When I ask financial advisors what their long-term strategy is for growing their revenues-while at the same time keeping their marketing time and expenses under control-I often receive back answers such as:

"I attend various functions to meet prospective referral sources or clients."

"I take potential referral sources to lunch."

"I am immersed in various organizations where new business is generated."

The traditional marketing of professional services is to sell yourself to someone that has no experience working with you or your firm. When you step back and think about it, that sounds like paddling upstream against a very strong current!

Of course, it makes sense to get out and meet new people, but are you doing that at the expense of marketing to the people you already know-your existing clients? I am of the belief that the most effective time spent discussing the value and spectrum of your services is with those individuals who already know and believe in you and your firm.

So, before you run out to meet the next "prospect," you might want to take a step back and ask yourself, if you had only one hour per month to market your services, where would you spend it? Would you rather spend it convincing strangers that you are great at what you do and that they should refer people to you? Or would you rather spend it marketing yourself to existing clients, who already think you are great at what you do but who might not realize that you offer other services that they need?

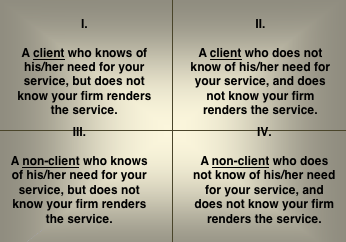

The professional service world, be it for a financial advisor, a CPA or a lawyer, is easily divided into four quadrants, as the accompanying chart indicates.

How would you feel if a client needed an advanced service that you render, but had no idea that you offer the service and used a competitor? It's so obvious that it's also very easy to overlook. The most effective hour that you could spend would be with a client in sector I-someone who needs what you do, but is unaware of your ability to satisfy their need. Isn't this a little easier than trying sell your services to someone you just met?

If this makes sense to you, your next question might be to ask how you get started marketing to existing clients. First, start by asking yourself two questions:

What advanced services are most appropriate for my client base and firm's skill set?

How do I engage my client?

If you are being held back from marketing to your existing clients because you are afraid they will be offended, don't worry. What I have found is quite the contrary. The client may have already been looking for help and is quite relieved that someone they trust has arrived to offer it. In fact, some financial advisors actually cause harm to clients by postponing planning. If you are still afraid to market new services to existing clients, consider some issues that can arise by failing to investigate their needs and offer solutions:

1. Business operating agreements are outdated and are not consistent with clients' current wishes, causing disputes upon retirement, disability or death of shareholder.

2. Employment agreements are not updated to reflect current responsibilities, salaries or benefits and are creating disagreements between partners and/or employees.

3. Asset protection plans that were established years ago are either not being followed correctly or are outdated for the current situation. Numerous individuals thought that they were protected when in reality, as time has passed, they have inadvertently not complied with their plan, leaving assets unprotected and subject to the claims of creditors.

4. Estate plans are outdated as goals, not reflecting changed family situations: children are no longer minors, have gotten married and may have children of their own. Financial situations have materially changed either for the better or for the worse. Some have even become divorced and not yet eliminated their ex-spouse from their wills.

Think about it. If your firm was at the heart of motivating your clients to engage in these services, not only will you be involved in bringing in the necessary professionals to carry out the plans-such as CPAs and attorneys-you should be billing for these advanced services at an enhanced rate, commensurate with the level of service-value billing. After you have held your client's hand throughout the planning process, future core services provided by your firm will be needed to maintain your client's plan.

But what is the hook? How do you get them engaged? One way that has worked for numerous firms is to begin the financial discussion by inquiring about the status of their life insurance. Why life insurance? For starters, article after article addresses how poorly life insurance as an asset class has performed. Nobody knows for sure, but from the articles I have read, the professionals I have spoken to and more specifically from my personal experience, nearly 75% of all in-force life insurance, is not performing anywhere near expectations (which means there is a 75% chance that you will find a problem that needs to be solved).

Issues include:

The policy will lapse prior to the death of the insured.

The annual premium for the same death benefit can be significantly reduced.

The same annual premium can purchase significantly more death benefit.

The policy is owned incorrectly, creating inheritance or income tax that could easily have been avoided.

The beneficiary noted in the policy is not consistent with current wishes and benefits will be paid to inadvertent beneficiaries.

In-force policies may be subject to premium increases where newer updated versions contain guarantees not available when the current policy was purchased. Depending upon the new insurance product purchased, future premiums will not be subject to potential increases in cost.

Many older policies cease at age 95 or 100 even if the insured is still alive. This will cause the policy to lapse with either no value or with a cash value far less than the death benefit. In some circumstances, the death of a policy before the death of the insured may create taxable income. Newer policies do not contain these age limitations.

Once a professional discussion of life insurance begins, there is only one way to properly evaluate a policy. You must begin with why the policy was purchased and what has since changed. Your clients' needs will become self-evident as the discussion progresses. And, as the financial advisor who initiated the process, you will lead the charge, directing all of the other players-from CPAs to attorneys-who may need to become involved in the process. And your efforts will not go unnoticed.

So if you can't remember the last time you called a client and asked them to lunch, with the billing clock off, just to chat about what is going on in their lives, I suggest you give it a try. After all, you'd do that for someone you met at a "networking event," wouldn't you? Like I said, it is so simple and self-evident that we forget who we are already indebted to as we pursue new clients.

When you do meet with your client, have a clear agenda and goals you would like to accomplish from the meeting. Start by finding out what is going on in their business and personal lives. Is there anything new (divorce, death, marriage, children, anew business partnership, etc.)? Have they set a long-term path for their business or personal estate plan? Educate them: Explain that a great place to start is by professionally evaluating their life insurance and their need for it.

Ask your client if he or she is aware that life insurance is a massively under-performing asset. For example:

5% to 10% of policies are at risk of lapsing in fewer than three years.

20% are in danger of lapsing between three and seven years.

80% need restructuring or replacement.

70% are "orphan policies," with no assigned or licensed agent.

If you are not sure that marketing to existing clients is "up your alley," ask yourself the following:

What type of business do you want to have? Do you want your clients to view you as a "one trick pony," or to see you as someone who plays a vital role in their overall financial health?

Where would you rather spend your marketing time and money? The most effective effort is spent with people who already know you and believe in you. They either do not know they need a certain service or may not know that you render the service or both.

When planning for the future of your business, you need to start by planning for your clients' futures. The most ironic part of the story is that much of the cost of your services can be paid for with the savings found by a professional review of their life insurance. That is a true win-win.

Richard Newman, CPA, PFS, AEP, is founder of Life Audit Professionals in Boca Raton, Fla. He can be reached at [email protected] or 561-948-2421.