Once again, stocks have rallied on the news that the U.S. and Japanese economies remain sufficiently weak that both require still more gentle nurturing from their respective central banks. In the absence of growth, investors continue to take solace in monetary accommodation, particularly as the corollary to soft growth—low interest rates—tends to prop up risky assets.

But there can be too much of a good thing. Although soft growth may be positive for equities, given the typical monetary response, negative growth is not. Bear markets typically coincide with recessions. And should a recession occur now, it would be particularly problematic for stocks: Earnings estimates for next year are aggressive at a time when central banks are struggling to conjure mediocre growth, even with the benefit of an evermore exotic toolkit.

All of this suggests that investors should be sensitive to any information that suggests the probability of a recession is increasing.

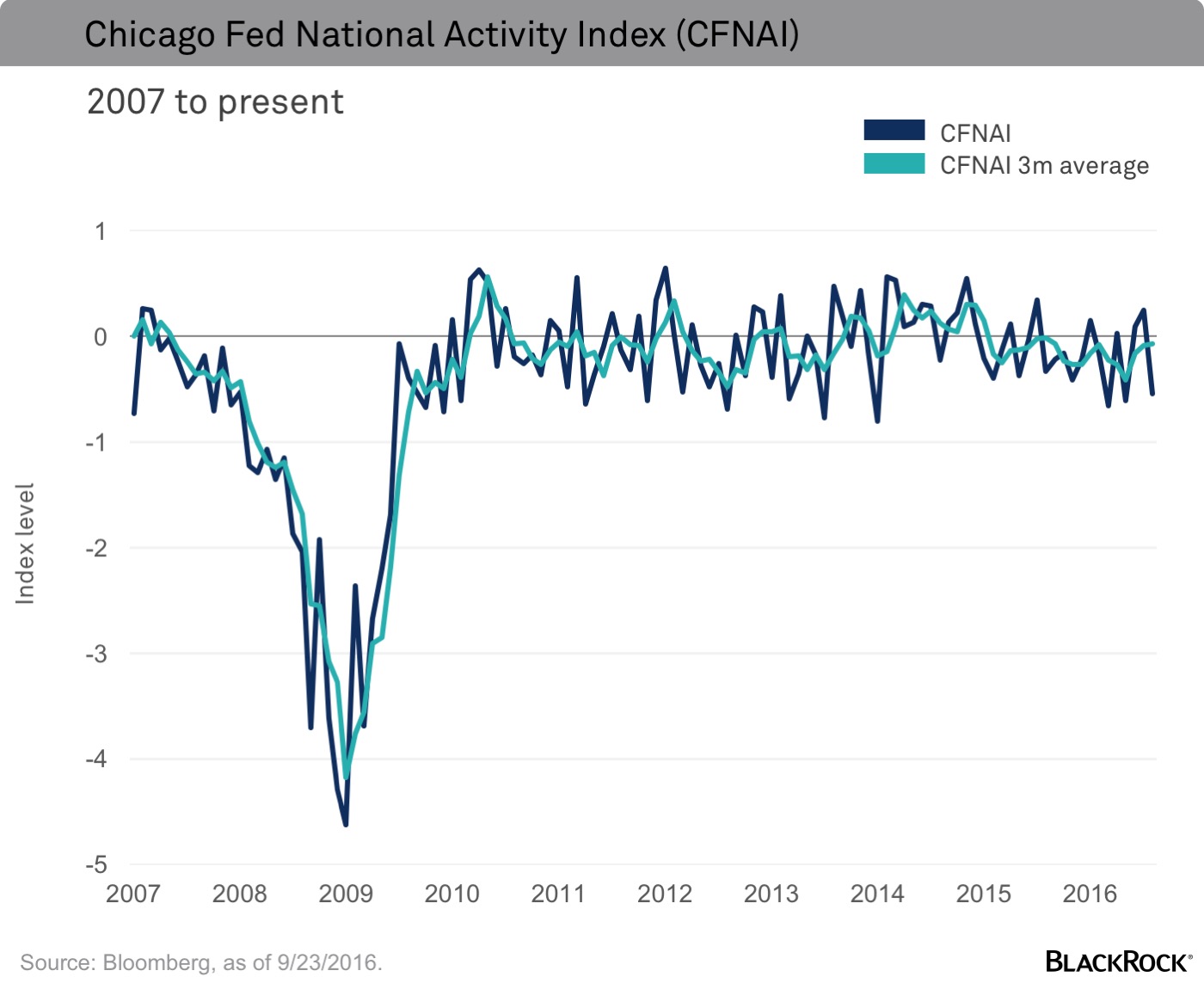

In fact, the Chicago Fed National Activity Index (CFNAI), my preferred leading indicator, recently fell back into negative territory (see the chart below). While this hasn’t stopped the market from imbibing the nectar of cheap money, I have watched this indicator long enough to know that it is telling us something and it merits our attention for three reasons.

1. Growth may disappoint.

Of all the indicators I’ve looked at, the CFNAI has the strongest leading relationship with real gross domestic product (GDP). Over the past 35 years, the level of the CFNAI has explained approximately 40% of the variation in the following quarter’s GDP (source: Bloomberg data). At the very least, the most recent reading suggests that the economic—and by extension earnings—rebound that the market is expecting in the second half may not materialize.

2. Consistently negative readings coincide with recessions.

More troubling than the level of the CFNAI is the pattern. The three-month average has been negative since early 2015. The last time this happened was the summer of 2007. Going back to 1980 this pattern has only occurred during recessions, or the period leading up to one.

3. Slower growth is inconsistent with rapid multiple expansion.

Historically, when CFNAI readings have been consistently negative, the multiple on the S&P 500 has been flat year-over-year, according to Bloomberg data. Today, the S&P 500 trades at a 15% premium to where it was a year ago. This confirms that markets have become increasingly dependent on ultralow rates.