Key Points

• The era of very low and falling interest rates may be coming to an end, which could mean rising bond yields.

• The shift to higher yields is likely to be slow, in our view, but markets don’t appear to be prepared for the change.

• We suggest investors prepare for a potential rise in bond yields by trimming exposure to bonds with either long durations or high credit risk.

Is the market ready for higher bond yields? After years of extremely low yields at home and a surge in negative-yielding debt in Europe and Japan, you might think the market would seize on any sign that conditions may be changing. But that doesn’t appear to be happening.

The forces that pushed yields lower—low and falling inflation, and very easy monetary policies by major central banks—appear to be abating. While we don’t think this this means yields will snap sharply higher, these trends should lead to a slow increase over time.

Here, we’ll take a closer look at inflation and monetary trends and discuss some ways investors can prepare for the potential return of higher bond yields.

Inflation expectations

Inflation expectations are one of the main forces driving intermediate and long-term bond yields. In short, inflation eats away at the value of investment returns, so bond investors generally require higher bond yields (i.e., lower bond prices) as compensation if they think prices will rise over the long term.

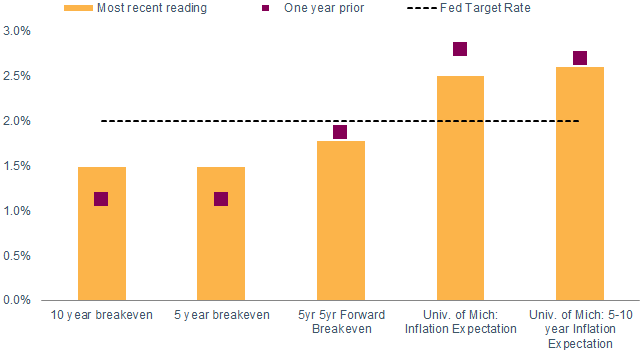

So where do things stand now? Inflation expectations haven’t moved significantly higher in the past year. Market-based measures of inflation expectations, such as the difference between Treasury Inflation Protection Securities (TIPS) and traditional Treasuries, indicate only a slight increase in inflation expectations over the past year—and those expected inflation rates are below the Federal Reserve’s 2% target level. Consumers’ inflation expectations have actually softened over the past year. For example, the University of Michigan’s inflation expectations survey shows that consumers have lower inflation expectations for the coming year than they did last year, though those expectations are still above the 2% target level.

Inflation expectations haven’t changed much in a year

Source: Bloomberg. Readings for each category are as of 8/30/2016 and 8/30/2015. The breakeven inflation rate is a measure of inflation expectations based on the difference in yields between TIPS and regular Treasuries of comparable maturities. The five-yea, five-year forward breakeven rate is a measure of inflation expectations over the five-year period that begins five years from today.

Inflation is edging higher

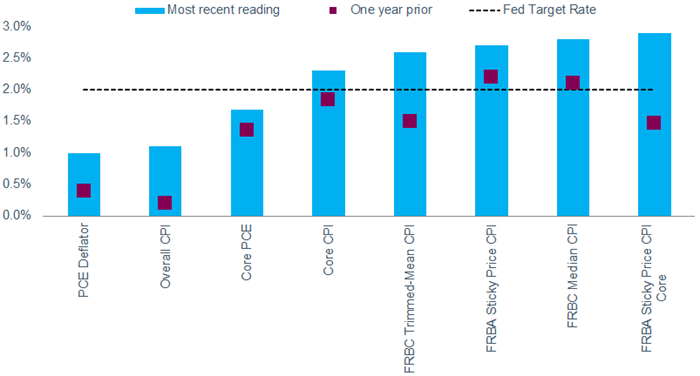

How do those expectations stack up against actual inflation? There are many ways to measure price changes, but by most measures the trend is moving up.

The Fed’s preferred measure is the deflator for personal consumption expenditures excluding food and energy (core PCE), though Fed Chair Janet Yellen has said the bank watches many different indicators. Below we’ve compiled a chart of the indicators cited by the various members of the Federal Open Market Committee over the past two years. These different measures reflect different methodologies, but all show that inflation is higher today than a year ago. Several are now above the Fed’s 2% inflation target.

Inflation indicators have edged up over the past year

Source: Bloomberg. Readings for each category are as of 8/30/2016 and 8/30/2015.

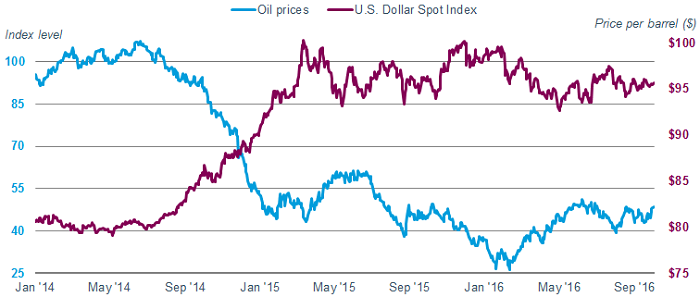

Inflation is likely to drift higher now that oil prices and the dollar have stabilized. Although we don’t expect a significant rise in oil prices since supply is still high relative to demand, prices do appear to have settled into a range of about $45 to $50 per barrel after having dropped from more than $100 per barrel over the past two years. The drag on overall inflation from falling oil prices appears to be abating.

Similarly, the dollar has stabilized this year after rising 20% from mid-2014, which should also lessen downward pressure on inflation. When the dollar rises, it tends to slow growth by making U.S. exports less competitive and hold down import prices, reducing inflation pressures. With a more stable dollar, the dampening effect on inflation should ease.

Oil prices and the U.S. dollar have stabilized

Note: U.S. Dollar Index (USDX) is an index (or measure) of the value of the United States dollar relative to a basket of foreign currencies. Source: Bloomberg. U.S. Dollar Spot Index (USDX) and Crude Oil Prices: West Texas Intermediate - Cushing, Oklahoma, Dollars per Barrel, Daily data as of 9/30/16. Past performance is no guarantee of future results.

Central Banks shift tactics

Meanwhile, foreign central banks appear to be shifting away from deeply negative interest rates, which could also help drive bond yields higher.

At its most recent meeting, the European Central Bank kept its target interest rate intact, contrary to expectations for a rate cut. Similarly, the Bank of Japan reviewed its policies recently and decided to adopt a policy that would target positive long-term interest rates. Both central banks have acknowledged that because low-to-negative interest rates squeeze banks’ profits from lending, such loose policy settings were actually making it difficult to push money into the economy. Moreover, very low to negative bond yields make it difficult for pension funds, insurance companies and other long-term investors to earn enough income to cover their obligations.

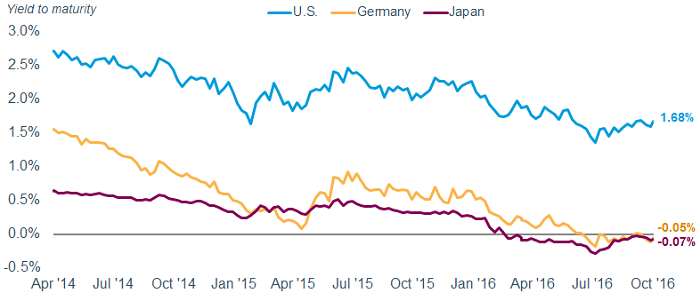

With nearly half of U.S. Treasuries held by foreign investors and the correlation among major international bond markets high, moves in one market can influence others. While still very low, bond yields in Japan and Germany have moved up from the most negative yields recently.

International bond yields have been rising modestly

Source: Bloomberg. Ten-year bond yields, U.S. (USGG10YR), Germany (GTDEM10YR) and Japan (GTJPY10YR). Data as of 10/4/16.