We believe the economic challenges to Brexit are significant. Britain’s specialization in services—not only in finance, but also law, accountancy, media, architecture, pharmaceutical research, etc.—makes membership in the EU single market critical, whereas it makes little economic difference to Germany, France, or Italy whether Britain is an EU member or simply in the World Trade Organization (WTO).

Britain would need to negotiate access to the EU single market for its service industries, whereas EU manufacturers would automatically enjoy virtually unlimited rights to sell goods in Britain under WTO rules.

In the event of Brexit, Britain would negotiate an EU association agreement similar to those negotiated with Switzerland and Norway, the only two significant European economies outside the EU. Among the conditions accepted by Norway and Switzerland that the EU would regard as non-negotiable are four that completely negate the political objectives of Brexit. Specifically:

• Norway and Switzerland must abide by all EU single market standards and regulations, without a say in their formulation.

• They must agree to translate all relevant EU laws into their domestic legislation without consulting domestic voters.

• They must contribute to the EU budget.

• Finally, they must accept EU immigration, resulting in a higher share of EU immigrants in the Swiss and Norwegian populations than in the United Kingdom.

If Britain were to reject such infringements on national sovereignty, its service industries would be locked out of the single market. In the event of Brexit, the pound is likely to weaken further from current levels. Perhaps, this will help make some of the manufacturing in central and northern England more competitive.

Although the risks of Brexit have not been downplayed by the Remain campaign, years of criticism of Europe by virtually the entire U.K. press have left the population grossly misinformed, in our view.

A recent Ipsos Mori poll suggests that the U.K. population thinks that immigrants from the EU make up about 15% of the U.K. population and receive about 8% of all child benefits paid out in the U.K.; in reality, they represent less than 5% and receive less than 1% of child benefits. Illustrating the misperceptions of bloated EU bureaucracy, the U.K. population thinks that almost 30% of the EU budget goes to administration (it’s about 6%). When it comes to foreign investment in the U.K., poll respondents think that 30% comes from the EU and almost 20% from China (when in reality almost 50% comes from the EU and just 1% from China.)

The appeal of anti-EU, anti-immigration rhetoric is strongest in the north of England, which failed to participate broadly in economic growth over the past 30-plus years. While the outcome of Thursday’s vote will likely deliver a majority for Brexit in this part of the country, we believe that it remains unlikely that the whole of the U.K.will vote for Brexit.

Outlook

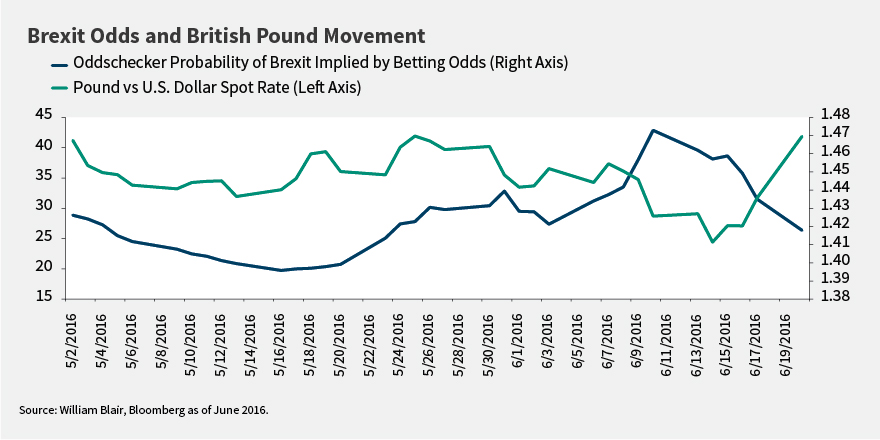

The tightening of the polls over the past weeks, with vote to leave leading several polls as of mid-June, led to a re-pricing of the risk that the British will vote to leave the EU on June 23. However, following the murder of pro-Remain Labour MP (member of parliament) Jo Cox last Thursday and the subsequent decision to suspend the referendum campaign, the bookmaker odds of a vote to leave have fallen substantially and the pound has rallied for the time being. Needless to say, Brexit odds are fluid, and we anticipate continued volatility in expectations and risk assets in the coming days.

Portfolio Positioning

While we remain overweight the U.K.across our international strategies and in line with the benchmark in our Global Leaders strategy, year-to-date we have broadly reduced our exposure to domestically-exposed Consumer Discretionary companies (including auto-related, media, retail, leisure, and homebuilders) and Financials (insurance in particular). These adjustments were largely driven by company-specific fundamentals, valuation risk concerns, and, to a lesser extent, Brexit risk considerations.

We have conducted a comprehensive review of our U.K. holdings across portfolios and analyzed the potential impact of the Brexit and “Bremain” scenarios. We will continue to closely monitor developments in the U.K. and are prepared to make adjustments, either defensively or opportunistically, as we deem appropriate in the context of our quality growth investment approach.

Olga Bitel is the economist at William Blair.

Brexit: Will They Stay Or Will They Go?

June 22, 2016

« Previous Article

| Next Article »

Login in order to post a comment