If mutual fund flows are any indication, active management is facing serious headwinds. Between 2007 and 2014, equity index mutual funds and ETFs received $1 trillion in net new cash, according to the Investment Company Institute, while actively managed stock funds experienced net outflows of $659 billion.

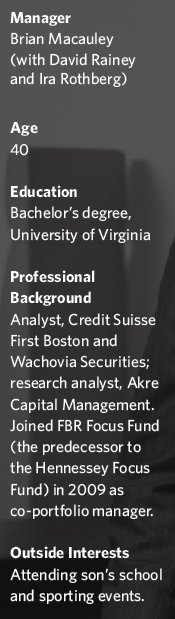

Brian Macauley, who co-manages the Hennessy Focus Fund with David Rainey and Ira Rothberg, believes that with the right management, mutual funds can generate long-term returns in excess of their passive benchmarks. At the same time, he sees the trend toward indexing as a response to the shortfalls of traditional actively managed funds. “Most of them hug a benchmark, over-diversify and underperform over the long term,” he says.

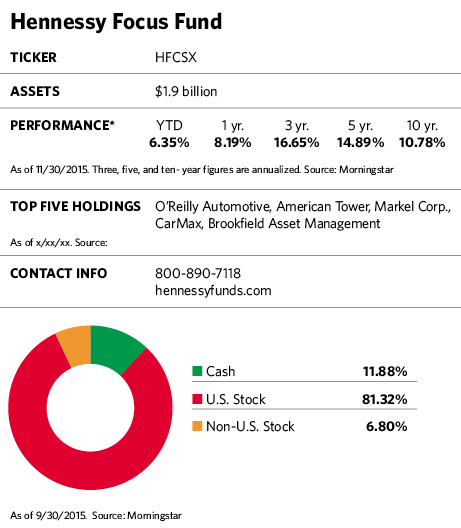

None of those descriptions even remotely applies to Hennessy Focus. As a concentrated “best picks” offering, it usually holds between 20 and 30 stocks, with approximately 60% to 80% of assets in the top 10 holdings. By comparison, the average fund in Morningstar’s mid-cap growth category holds 70 to 85 stocks and has 20% to 25% of assets in the top 10.

Hennessy’s high-conviction ideas also tend to stay in the portfolio for at least five years, and often longer. And both its sector weightings and stock picks deviate significantly from its mid-cap benchmark, the Russell 3000 Index.

Being benchmark-agnostic often means deviating from market performance. Generally, the fund’s performance relative to the benchmark has been better during times of economic and market distress because of the fund’s focus on higher-quality companies, but the performance has been slightly worse when an expanding economy provides a tailwind for a broad swath of companies, regardless of quality. Over the last five years, the portfolio has captured 93% of the market’s upside return, while experiencing only 71% of the downside loss.

While the fund has underperformed over short periods, its longer-term returns shine. From its inception in 1997 through September 30, 2015, it produced an average annual total return of 13.4%, outperforming both the Russell 3000 Index and the Russell Midcap Growth Index by over 500 basis points, annualized. Macauley stops short of predicting whether the fund will beat the indexes in 2016, but does make the modest observation that in an environment of low inflation and slow economic growth, his portfolio companies “should do pretty well.” As for the market as a whole, he believes stocks are neither overvalued nor undervalued at current levels.

He attributes much of the fund’s long-term track record to its managers’ complete familiarity with every stock in the portfolio. “It’s hard to run a fund with 100 or 150 stocks and have insight into every one of them,” he says. “Mutual funds that outperform tend to have concentrated portfolios.”

According to a white paper from the firm, titled “Unconventional Wisdom,” several studies have shown that so-called “best ideas” mutual funds focusing on a maximum of 25 stocks tend to perform better than their more diversified counterparts over the long term, yet do not have higher risk profiles. But the paper also warned that “since ‘best ideas’ tend to be smaller and less liquid, concentrated portfolios may be less nimble. Therefore, investors should plan to hold focused funds for longer periods of time.”

They should also be prepared for times when a “hot” sector that the fund is not invested in moves ahead and the fund falls behind.

Macauley says some financial advisors use his fund as “an alpha generating satellite around passive core holdings.” Others use it in conjunction with a handful of other focus funds run by skilled managers with strong track records. Since holdings among these types of funds rarely overlap, using several is a way to replace a highly diversified core equity fund, he says.

Making The Cut

In the Hennessy Focus Fund, the managers look for small and mid-cap growth businesses that are likely to grow earnings per share and cash flow at a rate at least in the mid-teen percentage area and that are selling at attractive valuations. The companies must also have a strong competitive niche, offer compensation incentives that benefit both their managements and shareholders and operate in industries with growth potential.

“We are also thoughtful about avoiding disasters,” says Macauley. “That means avoiding companies with too much leverage, that depend on some fad or fashion, that are hard to understand, or that carry regulation or litigation risk.”

Unlike many funds, this one doesn’t “trade around” positions by selling portfolio stocks when their price is high and buying them back in the future at a lower cost. Macauley says that strategy, which generates trading costs and tax liabilities, “isn’t worth the possibility of picking up a few extra basis points. The majority of our returns have come from a handful of businesses we’ve held for a long time.”

But the managers will sell when the original premise for investing is fading. That happened in late 2014 when it exited a long-held position in T. Rowe Price as the migration from active to passive investing began taking a toll on the company’s business. “This is an outstanding, well-run organization with great management,” he says. “But the headwinds from the move to passive investing aren’t going to dissipate.”

Stocks in the fund often start out with a small weighting of 3% of assets. The managers might do this because they want to move in slowly or because a company is very small and the fund cannot accommodate a larger allocation. A stock might have a medium-level weighting of 3% to 6% if the fund has a high level of confidence in the company’s long-term business prospects and the stock is reasonably priced. The largest weightings, 6% or more of fund assets, are reserved for the highest conviction picks in terms of price and prospects. These large weightings typically compose more than half of portfolio assets.

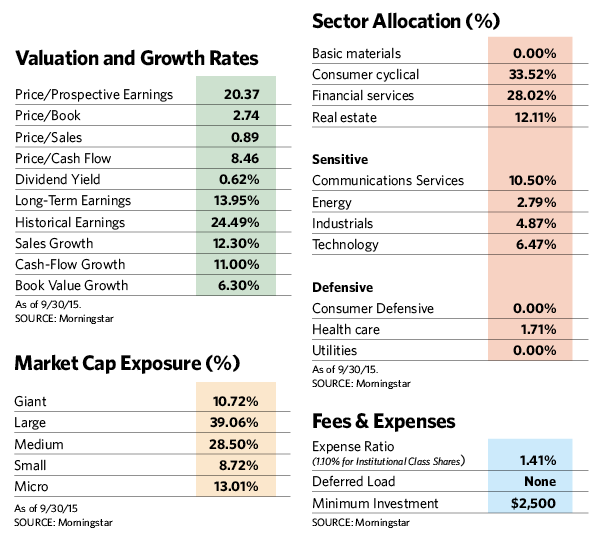

Sector weightings also deviate substantially from those of the benchmark. Right now, the fund is heavily skewed toward the financial sector (which represents 44.7% of assets) and consumer discretionary (which represents 26.5%). Macauley says the fund’s seemingly narrow focus is somewhat misleading because of the way the industry wedges companies with divergent characteristics into the same sector classification. He cites fund holding American Tower. Because the company leases cell phone towers, the stock falls into the financial REIT classification, which puts it in the same sector bucket as asset managers, brokerages and insurance companies. Yet all these companies have very different characteristics and risk profiles.

Brookfield Asset Management, a holding in the financial sector category, was added to the portfolio in early 2014 and is now a top holding. The firm owns and manages “real” assets such as office buildings, power lines and toll roads for pension plans and other institutional investors. Macauley says its business is growing as these investors continue to move more assets to this increasingly popular real asset category. “Brookfield is a global business with tens of thousands of employees and an expertise in this type of investing,” he says. “It’s hard to replicate what they do.”

One of the fund’s newer additions, Hexcel Corp., became part of the portfolio in early 2015. A leading producer of carbon fiber for high-performance aerospace and industrial applications, the company has become a global powerhouse in an industry with high barriers to entry, requiring the companies within it to meet federal aircraft quality specifications and boast formidable intellectual property rights. With Boeing and Airbus competing to make lighter, more durable and more fuel-efficient aircraft, and other aerospace customers increasingly using carbon fiber and other advanced materials instead of aluminum, Hexcel should see a midteens rate of earnings growth over the next five years.

Among the Hennessy Focus Fund’s longtime holdings is O’Reilly Automotive, the third-largest auto parts retailer in the U.S. As of September 30, the stock, which has been in the portfolio for over a decade, accounted for 11% of fund assets. Earnings per share at the company have grown at an annualized rate of 20% since O’Reilly Automotive became part of the portfolio, and the stock has appreciated at a similar pace.

The company has 4,400 stores, up from 1,300 stores 10 years ago, and Macauley believes that the number could increase to between 6,000 and 7,000. The company has stronger buying power than many of its smaller competitors and a highly efficient distribution system, and these advantages continue to give it a leg up. The company’s strong management should continue to find ways to uncover value.

Another long-timer, kitchen cabinet manufacturer American Woodmark, made its debut in the portfolio in 2003. One of the top three kitchen cabinetmakers in the U.S., the company is benefiting from an uptick in demand for its products as new home construction and remodeling projects rebound. Unlike many of its more leveraged competitors, American Woodmark has a strong cash position and is building market share.

CarMax has been in the portfolio since 2004. The company, which has 150 used car stores around the country, provides a better, no hassle car-buying experience because its prices are fixed and it has a wider selection than a typical dealer selling trade-ins. Its market share has grown from 1% 15 years ago to 4% today, and Macauley thinks it’s well on the road to doubling its store base.