The world of investing has changed dramatically. Over the past decade, many investors have discovered that conventional passive growth stock approaches failed to meet their goals. Following a buy-and-hold approach, investors suffered losses of as much as 51 percent during the 2000 through 2013 period. We believe conventional portfolio theory regarding the benefits of diversification has been broadly misinterpreted to mean that market returns will bail you out, and so investors should not worry about short-term losses. But in reality, typical market losses like these can make it difficult for investors to fund their retirement sufficiently, and may cause them to outlive their stream of income.

The world of investing has changed dramatically. Over the past decade, many investors have discovered that conventional passive growth stock approaches failed to meet their goals. Following a buy-and-hold approach, investors suffered losses of as much as 51 percent during the 2000 through 2013 period. We believe conventional portfolio theory regarding the benefits of diversification has been broadly misinterpreted to mean that market returns will bail you out, and so investors should not worry about short-term losses. But in reality, typical market losses like these can make it difficult for investors to fund their retirement sufficiently, and may cause them to outlive their stream of income.

In 2008, many investors found that traditional approaches relying on diversification to reduce risk failed them. Portfolio management strategies which were generally considered sound faltered. The markets defied the tenets of covariance and diversification and many asset classes declined precipitously across the board. Conventional portfolio construction theory has held forth the notion that asset diversification reduces risk. We believe investors have misunderstood this, interpreting it to mean that diversification protects capital. While diversification can reduce total risk if the correlation among the portfolio assets is low, we feel the real problem is that in periods of market turmoil, the low correlations evaporate as many assets move down together. Therefore, just when you need the risk-reducing benefits of diversification the most, they actually disappear, and capital is lost rather than protected.

Managing Portfolios For Market Capture

We believe investment allocators need to develop a process to find managers who have demonstrated ability over time to protect capital from severe losses in bear markets while capturing good returns in bull markets. Such ability may be confirmed using capture ratio statistics. To meet the “acid-test,” investment approaches must work in both good and bad market cycles. We believe that today more than ever, investors need to develop better allocation and manager selection approaches to replace the risk benefits of diversification to improve their odds of building capital more consistently.

The goal of each WBI strategy is to provide investors with wealth-building investment strategies that target an optimal blend of bear market capital preservation and bull market return. WBI’s responsive investment management process is designed to adjust portfolio allocations from being fully invested to maximize return, to raising cash to protect capital as risk increases. We believe that capital preservation in bear markets is far more important to achieving success than chasing the highest returns during bull markets.

Our observations about investor behavior in down-market cycles became the driving force behind the development of WBI’s powerful investment methodology. Each portfolio design starts by determining a risk and return profile that targets a down-market capture ratio of less than 100 percent when compared to a representative market index. We also target an up-market capture of as close to 100 percent as possible while continuously seeking to protect capital. The optimal blend of up-market and down-market capture depends on the portfolio investment objective.

For example, WBI’s Absolute Return Dividend Income Portfolio (DGI) seeks a down-market capture ratio of 50 percent with an up-market capture ratio of 70 percent to the S&P 500 Index. An additional portfolio design criteria is to limit cumulative down market losses, which for DGI is expressed as a maximum drawdown target of 20 percent. While this is a target and not a guarantee, we believe the DGI portfolio design targets provide investors with a pretty conservative loss profile when compared to the S&P 500 Index. Since DGI’s inception on June 30, 2003, investors experienced a net of fee maximum drawdown of 21.31 percent compared with 45.80 percent for the index. DGI also achieved a down-market capture ratio of 42 percent and an up-market capture ratio of 60 percent to the S&P 500 Index. The charts displayed are based on a net of fee calculation equaling gross of fee minus an assumed 1 percent WBI annual fee.

The benefits of developing an optimal blend of up-market and down-market performance can be very powerful over an investor’s lifetime. To illustrate the potential long-run capital and wealth-building benefits of WBI’s investment approach, we built a quantitative illustration to estimate how an investor may have fared going back to 1928. There is no guarantee that we would have been able to achieve the results illustrated, however they are based on the actual capture ratio we achieved since each portfolio’s performance composite inception.

The Long Run

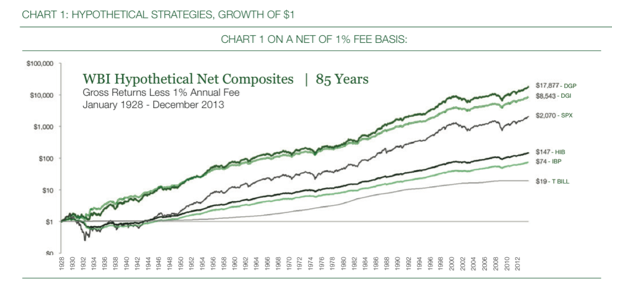

WBI offers four flagship strategies: Absolute Return (AR) Dividend Growth (DGP), AR Dividend Income (DGI), AR Balanced Plus (HIB), and AR Balanced (IBP). Chart 1 illustrates the hypothetical results of these strategies, estimated over the 85-year period January 1, 1928, through December 31, 2013. The results displayed in Chart 1 were developed by quantitatively back-testing the actual monthly performance composite records, net of fees, of WBI’s four flagship strategies currently representing approximately $2.6 billion of total assets under management in more than 10,000 separately managed accounts.

While chart 1 displays hypothetical rather than actual performance records, it is intended to illustrate the characteristics of strategies currently employed by WBI, had they been available over a long-term horizon covering a wide variety of economic and market cycles. Both of the equity strategies (DGI and DGP) significantly outperform the S&P 500 Index over the period, while both of the balanced strategies (HIB and IBP) significantly outperform fixed income as represented by the U.S. 3-month Treasury bill.

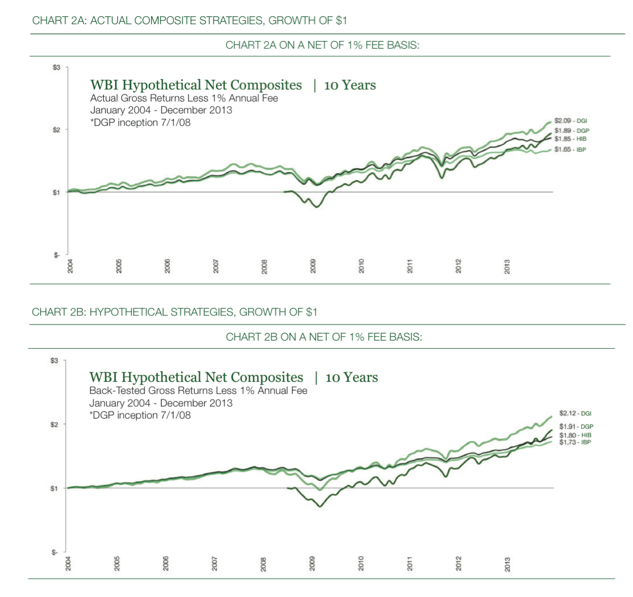

How reasonable are the hypothetical results? We compared the 10-year performance periods of WBI’s actual monthly performance composite records, net of fees, versus the corresponding hypothetical results in Charts 2A and 2B.

Chart 2A illustrates the 10-year historical performance records of the actual monthly performance composite records, net of fees, of WBI’s four flagship strategies, while Chart 2B displays the hypothetical back-tested results over the same period.

The charts highlight the similarity of the hypothetical performance with the actual performance -- all cumulative hypothetical growth values are within pennies of the actual growth values, with similar volatility characteristics.

Over their respective longest concurrent periods, cross-correlations of the hypothetical strategies versus the actual composites were high, as follows: DGP 0.93; DGI 0.88; HIB 0.65; IBP 0.60. Risk as measured by the monthly standard deviation of the results is also quite similar.

Return, Risk And Risk-Adjusted Return

Investors are concerned with risk as well as return. The terminal values illustrated in charts 1, 2A and 2B illustrate the compounded cumulative return of a hypothetical $1 investment; the variability of each performance record indicates the risk inherent in each strategy.

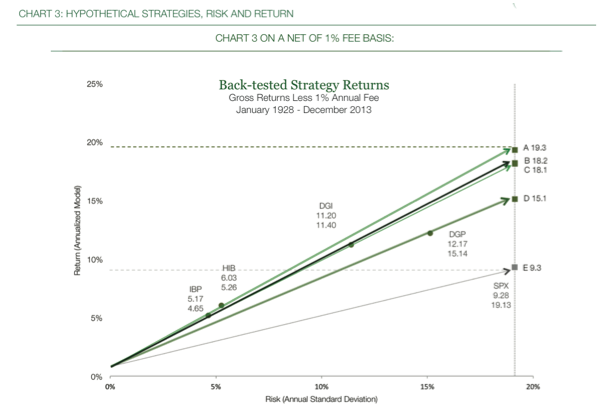

In Chart 3, we display the 85-year hypothetical performance illustration of the strategies from another perspective -- in mean-variance space. This view plots the hypothetical return, along the vertical axis, versus the risk of loss, along the horizontal axis. One benefit of this graphical approach is that investments with various levels of risk can be compared in an apples-to-apples fashion.

Chart 3 highlights an important benefit of how the WBI investment approach can be superior to a passive investment in a market index. Some strategies, such as DGP and DGI, are designed to have more aggressive investment profiles, meaning they seek higher returns. Other strategies, such as HIB and IBP, are designed to have more conservative performance, meaning they seek lower risk. All the strategies are designed to have better risk-adjusted performance than the market overall. Chart 3 illustrates that, over the long run, these strategies can accomplish their stated goals. In the back-tested illustration, all of the strategies exhibited significantly lower risk than the market.

Lower risk translates into losing less in the strategy than the market loses when it declines. Over time, compounding gains along with such limited losses can have a large impact on the total value of compounded wealth, as we saw in Chart 1. The lines connecting each strategy from an assumed risk-free rate of 1 percent in Chart 3 provide more insight into the true value of such a risk-managed investment approach. The slope of these lines shows graphically a statistic commonly used to measure risk-adjusted return, the Sharpe Ratio. The higher the Sharpe Ratio, the better. The points A, B, C, and D, where, if we were to lever strategies to the same level of risk as the market, show the risk-adjusted returns of each strategy, graphically displaying another risk-adjusted return statistic, the Modigliani-Modigliani measure known as M-squared. For example, point A shows that the hypothetical risk-adjusted return of a strategy replicating HIB is 19.3 percent, which is more than double the market return of 9.3 percent at the same level of risk. Point B shows the hypothetical risk-adjusted return strategy replicating DGI is 18.2 percent; point C shows that the hypothetical risk adjusted return of a strategy replicating IBP is 18.1 percent; and point D shows that the hypothetical risk-adjusted return of a strategy replicating DGP is 15.1 percent. Chart 3 shows that by both measures, Sharpe Ratio and M-squared, all of the back-tested strategies have higher risk-adjusted returns than the market.

Conclusions

We believe investors need to replace antiquated diversification risk-reduction strategies with a more capture-ratio-oriented approach to find managers who have demonstrated the ability to provide the desired blend of return and risk management based on client risk profiles. Selecting managers who have historically demonstrated performance with a desirable blend of up and down-market capture ratios should allow investment allocators to develop portfolio allocations that will allow investors to stay more comfortably invested for the long run, and especially when markets turn bearish.

Donald Schreiber, Jr. is CEO and co-portfolio manager of WBI Investments Inc., which manages $2.6 billion for financial advisors and their clients. Since founding the firm in 1984, Schreiber has focused company resources on developing the firm’s proprietary value-oriented, dividend-based, risk-managed investment approach.

Craig French is portfolio manager for WBI Investments Inc. French previously worked at Lasair Capital as senior investment officer. Prior to his tenure with Lasair Capital, French was a partner and director of Risk Management and Quantitative Research at Corbin Capital Partners. Previous to joining Corbin, French was the U.S. Equity Strategist for SEI Investments.and an analyst and associate at Goldman Sachs Asset Management.