With the Federal Reserve suppressing interest rates through successive rounds of quantitative easing, clients and advisors have been searching for yield-bearing investments for years.

In addition to looking for interest income, clients are concerned about the long-term effect of inflation that may be caused by the Fed printing new money. In many cases, investors reach for yield in more risky assets and overlook another form of inflation protection -- Treasury Inflation-Protected Securities (TIPS). They are being overlooked because they currently offer negative nominal yields.

Recently I was constructing a laddered bond portfolio for a client who was concerned about preserving his spending power. Naturally I thought of purchasing TIPS for those "rungs" of the ladder, but as I examined them more closely, one glaring question came to mind: Can I really recommend bonds with negative yields?

Knowing that I could face resistance to such a recommendation, I dove deeper into the relationship between TIPS and nominal Treasurys. My research led me to the conclusion that it does make sense to recommend TIPS despite their negative advertised yield. Here's how I explained this concept and presented it to my client.

TIPS are an inflation-indexed bond offered by the Treasury. Their principal value increases without limit every six months in line with changes in the Consumer Price Index (CPI). The bond's coupon rate of interest doesn't change, but as the principal grows it causes the amount of interest paid to the investor to increase. When the security matures, the U.S. Treasury pays the original or adjusted principal, whichever is greater.

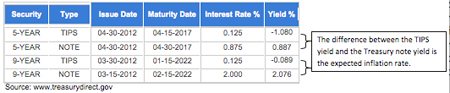

When we look at the -1.080 percent TIPS yield in the chart below, it is expressed as a real return, meaning that inflation has already been factored in. On the other hand, the real return on the 5-year Treasury note is determined by subtracting the inflation rate from the 0.887% nominal yield.

To understand the value of a negative TIPS yield, we have to look at the expected inflation rate. The expected inflation rate is determined by calculating the difference between the TIPS and Treasury note yields. In the examples above you see that the expected inflation rate at the time of the 5-year issues was 1.967 percent (0.887 percent -(-1.08 percent)=1.967 percent). If inflation comes in exactly as expected, the Treasury note will have a real yield of -1.080 percent.

That means that if inflation is higher than expected over the next five years, the Treasury note will have a real return less than 1.967 percent, making TIPS the favorable investment choice. When inflation is higher than expected, TIPS receive an upward adjustment to their value, which is what preserves the purchasing power of the principle. Alternatively, nominal Treasury notes would be preferred when inflation is expected to fall short of expectations.

With the monetary policy stimulus packages the Fed has put in place since 2008, it doesn't seem outrageous to think that inflation could exceed 1.967 percent over the next five years, or 2.165 percent over the next 10 years. Because of this, I help my clients understand how TIPS can be a useful tool to protect against inflation, despite their negative yields.

Matthew Moses is a Certified Financial Planner professional with StanCorp Investment Advisers in Ann Arbor, Mich. Throughout his career, his area of focus has been high-net-worth clients with complex planning needs.