For many US investors, domestic bonds have been the cornerstone of a “core” fixed-income allocation. While this approach may have served investors well in the past, we believe a changing fixed-income landscape may prompt a consideration of new approaches, including expanding one’s fixed-income horizons to international bonds.

We believe investors should understand three potential benefits of diversifying their core bond holdings beyond benchmarks such as the Barclays US Aggregate Bond Index into global bonds – and that they should understand the potential role of currency hedging in seeking to manage the risk and returns of bond allocations. Here, we explore the reasons we believe global bonds are worth investors’ attention now.

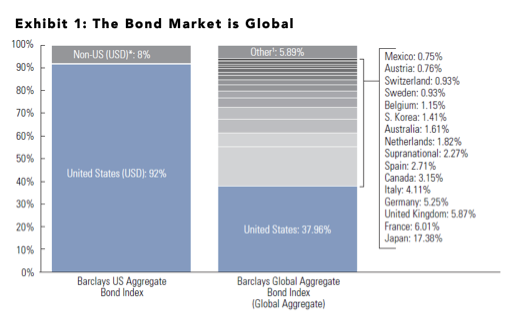

1. Today’s opportunity set is global. With historically low interest rates and the potential for rate increases by the Federal Reserve in the coming months and years, many investors may see limited opportunity in US fixed income. We would point out that the US market is only part of the story of global bonds (See Exhibit 1). Worldwide, other major central banks’ monetary policy remains accommodative. In our view, the European Central Bank (ECB), to take one example, may not enact tighter policy for years. We believe the policy divergence between the US and other world central banks may create a number of potentially attractive investment return opportunities for global bond portfolios.

Source: GSAM, Barclays. As of 3/31/16. *Non-US refers to USD-denominated emerging and developed market exposure. 1 Other refers to countries with less than 0.5% exposure. Past performance does not guarantee future results, which may vary.

All charts are based on indices and do not represent any Goldman Sachs fund. Diversification does not protect an investor from market risk and does not ensure a profit.

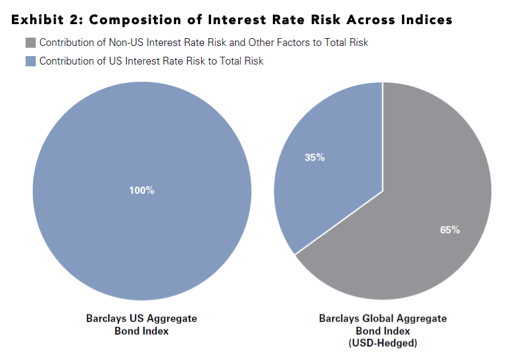

2. Going global may help investors diversify interest rate risk. Although global interest rate movements are frequently synchronized, monetary policy divergence between major global central banks remains a key theme. We believe a portfolio’s exposure to US interest rates should be complemented with exposures outside the US. Although currency-hedged global bonds (as represented by the benchmark Barclays Global Aggregate USD-Hedged Index2) have exhibited a higher overall duration3 than the Barclays US Aggregate Bond Index, their sensitivity to US rates has been smaller.4 For US investors, we believe that global bonds provide investors with the potential opportunity to diversify their US interest rate risk into global rate risk.

Source: GSAM as of 3/31/16. Please reference additional disclosures. Past performance does not guarantee future results, which may vary.

All charts are based on indices and do not represent any Goldman Sachs fund.

2. The Barclays Global Aggregate Bond Index hedged to the U.S dollar is an unmanaged index, provides a broad-based measure of the global investment-grade fixed-rate debt markets and covers the most liquid portion of the global investment grade fixed-rate bond market, including government, credit and collateralized securities. The Index figures do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

3. Duration: a measure of the sensitivity of a bond’s price to interest-rate changes.

4. Currency-hedged global bonds are represented by the benchmark Barclays Global Aggregate USD-Hedged Index.

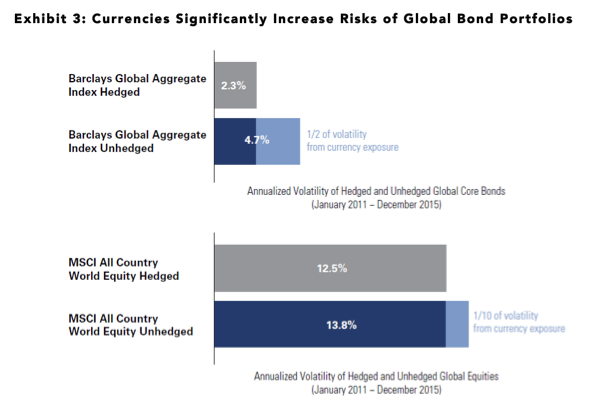

3. Global bonds may offer investors an attractive balance between risk and return – a currency-hedged approach may help. The pros and cons of currency hedging are a frequent topic in equity portfolios, but the subject arises less frequently for bonds. In our view, this is an important omission. We think of currencies’ impact on core bond allocations as a “blunt-force instrument.” In contrast to the lighter impact on equity volatility, currencies can drive a large portion of the month-to-month movement of a bond allocation.

Exhibit 3 shows that over the period of January 2011 – December 2015, currency moves drove about half the volatility of the unhedged global bond index, versus only about one-tenth the volatility of an unhedged approach to global equities.

For many investors, core bonds play a risk-managing role in the overall portfolio in comparison to more volatile equity and low-quality fixed income. If currency exposures cause an increase in risk, the allocation may work against these investors’ intended goals.

Source: Bloomberg, GSAM, covering the five-year period Dec. 31, 2010 through Dec. 31, 2015. Volatility is a statistical measure of the dispersion of returns for a given security or index. See end notes for index definitions and important disclosures. Index returns do not represent any GS Fund. Past performance does not guarantee future results, which may vary.

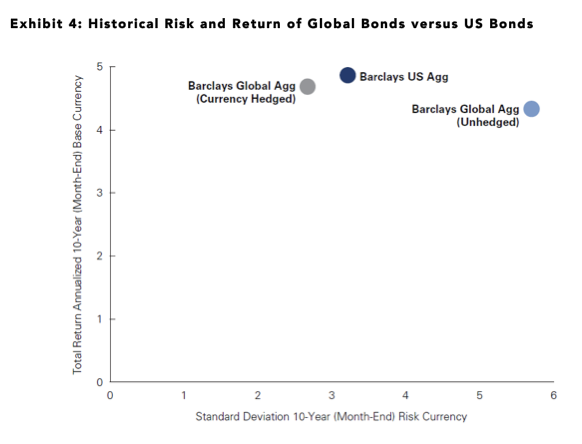

However, currency-hedged global bond portfolios have often delivered more attractive risk-adjusted returns than the unhedged equivalent. Over the five years ending December 31, 2015, hedged global bonds returned 3.9%, while unhedged global bonds returned 0.9%.

As a result of this higher return and lower volatility, hedged global bonds’ risk-adjusted returns have been stronger, with the unhedged index’s Sharpe ratio5 of 0.19 over the period, versus 1.68 for the hedged index (Exhibit 4).

For investors who believe that the US Dollar’s lower volatility will continue (or those who believe that the US Dollar’s strengthening trend since 2014 will continue), we believe these characteristics are arguments for incorporating global bonds into a core fixed income allocation.

In sum, we believe global bond exposure can help enhance investors’ core bond holdings by seeking to deliver additional country and interest rate diversification, while maintaining a similar risk/return profile to that of traditional core fixed income.

Source: Morningstar, 10-Year Annualized total net returns as of 3/31/2016.Past performance does not guarantee future results, which may vary. Index returns do not represent any GS Fund.

Risk Considerations

Investing in fixed income securities are subject to the risks associated with debt securities generally, including credit, liquidity and interest rate risk. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. Issuers of sovereign debt may be unable or unwilling to repay principal or interest when due. Investments in mortgage-backed securities are also subject to prepayment risk (i.e., the risk that in a declining interest rate environment, issuers may pay principal more quickly than expected, causing the Fund to reinvest proceeds at lower prevailing interest rates). Derivative instruments may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; risks of default by a counterparty; and liquidity risk (i.e., the risk that an investment may not be able to be sold without a substantial drop in price, if at all). The Fund may invest heavily in investments in particular countries or regions and may be subject to greater losses than if it were less concentrated in a particular country or region.

Christina Kopec and Jason Singer are managing directors at Goldman Sachs Asset Management.