The number of bulls is dwindling. In periods of extreme market volatility such as we have experienced in recent weeks—and Friday, January 15, 2016, in particular, when the Dow was down over 500 points at one point before paring losses—we find it helpful to try to take some of the emotion out of our investment decisions. As difficult as that can be at times, this approach can help us reduce the chances of selling at the bottom, even though the natural reaction for many is to panic and hit the sell button.

DERIVATIVES POSITIONING

Evidence of “capitulation,” essentially marking investors as throwing in the towel, can also signal the end of selling may be near. When the S&P 500 Index was at 1867 on August 25, 2015, many technical and sentiment stock market indicators were at extreme levels on heavy trading volume and were characterized by some as capitulation. This essentially means investors have all headed for the exits, leaving no one else to sell (in theory) and signaling a potential tradable stock market bottom.

One way to help measure how close to the bottom stocks may be is to use sentiment indicators to identify extremes in bullishness and bearishness. When the bulls are all washed out, in theory, there are few sells left to put more pressure on stocks. In this case, extreme bearishness can be viewed as a contrarian indicator and may signal that selling could be near an end.

Technical analysis can also help identify key price levels that may signal breaks in either direction. These tools can give us an idea of when the selling might stop and a reversal might ensue. An objective look at some data can be reassuring and help us make better investment decisions.

A closer look at sentiment indicators suggests most of the selling may be behind us. We haven’t seen full panic—or capitulation—but we have gained some confidence that the upside opportunity for stocks may outweigh the downside.

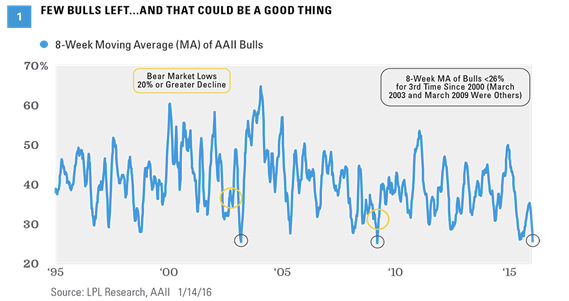

FEW BULLS LEFT

The latest American Association of Individual Investors (AAII) survey indicates an extreme scarcity of bullish investors, even more extreme than was observed in the summer of 2015. In fact, based on the latest AAII survey, bulls are as scarce as they were in 2009 and 2003, the last two major market bottoms. The reading of bulls during the latest week came in at 18%, the lowest level since April 2005. Bears have spiked as well, up to more than 45%, the most since April 2013.

Using weekly data, the eight-week moving average of the bulls is below 26% [Figure 1]. For comparison, this was the lowest since March 2009 during the depths of the financial crisis. The only other time it was less than 26% over the past 20 years was March 2003. This extreme level of bearish sentiment may suggest a lack of new sellers and that stocks may be nearing a bottom.

Another way to assess investor sentiment is by looking at the ratio of bullish to bearish positioning in the derivatives market. Recently, positioning in the derivatives markets has become much more bearish, according to data from the Chicago Board Options Exchange (CBOE). Coupled with the action in the AAII sentiment poll, this shows how dour most view the stock market currently. From a contrarian point of view, this could be a sign that a bottom may be near.

ASSESSING TECHNICAL DAMAGE

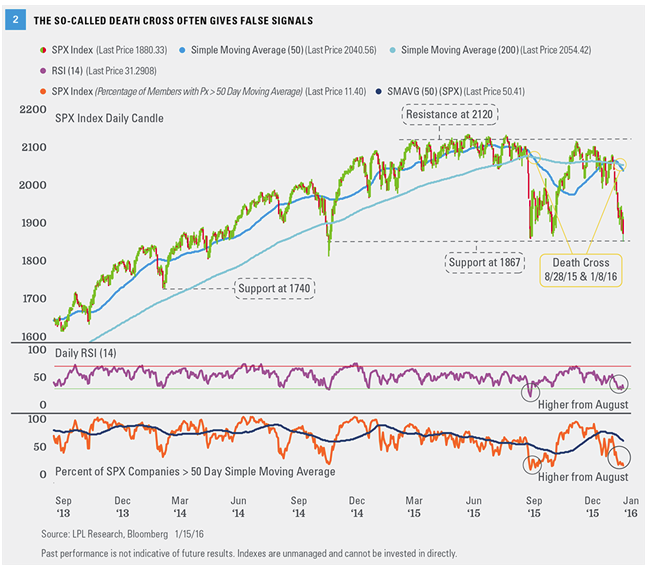

We can also use more traditional technical analysis to assess how likely it is that stocks are nearing a bottom. Over the past few weeks, the S&P 500 Index has incurred some technical damage, with the index now testing its August 25, 2015, low at 1867. From a technical perspective, a sustained break below the 1867 support level would establish a lower low, indicating the downtrend may continue. Conversely, a bounce off of the 1867 level would indicate stabilization by setting up a higher low, increasing the potential for a short-term bottoming process.

Another form of technical damage occurred on January 8, 2016, when the shorter-term moving average (50 periods) crossed below its longer-term moving average (200 periods) on the daily price chart (which some refer to as a “death cross”). This is the second time this cross has occurred over the past six months—the first occurred on August 28, 2015, very close to the stock market lows of August and 2015 [Figure 2].

Since 1980, the S&P 500 has experienced 16 of these crosses. In 11 of those instances, the S&P 500 was higher 3 months later, with an average gain of 4.7%. The numbers improve after 6 months, with gains in 10 out of 15 instances, and an average gain of 7.4%. And over 12 months, stocks are only down if accompanied by recessions. This indicator has provided many false bear market signals over time and often indicated the approach of a rebound (see our Weekly Market Commentary, “Consulting Our Technical Playbook,” for more on this topic).

CAPITULATION?

The Relative Strength Index (RSI) can assess capitulation by measuring the depth of oversold conditions. A greater frequency of steep declines over a period (in this case we use 14 days) coincides with a low RSI. The RSI at just over 18 on August 24, 2015, was considered extremely oversold, compared with the recent low back on January 8, 2016, at 29. Holding this level would be considered a higher low, indicating the potential start of a short-term bottoming process and increasing the likelihood that stocks move higher.

We can also look at the percent of S&P 500 companies above their 50-day moving average to assess capitulation. On August 24, 2015, this measure stood at 8.2, an extremely oversold, capitulation-like reading, compared with the more recent low of 12.7 on January 8, 2016. Again, should this level hold, it would suggest the start of a potential short-term bottoming process and, hopefully, a subsequent rebound in stocks. We may not have seen full-blown panic, but we have gained some confidence that the upside opportunity for stocks from here may outweigh the downside.

VALUATIONS

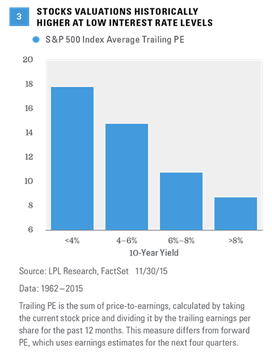

Another way to gauge sentiment is valuations, one of the more common worries about the ongoing bull market. The latest stock market correction has brought stocks down to a reasonable forward (next 12 months) price-to-earnings ratio (PE), below 15, down from more than 17 back in March 2015 (based on Thomson-tracked S&P 500 consensus estimates). On a trailing 12-month basis, at 15.8, valuations are in-line with the average since 1950 and slightly below the post-1980 average.

While valuations alone do not drive our investment decisions, especially in the short term, they can help entice buyers when stocks fall, especially at such low interest rate levels [Figure 3]. In fact, the dividend yield for the S&P 500 at 2.37% as of January 15, 2016, is higher than the yield on 10-year Treasury bonds at 2.03%. Corporate America, outside of the challenged energy sector, remains in very good shape and, we believe, is in good position to grow profits in 2016 despite the drags from the energy sector, a strong U.S. dollar, and slower growth in China.

WHAT ABOUT FUNDAMENTALS?

Technical analysis and valuations can provide some reassurance that a market decline might be nearing an end, but fundamentals are another key piece of the story. We continue to watch a number of fundamental indicators that might provide early warning of a potentially larger bear market decline. Look for an update on some of our favorite leading fundamental indicators in this publication over the coming weeks.

CONCLUSION

As difficult as it is in periods of heightened volatility, we encourage investors to stick with their plan. The natural emotional response is to sell everything and go to cash, but that is rarely the right decision. Technical analysis tools can help inform our decisions, in addition to valuations and fundamentals. Technical indicators, like valuation and fundamental indicators, are not perfect, but the convergence of extreme bearish signals indicate selling may be near an end.

Burt White is chief investment officer for LPL Financial

Any Bulls Left?

January 20, 2016

« Previous Article

| Next Article »

Login in order to post a comment