Key Points

• So far, 2016 has been a year that has frustrated both the bulls and the bears.

• Last week’s Brexit vote is likely to cause additional near-term volatility, but shouldn’t derail the U.S. equity bull market.

• Equity gains are likely to be modest compared to the post-recession pace, but we expect prices to move unevenly higher.

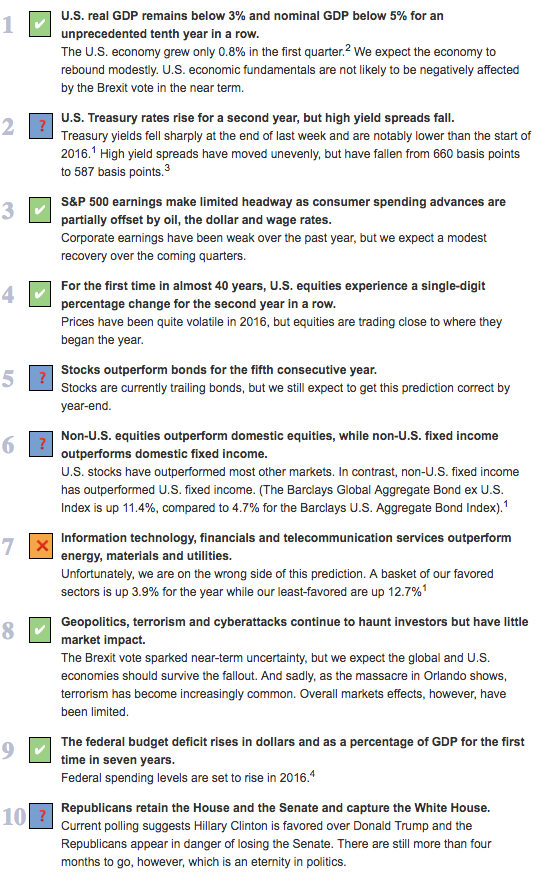

In January, we described 2016 as a year that would likely frustrate both the bulls and the bears. At the halfway point, that has certainly come to pass. We have already seen a double-digit decline in U.S. equities followed by a double-digit recovery.1 And stock prices remain uneven as investors focus on uncertain Federal Reserve policy, mixed economic and earnings data and, most recently, the political and financial turmoil following the Brexit vote.1 We forecasted equity prices would be volatile in both directions but would end the year close to where they began. With six months to go, the predictions we made at the beginning of the year are mostly on track:

Looking Ahead

Equities are no longer as cheap as they once were. But we think valuations are reasonable, especially compared to bonds and cash. We expect the global economy to improve unevenly, which should help corporate earnings recover. If this occurs, equities should be able to move unevenly higher. The pace of gains, however, is likely to be slower than what investors experienced during the first six years of this bull market. Within the equity market, we prefer mid-cycle cyclicals, companies that can generate positive free cash flow and those with higher levels of domestic earnings.

Bob Doll is chief equity strategist at Nuveen Asset Management.