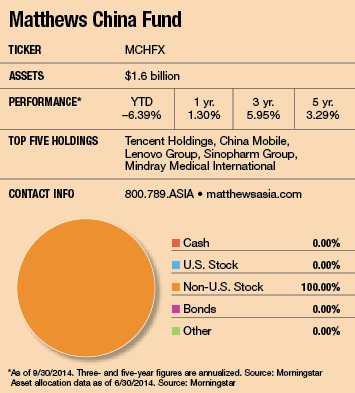

After lagging the u.s. market for several years, China’s stock market seems to be perking up lately, and Richard Gao, manager of the Matthews China Fund, believes investors have reason for optimism. While it’s true that China’s 10%-14% GDP growth in the late 1990s and early 2000s appears unlikely to happen again anytime soon, he says, growth in the 7% to 8% range is a “reasonable expectation.” Furthermore, that growth is becoming more diversified and stable thanks to increasing demand for consumer goods by the country’s growing middle class.

“Years ago, the government relied on infrastructure investments and exports to stimulate growth,” he says. “But a couple of years ago, there was an intentional shift by the Chinese government toward supporting more quality, stable growth through consumption and the service sector.” New rules making it easier for foreigners to invest directly in China’s stock market rather than indirectly through “H” shares listed on the Hong Kong exchange are another draw for investors, he adds.

Investors may also be attracted to stock valuations that are cheap both by historic standards and when compared now with other markets. The MSCI China Index trades at about 9 times forward 12-month earnings, compared with 11 times earning for the MSCI Emerging Market Index and 17 times earnings for the S&P 500 index.

In the past, the country’s stock market was like a caboose that followed the dips and surges of China’s GDP growth. In 2006, for example, when the economy grew 12.7% the MSCI China Index shot up 82.7%. But when growth slowed to 9.6% in 2008, the index lost 51%. And in 2012 and 2013, when GDP rose between 7% and 8%, the index lagged other world markets by a substantial margin. The question now is whether investors can accept slower but perhaps more stable growth as the new normal.

China’s Next Chapter

November 3, 2014

« Previous Article

| Next Article »

Login in order to post a comment