Charles concludes by noting:

To summarize, if Brexit materializes, there will be dislocation, but it will offer an immense opportunity for those willing to take risks and extend the duration of their views. The end of horror is always better than a horror without end, runs the German saying, and it must be said that they are specialists in this topic. Meanwhile, back at my trading turret, I am being deluged with questions like, “Is the bond market telling us we are going into a recession?” Andrew and I have discussed this point ad nauseam by noting it is all about capital flows. If you are a German insurance company needing to park funds, in Germen Bunds you get a negative return 10 years out on the yield curve, but a positive return in US govies. Even more impressive is the fact that Europeans are buying US munis, but that’s a discussion for another time. (Continued on page 2) “In the law, a proximate cause (aka causa proxima) is an event sufficiently related to a legally recognizable injury to be held to be the cause of that injury.”

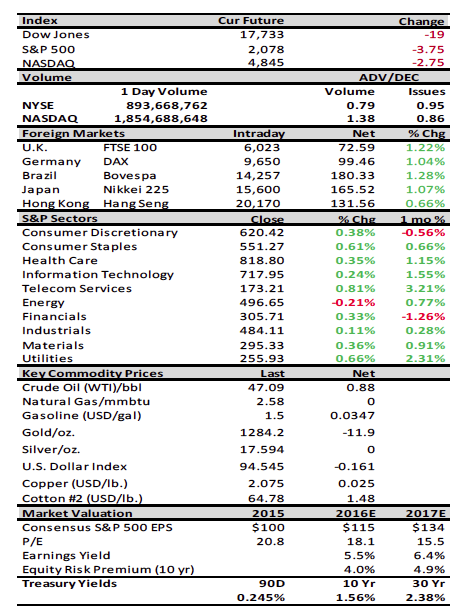

Yesterday, the S&P 500 (SPX/2077.99) retreated to its 2040-2050 support zone following last Tuesday’s MACD very short-term “sell signal”

Jeffrey D. Saut is chief investment strategist at Raymond James.

registered when the SPX closed below 2078.40. That pullback has rebuilt the equity market’s “internal energy”, suggesting a move above the 2080-2082 should produce the “legs,” if the Brexit vote is to “stay,” for a move to new all-time highs. This potential upside “vault” is supported by the extremely oversold reading from the McClellan Oscillator (see chart where green is the MO), the negative sentiment readings, our internal energy indicators, and many other metrics. This morning, the preopening futures are flat; crude oil is up 1.5%; the Brexit vote is tilting towards “stay” as the UK morns the murder of Jo Cox, an advocate of “staying”; and dozens of diplomats urge for military strikes against Syria’s Assad.