For many advisors, growing a financial planning business generally means increasing their assets under management. In a study of 803 financial advisors, the No. 1 concern cited by 91% of them was that they grow their asset base. This often entails focusing their efforts on cultivating wealthy clients. Nearly nine out of 10 of the advisors surveyed identified affluent investors as their preferred clients. Moreover, 78% said they are very interested in working with the super-rich (those with a net worth of $500 million or more).

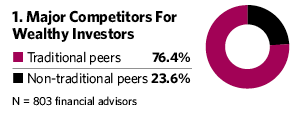

Complicating the matter is that 88% of those surveyed reported an intense competition for wealthy investors (Figure 1). About three-quarters cited their traditional peers as prime competitors while the remainder pointed to non-traditional rivals such as robo-advisors and accounting firms.

Clearly, many financial advisors are tending to focus their efforts on cultivating affluent investors, which makes it a very competitive environment. At the same time, the principal approach financial advisors are taking to capture discretionary assets is highlighting their investment management capabilities. While this approach is going to continue to dominate the industry, there are less direct ways of increasing assets under management. Specifically, there are a variety of advanced planning strategies in which investment expertise is “built in.”

Advanced Planning

Investment management is quite important to wealthy investors, but they also want to blunt the impact of taxes and be protected from frivolous lawsuits. Advanced planning is a collection of interconnected services and products, many of which result in lowering the tax burden of the wealthy.

These approaches skillfully meld an advisor’s legal, regulatory and financial expertise in order to enhance and safeguard an individual’s or a family’s net worth. It means you provide one or more of the following three (often interconnected) services:

• Wealth enhancement is the process of using advanced planning strategies to relieve the client’s tax burden and thus foster greater wealth creation. With investment income, for example, the ideal is to change income into short-term capital gains, then into long-term capital gains, then into tax deferral and ultimately into no taxes whatsoever.

• Estate planning is the process of legally structuring the future disposition of current and projected assets. Included here are the various charitable solutions affluent investors can use to address taxes while making significant gifts to non-profits.

• Asset protection planning is the process of employing risk management products and advanced planning strategies to ensure an affluent investor’s wealth is not unjustly taken.

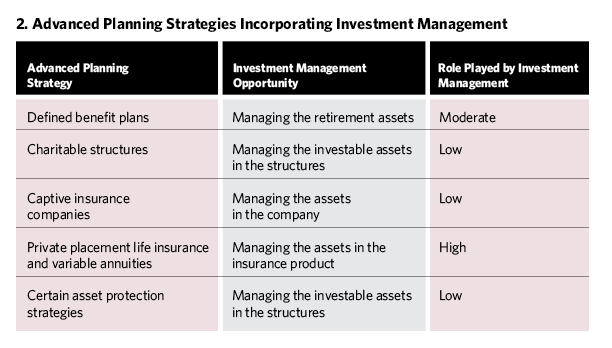

Investment management, while not the ultimate goal, is an integral component of these strategies. Consequently, when an affluent investor adopts them, the advisor will often be given additional assets to manage. Let’s consider a few examples of these different approaches (Figure 2):

• Defined benefit plans can include meaningful tax deductions and a platform where the investable assets grow tax deferred. Some of these plans allow wealthy business owners to garner most of the monies.

• Charitable structures are tax-efficient ways to benefit worthy causes. The monies used to fund charitable trusts and foundations can be professionally managed.

• Captive insurance companies are used to address certain corporate risks. The premium dollars not used to pay claims can be managed and tend to grow over time.

• Private placement life insurance and private placement variable annuities are ways to eliminate most or all of the taxes involved in an investment portfolio. This is an explicit combination of advanced planning and investment management.

• Certain asset protection strategies have money management components that are a distant second in importance to wealth protection. One known as “floating islands” almost always requires that the funds be professionally managed.

There are a number of other advanced planning strategies where investment management plays an integral role. But except for a few of them (such as captive insurance companies) the money management component is considered a distant second in importance.