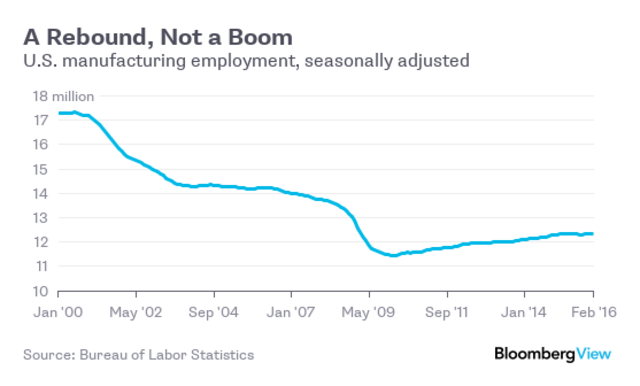

After a brutal period of downsizing and reorganizing, the U.S. manufacturing sector has become the most competitive in the world. Output per worker is higher than in any other major manufacturing country. Labor costs per unit of output are lower than in Brazil, Canada and Germany, and only slightly higher than in China. What's more, writes Gregory Daco of Oxford Economics in the new report from which the above facts are taken, "the U.S. is 'gifted' with a stable regulatory framework, a flexible labor market, low energy costs and access to a large domestic market. "So that's great! Time for a manufacturing renaissance, right? Well, maybe, eventually. But -- and Daco notes this in his report -- there are few signs of it actually happening yet. Yes, there are the almost 900,000 manufacturing jobs added in the U.S. since early 2010. But it's important to see that for what it is -- a modest rebound after a spectacular collapse:

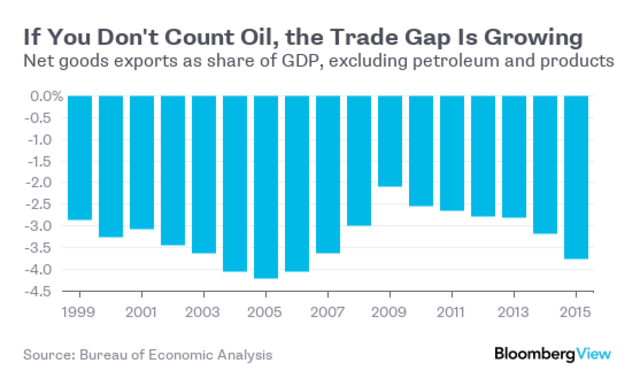

There has also been a big decline in the trade deficit, from 5.6 percent of gross domestic product in 2006 to 3 percent in 2015. But that turns out to be a product of (1) an increase in the trade surplus in services and (2) the huge boom in domestic oil-production and accompanying fall in global oil prices. Strip out petroleum and petroleum products, in fact, and the trade deficit in goods is only down a little from its peak, and has grown markedly over the past two years.

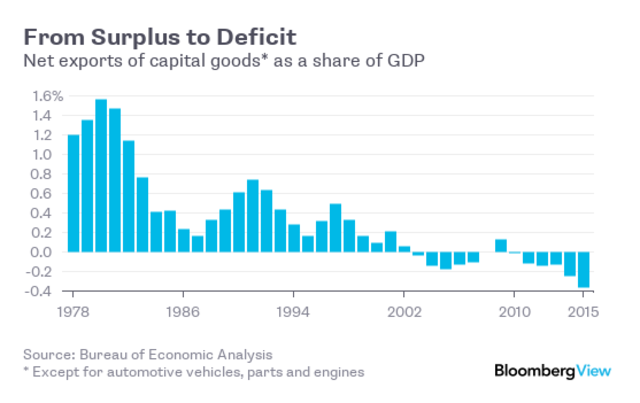

This seems like a good spot to mention that running a trade deficit isn't necessarily a bad thing. The growth in the deficit in 2014 and 2015 is due in part to the strength of the U.S. economy -- faster growth than in other major economies and a strengthening dollar have led to more imports and fewer exports.Still, you'd think that if there were a big return to manufacturing in the U.S. afoot -- "reshoring" is the term of art -- it would be making itself more apparent in the data. Consider, for example, trade in capital goods. While, the U.S. has been importing more cars and consumer goods than it exports for many decades, capital goods -- airplanes, medical equipment, semiconductors and so on -- have long been an area of comparative strength. Not so much anymore:

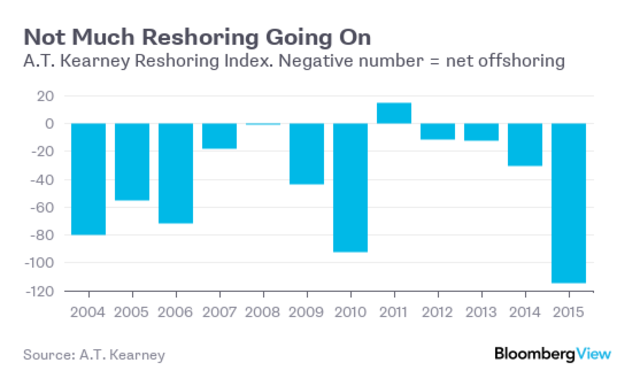

Again, one can find temporary factors increasing this deficit. The U.S. is usually a big net exporter of oil-drilling, mining and construction machinery, and recently demand for such equipment has plummeted (sorry, Caterpillar!). That demand will return someday, presumably.There really aren't many tangible signs, though, of a larger shift in manufacturing activity back to the U.S. The Boston Consulting Group, which has done as much as any organization to popularize the idea of reshoring manufacturing after years of offshoring to China and elsewhere, reported in December that a growing number of executives surveyed say they are moving production back to the U.S. from China or at least thinking about it. But rival consulting firm A.T. Kearney put out its own report in December asserting that "the reshoring phenomenon appears to have been more a one-off aberration than an inexorable trend." Here's the trajectory of A.T. Kearney's reshoring index, which measures net reshoring or offshoring based on actual import and production data:

Why isn't reshoring taking off? Daco, of Oxford Economics, stressed that such shifts don't happen overnight. "It takes quite a bit of time for a company to modify its supply chain," he said in a phone conversation. He also noted that "nearshoring" to Mexico, where unit labor costs are still substantially lower than in the U.S., remains popular.A.T. Kearney, in its reshoring report, said that industries trying to avoid rising labor costs in China have been moving production to other Asian countries, not to the U.S. -- and that that's probably not going to change soon:

The countries of South and Southeast Asia -- even after India is taken out of the equation -- have labor forces that run into the hundreds of millions of workers, so the gradual shift of certain industries to other Asian low-cost countries is likely to continue.