a blockbuster year. In fact, Japan’s Nikkei 225 Index has posted a 4.5% total return for 2016 through the end of September, measured in U.S. dollars. This return lagged both the U.S. S&P 500 and broad MSCI All-Country World Index by about 2 percentage points. This is no surprise, since the Japanese stock market has behaved like the global financial sector, as discussed in the recent commentary Your portfolio may be less diversified than you think. Changes in interest rates have been a far more potent factor driving Japanese stocks than BOJ buying, at least so far.

Another sequel

The BOJ is delivering yet another sequel to their long-running stimulus program with little hope of successfully boosting long-term growth or inflation. Japan’s growth solution is more people, not more policy. Japan’s GDP for the past 10 years has been less than 1% a year, second only to Italy as the worst among the Group of Seven (G7) countries (United States, United Kingdom, Canada, Germany, France, Italy, and Japan). At first glance, it appears that the BOJ desperately needs to do something to drive greater growth. But GDP per worker in Japan is the second best of the G7, higher than Germany and second only to the United States. In Japan, it’s the demographic decline in workers that is limiting growth. The BOJ’s policy of expanding the monetary base has been a poor substitute for a shrinking number of people and poses an increasing risk to the markets.