What a difference a few years make.

In July 2008, the world was on the verge of a financial meltdown that would have a significant impact not only on the portfolios that independent registered investment advisors managed but also on their own revenues. Three years later, the stock market is almost back to where it was, and so are most RIAs-in fact, many are now in better shape. Having nurtured client relationships and built important efficiencies into their businesses during the downturn, RIAs have established an excellent foundation for growth.

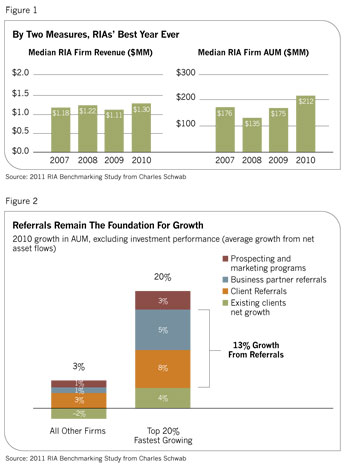

Some of that growth is already here. The newly released 2011 RIA Benchmarking Study from Charles Schwab1 shows the typical RIA in the study had revenue grow 18% last year, to $1.30 million, and assets under management (AUM) jumped 16% to $212 million (see Figure 1).

The 2010 revenue and AUM numbers are both the highest since the study began, and in many ways they show the RIA model is winning in the marketplace. It's a model that offers high-net-worth investors a level of support they can't get through more traditional models of financial advice. Where wirehouse advisors often still have an incentive to sell products with their institutions' names on them, this isn't the case with RIAs. The RIAs' open architecture environment-the model's most visible differentiator-means advisors can freely offer the products that suit their clients' needs. This is good for clients, and is one of the things (along with the transparent fee structure) that gives clients confidence that they and their advisors are in it together.

But open architecture isn't the only factor driving more business toward RIAs. Former wirehouse clients who have defected to RIA firms have done so because they think they will end up getting better treatment. Two-thirds of clients who made the wirehouse-to-RIA switch in 2010 did so because they thought they would get more personal, customized advice; 58% said they had lost trust in the full-service brokerages that had served them in the past. In light of the turmoil in 2008, it's no wonder that clients are looking for more guidance and a trusted partner.

For the RIA, 2010 was also a story about reaping the rewards of renewed discipline. By making their practices more efficient during the financial crisis of 2008 and 2009, RIAs saw profits rebound in 2010. Average operating income rose to 18.3% of revenue from 14.9% in 2009, while typical profits surged 45%. Income per principal (the total of base salary, bonus and firm profits) for the median firm was $325,000, an 18% jump from 2009.

The discipline that propelled these results was clear in two major areas and says a lot about what RIAs have done in the last few years to make themselves successful-and more important, what they must continue to do.

Strong Bonds Lead To Growth

Starting in late 2008, RIAs focused on keeping clients for the next 15 months, making sure they talked frequently with (and listened to) their clients, reassured them and closely managed their portfolios. During this time, RIAs were focused on doing the core things that had won them business in the first place.

Today, clients rely on their advisors to provide them with a basic understanding of markets, their particular investments and their options. With retirement a key concern, clients are looking for investment advice and products that will help them regain past losses. RIAs have always made a point of doing all this, but the best ones have devoted even more time to client service in the last year and a half, reaching out to proactively answer questions that clients might have.

The time RIAs spend working on clients' retirement plans or helping them calculate what they can contribute to their grandchildren's college educations may not contribute to the bottom line. But this attention is an important part of what keeps clients loyal. In the case of RIAs, it worked quite well. On average, RIAs slowed client attrition by 25% versus the previous year, holding on to 97% of their clients during 2010. In fact, the fastest growing 20% of firms in net asset flows are growing 13% annually solely from referrals. (See Figure 2.)

Operational Discipline Cost Management

The second area of discipline that helped RIAs in 2010 involved internal operations. RIAs made tougher decisions starting in 2009, including doing some downsizing. In other cases, rather than downsize, principals lowered their own bonuses and compensation. When things were at their worst, some principals went without any compensation at all, doing what they needed to do to pay, and keep, their people.

It is amazing how much engagement and loyalty this can engender both in employees and clients. Employees see that a firm values their livelihoods; clients see that a firm is not making organizational changes at the expense of client service. This kind of long-term commitment gets everyone fired up for a recovery. Cost-saving moves like these helped reduce staffing-related expenses at the average RIA firm to 61.8% of revenue in 2010 from 64.7% a year earlier. In a belt-tightening environment, advisors found new ways to do work more efficiently. It's those new, more efficient work styles that are serving firms well during the recovery.

Technology

To improve their operational efficiency in 2010, advisors also made better use of technology, and did more outsourcing to reduce the time they spent on non-value-added activities and to increase their time with both prospects and clients. In fact, adoption of technology rose sharply in 2010. The average firm now uses 5.4 of the eight common systems in their office, up from 4.2 just three years ago.

Core technologies like portfolio management and customer relationship management (CRM) were both in place at more than four in every five RIA firms. In just one year, firms went from using 4.9 to 5.3 important features in a CRM, an 8% increase. In order to improve communications with clients, RIAs focused on developing Web sites where clients could access data. Forty-eight percent of RIAs were doing that by the end of the year, versus 41% who were doing it when 2010 started. That enabled firms to plow more time into business development.

Regulations

Adapting to regulatory changes will be an opportunity for advisors. With the Dodd-Frank Wall Street Reform and Consumer Protection Act, the Securities and Exchange Commission (SEC) will be issuing new regulations. Understanding the new rules and ensuring that a firm has the people in place to manage and follow the rules will undoubtedly require more time and expense. Twenty-one percent of RIAs say that compliance requirements have created a barrier to growth for them and expect this concern to become more prevalent in the next few years.

Outsourcing

Outsourcing was another way that RIAs boosted their productivity in 2010; RIAs were far more aggressive about outsourcing certain functions. They learned that if an outside firm can take over certain functions that don't interfere with client service, and save them money in the process, it can be more efficient. For RIAs, data management, performance reporting and invoicing all fall into this category, increasing 40% over the previous year. The availability of outsourcing options is one of the clearest signs that the RIA industry is evolving in a fundamental way.

Emerging RIA 'Ecosystem'

All around us, a new ecosystem is evolving to serve independent advisors. It's important to keep in mind that one of the advantages wirehouses have had in the past has been their access to highly sophisticated products, services and advice. Up until 2008 or so, a full-service wirehouse could have made the case that it offered a better assortment of products to a high-net-worth client (even if products in the platform bore the wirehouse's brand name), better tax advice, better risk management, and so on. That claim is no longer so easy to defend.

Nowadays, there are companies that offer alternative products, including hedge fund and private equity investments, to independent advisors. There are turnkey asset management programs, which independent advisors can turn to for research, portfolio construction, rebalancing, tax optimization and the like.

Many of these companies have come into being with the sole purpose of serving independent advisors. Their very existence testifies to the fact that independent financial advice has grown from a cottage business to an industry in its own right.

Today, advisors who leave the wirehouse world for independence have more options than ever. Pure independence still remains the first choice for most. There are consolidators that can pool advisors' revenue to companies that provide a platform consisting of product, consulting and technology, allowing an advisor to concentrate on his or her client-facing work.

To be sure, the emergence of an ecosystem doesn't eliminate the very real challenges that RIAs face. Most RIA firms, for instance, are finding ways to do more with less. Despite the record revenue and AUM numbers in 2010, average revenue per client at the median firm ($7,300) was down 13% from the 2007 peak. This may be a sign that RIAs need to be slightly more selective about what they do for which clients.

Organizational issues also challenge many RIAs. Nearly seven in ten firms in the study were concerned about staffing and resources for business development. This is not surprising, considering that most RIA firms were started by an individual rainmaker or visionary. These founders are usually very adept at sales and very knowledgeable in the field of financial advice but may well be bootstrapping the operation-playing at least some role in managing the books, collecting the fees, laying out the processes and overseeing technology. So it's no wonder that one of the biggest problems (cited by 52% of the participants) is finding time for business development. Other resource-related problems include obstacles to developing and following a well-thought-out marketing strategy (cited by 39%), identifying new prospects (34%), making sufficient financial investment in marketing (32%) and maintaining accountability for business development (24%).

Moving To The Future

Where does all this net out for RIAs? They have great reason to be optimistic, for sure, but also have a few things to work on. There are four traits that will distinguish successful RIAs in the future.

They will have a succession plan in place. The average RIA is in his or her mid to late 50s. Having a clear succession plan is critical to staff recruitment, client development and client retention. Of those advisors surveyed, four out of ten do not have a succession plan in place. This is not a dental practice model, where you close the door one day and you've exhausted the revenue stream. Principals need to be clear about what will happen to, and within, their practice after it stops being their full-time job.

They will continue to organize their operations for maximum firm efficiency. There are a number of steps that RIA firms can take to ensure that they are using staff and principal time in the most efficient way possible. Segmenting an RIA client base is a good starting point for managing client profitability and giving the best clients the attention they deserve. Clients with higher levels of investable assets generally require more time, but the differences in demand are small, underscoring how much more profitable big clients are.

They will have a solid strategic plan in place. Well under half of the RIA firms in our study have a strategic plan, and 36% have no strategic planning process at all, written or otherwise. This prevents a firm as a whole from building up expertise or capabilities in clearly defined areas, and makes it likelier that the firm's fortunes will be determined by external factors and will depend on the efforts of a few individual rainmakers. An analysis of the best-managed firms3 shows they follow a more rigorous approach to strategic planning-integrating outside resources-using longer time horizons and circling back more often to see how they are doing versus plan.

They will be prepared to operate in a dynamic regulatory environment. In an industry where trust and reputation are paramount, falling short can have long-term consequences, so it's essential that RIAs stay abreast of forthcoming regulations. Those who have an approach to doing so will be able to devote less time to defending their reputations and more time helping clients, which is what we're all in business for in the first place.

Independent financial advice, while still a young industry in many ways, has broken through the skepticism of its early days and is entering another phase. The RIAs who stay focused on their clients, improve their operational discipline, and understand how to survive in a new regulatory environment will have an excellent foundation for growth in 2011 and beyond.

Bernie Clark is the executive vice president and head of Schwab Advisor Services, a leading provider of custodial, operational and trading support for approximately 6,000 investment advisory firms.

Information provided is for general informational purposes only.

Schwab Advisor Services serves independent investment advisors and includes the custody, trading and support services of Charles Schwab & Co., Inc. Member SIPC.

Independent investment advisors are not owned, affiliated with or supervised by Schwab.

(0711-3688)

1. All stats in this article are based on the 2011 RIA Benchmarking Study from Charles Schwab unless otherwise noted.

2. 2011 Schwab Independent Advisor Outlook Study

3. The RIA Benchmarking Study from Charles Schwab comprises self-reported data from advisory firms that custody their assets with Charles Schwab. The top 20% is calculated after removing those with less than $1 million in revenue. "Best-managed firms" are defined as the top 20% of independent, fee-based advisory firms in the study based on a composite score of firm growth, profitability and productivity.