What should the U.S. government do to fight recessions? What should it do to fight slow growth? This is the eternal question of so-called countercyclical policy. The two mainstream ideas are fiscal and monetary stimulus. The fiscal version works by having the government borrow and spend money, either on useful things like infrastructure, or by simply mailing people checks. The typical monetary variety works by having the Federal Reserve swap money for financial assets, which lowers interest rates.

Unfortunately, both of these methods have major drawbacks. Fiscal stimulus is dependent on Congress, which these days doesn't tend to respond in a rapid, reliable or even a responsible way. Monetary stimulus just doesn’t seem to work very well when interest rates are near zero -- the impact of quantitative easing, for example, was questionable.

Because of these limitations, macroeconomists have been trying to dream up alternate ways of stimulating the economy. One of these ideas is the so-called helicopter drop -- have the central bank print money and give it to people. A second idea is to make interest rates very negative, which would probably require forcing people to use electronic money rather than physical cash.

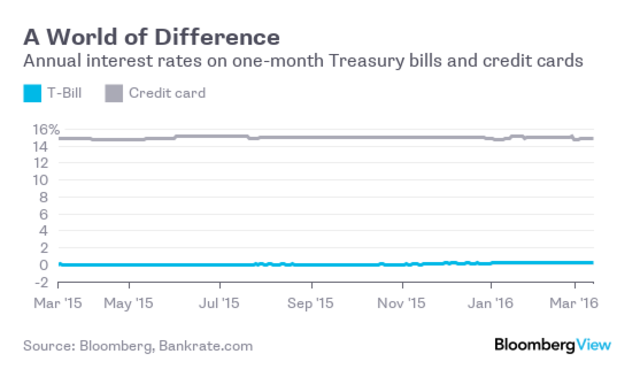

A third new idea is to have the government lend people money at very low interest rates. The basic reasoning is that people have constraints on how much they can borrow -- not everyone can get a mortgage, or take out a large loan on a credit card. This creates limits on how much they can spend. The government, on the other hand, can borrow almost unlimited money, at far lower interest rates than normal people. The interest rate on one-month Treasury bills is just a bit more than 0.25 percent, while credit-card interest rates are about 15 percent:

Suppose the government offers loans to citizens at 0.5 percent, up to some maximum amount per-person. If people repay the loans, the government makes a profit. If they don’t, the amount they don’t pay back acts as fiscal stimulus. Either way, people will tend to spend the money they borrow, giving a bump to aggregate demand in the short term. Because some people will pay back their loans, the cost to the government -- and thus to the future taxpayer -- is lower than for pure fiscal stimulus.

This approach was suggested by University of Michigan economist Miles Kimball, in a 2011 paper entitled “Getting the Biggest Bang for the Buck in Fiscal Policy.” He called the proposal “national lines of credit.” More recently, it has been suggested by the University of California-Berkeley’s Brad DeLong, under the name of “social credit.”

Now, some research suggests that the U.S. government may have already done a version of this during the Great Recession, and that it helped fight the slump. In a conference paper entitled “Credit Policy as Fiscal Policy,” Massachusetts Institute of Technology finance professor Deborah Lucas documents more than 150 programs that the government used to lend to or encourage lending to consumers. Here, from Lucas’ paper, is a picture of total nonemergency federal loans, including direct loans and guarantees:

Lucas calculates the impact of these loans on aggregate demand, using standard estimates of fiscal multipliers. She finds that federal lending did as much as the American Recovery and Reinvestment Act of 2009 to stimulate demand and keep the economy from crashing during those dark years.