Last year represented a "normal" economic and investment environment only when compared with the shocking events and one-way markets of 2008 and 2009. It was a year of progress-the deep recession passed and financial market volatility receded. Yet fallout from the credit crisis was everywhere: sovereign debt panic in Europe, muni credit worries in the U.S. and unprecedented aggressiveness by the Federal Reserve to avoid a flameout of the fragile economic recovery.

What follows is an assessment of the opportunities and risks facing high-net-worth investors in the year ahead.

The Fed's announcement of another round of aggressive monetary easing in November indicated that policymakers still believe the recovery is fragile. We concur. An extended period of uncomfortably slow growth is likely-something between recession and prosperity.

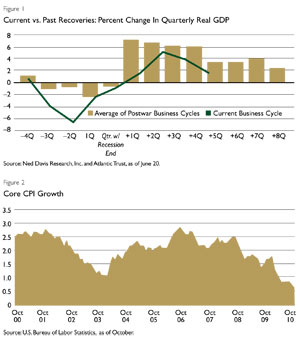

We believe unemployment will remain elevated for years, leading to subdued consumer spending. This should be offset by somewhat better capital investment, as cash-rich businesses attempt to ramp up their productivity. Exports should also be a source of relative strength, as demand from faster- growing overseas economies is likely to be sustained. A real GDP growth rate of 2% to 2.5% through 2011 is likely. (See Figure 1.)

There is great concern that the huge debt accumulation of the government will spark an inflationary money-printing binge. This is a significant long-term risk, but there is too much slack in the economy for inflation to rise anytime soon. Indeed, growth in the 12-month core Consumer Price Index (CPI) slowed to just 0.6% in October, the slowest rate since the U.S. Bureau of Labor Statistics began computing the numbers in 1958. Continued weakness in the job market means there will be minimal wage pressure. Thus, it is likely that inflation will stay quite subdued at least through 2011. (See Figure 2.)

Fiscal Restraint Begins

At this point, the biggest wild card for the economy may be politics and policy.

The decisive midterm election results have begun to clarify the fiscal policy outlook. The Republican takeover of the House of Representatives will blunt many of the Obama administration's plans to further intertwine the federal government and the private sector. Tax policy will also be impacted, as it appears all of the current Bush tax cut rates will be extended for two years, at least temporarily foiling the administration's desire to raise tax rates on upper-income families.

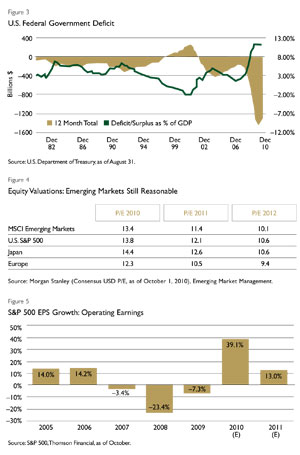

The biggest issue for the economy's long-term health-and perhaps for sentiment in the financial markets in 2011-will be whether the nation's trillion-dollar deficit is addressed by the more balanced (or gridlocked?) power structure in Washington. The election results and investor sentiment polls indicate that both Main Street and Wall Street believe that reducing the size of the federal government and slashing the deficit are high priorities. After his political setback, President Barack Obama has little choice but to adopt the mantle of fiscal responsibility. Meanwhile, Republicans will at least partially own the results of the economy's performance and perceptions about whether government is helping or hurting. We believe the chances are good that a deficit reduction package of modest size will be signed into law in 2011. While it would be a drop in the bucket, as the saying goes, "If you want to pull yourself out of a ditch, the first step is to stop digging." (See Figure 3.)

The Federal Reserve's decision to enact further monetary stimulus has so far produced a classic "buy the rumor, sell the news" reaction. In late August, the Fed telegraphed its intention to implement another round of quantitative easing to counter what looked like a flagging economic recovery. This was a major reason for the 13.5% surge in global stock markets (MSCI World Index) in September and October. Since the November 3 announcement of the Fed's plan to purchase $600 billion in long-term Treasury securities through mid-2011, both stock and bond investors have had second thoughts. The Fed's thesis-that they needed to lower long-term interest rates to stimulate bank credit and avert a double-dip recession and deflation-seems less credible in the face of recent stronger economic reports.

"Go Where the Growth Is ... And Where The Debt Isn't"

Our roadmap for assessing where opportunities abound-and risks lurk-was neatly summarized by a member of Atlantic Trust's asset allocation

committee: "Go where the growth is ...and where the debt isn't."

Excessive debt was the weakest link in a chain of events that caused the worst global recession and bear market since the Great Depression. Economies highly dependent on debt-fueled policies suffered the most. Those governments, in turn, combated the bursting of the credit bubble with a flood of public spending to avert further economic chaos, driving governments deeper into debt. After more than two years, this strategy has worked to stabilize the global economy. But the recovery has been uneven and has left certain countries and investment strategies in a better place than others. Atlantic Trust's major asset allocation themes have been developed from this perspective: emphasizing opportunities with organic growth and minimizing exposure to investments weighed down by debt.

The Emerging Market Engine

The developed markets of Europe continue to struggle with sovereign debt problems.

While growth in the core economies of Germany and France has been better than expected, impending austerity measures foreshadow anemic growth in 2011. Meanwhile, Japan remains in its 20-year funk.

Emerging market equities have experienced a strong period of growth since bottoming in early 2009, so much so that some investors are speculating whether these markets have gotten ahead of themselves. We believe that the case remains strong for continuing to allocate capital to these faster-growing economies. The massive transition from agriculture-based economies to manufacturing and service economies is a long-term phenomenon that will ultimately dominate shorter-term peaks and valleys in equity market performance. Macroeconomic and political changes in these countries have substantially reduced the potential for future, fundamentally based crises.

In the midst of 2008's financial crisis and the two years that have followed, China and other economies have demonstrated remarkable resilience. They will continue to be the growth engines of the global economy. (See Figure 4.)

U.S. Equity: A Stock Picker's Market

Despite recovery years in 2009 and 2010, the S&P 500 Index remains about 25% below its October 2007 peak (as of November 30). We believe that some progress toward regaining the old high can be achieved in 2011, but with muted investor expectations. Risk of the dreaded double-dip recession is low, but the outlook for economic growth is dreary. Equity valuations are reasonable in the context of low interest rates, but earnings growth in 2011 will substantially decelerate from the torrid pace of the last six quarters. We envision a market with continued volatility that progresses in two steps forward, one step back fashion. (See Figure 5.)

This scenario sounds a lot like 2010. However, we expect at least one major difference: There will be much higher disparity in individual stock returns. The 2010 market was notable for its very high correlation of returns, with little distinctions based on quality or valuations. An unusually high percentage of trading strategies were driven by macroeconomic calls on the overall market's direction. With this mindset, many investors' assessment of the stock market might be described as Jeffersonian-as if all stocks are created equal. They are not, of course. In time, we think investors will realize that the outlook is actually fairly certain-slow growth for a long time. When this occurs, more security-specific differentiation is likely, which will create a far more hospitable environment for active managers. Large-cap multinationals with strong balance sheets and above-average dividend growth should be the sweet spot for U.S. equities in 2011.

Fixed-Income Markets

The government bond markets continue to be whipsawed by monetary and fiscal policy, and ever-changing assessments of the economy's strength. With the two-year note yielding less than 0.5% and the ten-year yielding less than 3.0%, we do not view Treasuries as good value, though they will continue to be a place to hide when there is macro risk.

After a late year selloff, the municipal market has become slightly more attractive relative to Treasuries. Muni credit quality has come under the microscope with California and Illinois facing enormous budget challenges. However, a broad assessment of the landscape indicates that state and local tax revenues are beginning to increase as the economy stabilizes.

The Fed has become the "leverager" of last resort and through quantitative easing is further expanding the size of its balance sheet. As a result, interest rates across the yield curve are likely to remain lower for longer than previously anticipated. With yields unusually low, we would look to a variety of other enhanced yield income sources to complement high-quality municipal positions, such as: emerging market debt, senior floating rate bank debt and mid-tier quality corporate debt. For investors willing to take on more volatility to build portfolio yield, we also favor energy master limited partnerships and equity income strategies blending higher yielding stocks, REITs and convertible and preferred securities.

David L. Donabedian, CFA, is chief investment officer of Atlantic Trust, the wealth management division of Atlanta-based Invesco.