The 15-year history of the Arbitrage Fund illustrates that merger arbitrage can be an all-weather strategy with a low correlation to the stock and bond markets and a low volatility port during market storms. At the same time, its comparatively sedate returns also make it something of a dark horse when the stock market is galloping ahead.

The Arbitrage Fund is one of a handful of funds that seek to profit from capturing the difference, or spread, between the price of a target company’s stock after the announcement of an acquisition and the acquiring company’s offer. The strategy follows well-documented patterns that show a target’s stock price will jump on the announcement of an acquisition, since the acquirer offers a premium over the prevailing market value to sweeten the deal. But it won’t rise to the full offer because the transaction could hit a snag before it’s completed and fall through.

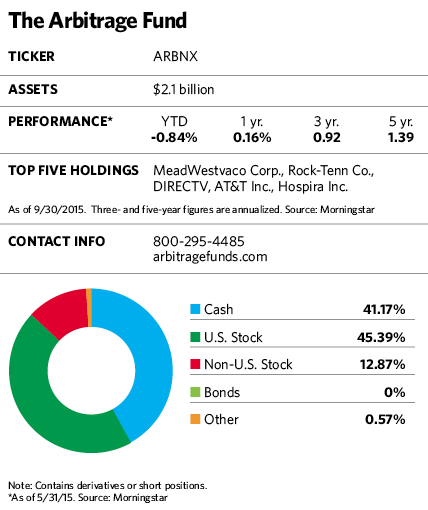

Although the strategy may sound complex and risky, the risk-return profile for the Arbitrage Fund is fairly conservative. Since its inception in the year 2000, the calendar year returns for the fund have fluctuated in a narrow band, from a low of negative 0.63% in 2008 to a high of 15% in 2003. There were only two years of negative returns, and both were less than 1% drops. The fund’s three-year standard deviation is a modest 2.6%, and it has a 0.20 correlation to the S&P 500 Index and a 0.06 correlation to the Barclays U.S. Aggregate Bond Index.

Although the strategy may sound complex and risky, the risk-return profile for the Arbitrage Fund is fairly conservative. Since its inception in the year 2000, the calendar year returns for the fund have fluctuated in a narrow band, from a low of negative 0.63% in 2008 to a high of 15% in 2003. There were only two years of negative returns, and both were less than 1% drops. The fund’s three-year standard deviation is a modest 2.6%, and it has a 0.20 correlation to the S&P 500 Index and a 0.06 correlation to the Barclays U.S. Aggregate Bond Index.

The fund was a small niche offering during its first eight years, when the bull market made its returns look modest by comparison. But by 2009, assets in the fund had quadrupled to $1 billion as investors migrated to safer investment pastures, and it now stands at $2 billion.

“In times of turmoil, people really start to appreciate what we offer,” says Roger Foltynowicz, who manages the fund with Todd Munn and John Orrico at Water Island Capital, a New York City-based investment advisor that oversees a total of $3.3 billion, including the $2 billion in the Arbitrage Fund. “They know we put capital preservation first, and that we won’t be cowboys with their money.”

Because of its low correlation to the stock markets, some of the fund’s investors use it in the alternative investments sleeve of their portfolios. Others see it as a fixed-income substitute because of its low volatility and decent, if not spectacular, returns. (As a rule, unlevered merger arbitrage investors have traditionally sought to capture returns of two to three times the risk-free rate of 90-day Treasury bills, although that can vary widely from year to year.)

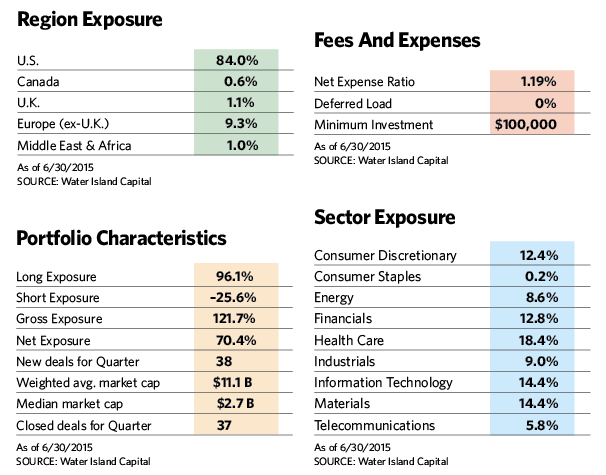

Most of the last five years have not been accommodating for merger arbitrage practitioners. Many companies seemed more interested in using cash to buy back stock or raise dividends than to expand through acquisitions, and light M&A deal calendars limited investment opportunities. Merger arbitrage returns were well below those generated by U.S. stock or bond indices. The Arbitrage Fund’s expense ratio of 1.19% for institutional class shares, while low for a fund of its type, still puts a big dent in returns when internal investments are generating razor-thin profits. And because the average deal plays out in three to four months, the fund’s portfolio turnover is high, creating a high level of taxable distributions for taxable accounts.

But the managers believe the benefits of merger arbitrage could come into clearer focus for investors as the bull market starts to show its age and market turbulence sets in. As for bonds, investors may come to see them as a less-than-sedate investment if interest rates rise and prices fall. By contrast, history shows that merger arbitrage strategies tend to do well compared with stocks when bear markets set in; and unlike bonds, which lose value when interest rates rise, arbitrage strategy returns follow the upward march of interest rates.

But the managers believe the benefits of merger arbitrage could come into clearer focus for investors as the bull market starts to show its age and market turbulence sets in. As for bonds, investors may come to see them as a less-than-sedate investment if interest rates rise and prices fall. By contrast, history shows that merger arbitrage strategies tend to do well compared with stocks when bear markets set in; and unlike bonds, which lose value when interest rates rise, arbitrage strategy returns follow the upward march of interest rates.

“Rising rates are a headwind for bond funds,” says Foltynowicz. “For us, they’re a tailwind.”

A number of other trends point to the possibility of better days ahead. The lackluster environment for merger arbitrage is beginning to change as more deals come to market. Shareholder activists, who once pushed for buybacks and dividend hikes, are increasingly pressing boards to elevate growth and shareholder value through acquisitions. Companies that have been hoarding cash may finally decide it’s time to go into growth mode, and acquisitions are a quick way to do that. A number of sectors, such as banks, technology and utilities, are still in the early stages of consolidation, and activity in the energy sector could perk up as large, healthy companies buy up smaller ones that have been socked by low commodity prices. And the healthier environment for M&A has generated more competing bids for companies, which could help boost returns for merger arbitrage transactions.

A Port In Market Storms

November 2, 2015

« Previous Article

| Next Article »

Login in order to post a comment