As a result of recent global economic expansion, successful individuals frequently control wealth and earn income in numerous countries around the world. When such individuals desire to become active in philanthropy, they are faced with many choices. They could give to operating charities in a myriad of charitable fields in almost every country, but gift or inheritance taxes in the contributor’s home country may apply.

Not infrequently, however, successful individuals desire to fund a charitable organization they can control, which can fund other charities and charitable causes in their home countries and overseas. When that is the objective, where should the grant-making foundation be formed to provide the greatest degree of flexibility and to maximize the tax advantage? What structure or legal entity is best and what rules will govern its grant-making activities?

The answers to these inquiries must take into account specific traits of the countries considered:

• How difficult or expensive is it to form and qualify a charity in the country?

• What types of legal entities are generally used?

• To what extent can the principal individual providing funding (the donor) or a family member be a director, trustee, employee, contractor, vendor or paid service provider to the charity?

• Are there annual filing requirements?

• Will the donor’s involvement be publicly disclosed?

• Are there investment limitations?

• Will the charity be subject to the country’s income tax?

• Will the donor’s contributions to the charity provide a tax advantage and avoid tax charges?

• What charitable fields may the charity support in the country?

• Can the charity make grants to charities and charitable causes in other countries?

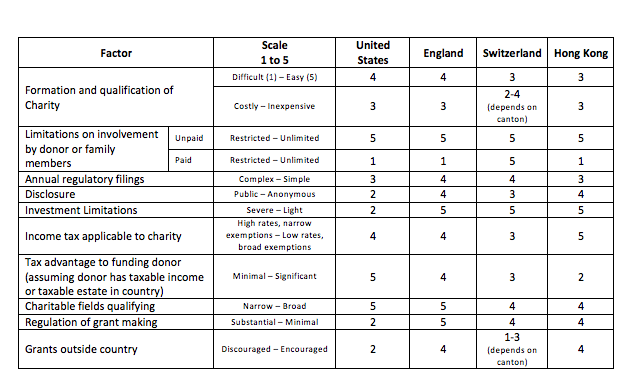

Answering these questions for the several countries that might be considered in a donor’s particular situation is a task for expert counsel. Figure 1 summarizes the law and compares many of the important factors in choosing a jurisdiction in which to form a donor’s charity.

The chart is limited to grant-making, non-operating charities formed in four frequently considered jurisdictions: the United States, England, Switzerland and Hong Kong. (My reference to England instead of the United Kingdom is an acknowledgement that the relevant rules may differ in Scotland and Northern Ireland. The reference to Switzerland is generic—each Swiss canton has its own rules for charitable foundations.) For each of the factors examined, countries are ranked on a rough scale of 1 to 5 , with 5 being the best.

("International Charitable Giving," by Clive Cutbill, Alison Paines, and Murray Hallam, was used as a source for this chart.)

The United States and Hong Kong share a legal history with England, which explains the prevalence of trusts as charitable vehicles in all three countries. Nonprofit corporations (U.S.) and companies limited by guarantee (England and Hong Kong) are also widely used—in some cases more frequently than trusts. In Switzerland, the use of the “Deed of Foundation” as the common choice of entity for a grant-making charity is a distinguishing feature compared to the U.K. and its former colonies.

The U.S. tends to rank highly for the breadth of charitable fields that a qualified charity may support. Hong Kong, by comparison, recognizes only relief of the poor, advancement of education, advancement of religion and “other purposes of a charitable nature beneficial to the community”—the four “heads of charity” inherited from British law before 1997. In Hong Kong, the fourth (and broadest) category may have some requirement for “local benefit,” requiring some application of assets within Hong Kong for public benefit.

Hong Kong’s requirement of local use of assets by such charities and the U.S. requirement that private foundations exercise expenditure responsibility or make equivalency determinations for grants outside the U.S., not to mention the U.S. anti-terrorism restrictions on overseas transfers, leave England and Switzerland as generally more friendly jurisdictions to charitable grants outside the home country. Still, England’s requirement to exercise reasonable due diligence and the local-benefit rules for charities in some Swiss cantons mean that even in those countries, international grant-making should be approached with care.

Overall, it may safely be said that grant-making charities in the U.S. are more heavily regulated than charities in the other countries. The minimum distribution rules, net investment income tax, self-dealing restrictions and public disclosure of annual tax return (including tax return reporting of compensation paid to insiders and of donor identity and contribution amounts) make the U.S. a country of rules and specific requirements for grant-making charities. Compare that with England, which makes no distinction between private foundations and operating charities. None of the other three countries requires grant-making charities to disburse a minimum percentage of asset value per year and none imposes additional requirements (beyond reasonable due diligence) on overseas grant-making.

The U.S. does tend to rank highly when it comes to income tax relief for the charity and tax advantages for donors. Most countries provide exemption from their income tax for the charity’s investment income. The U.S. net-investment income tax (1 percent to 2 percent) and Switzerland’s 4 percent federal income tax do not seriously deter the choice of those jurisdictions.

The donor’s deduction limit of 30 percent of adjusted gross U.S. income with excess carried forward for five years compares favorably to a 20 percent limit in Switzerland with no deduction for the excess. Tax relief based on the fair market value of contributed publicly traded securities in the U.S., England and Switzerland compares favorably to Hong Kong’s deduction, which is solely for contributions of cash (although Hong Kong may offer stamp duty relief on transfers of stock. In any event, capital gains may not be taxable in Hong Kong, which has a relatively benign territorial system of tax). England’s gift aid and so-called share aid produce a tax advantage for the donor similar to that available in the U.S., but only for contributions of cash, publicly listed securities and real property (more on this below). There is no tax advantage for contributions of other assets. By comparison, the U.S. allows a deduction for most appreciated assets other than publicly traded securities in an amount equal to the donor’s tax basis in the asset. When it comes to contributions of real estate, Switzerland provides a deduction based on the market value of the property and England does the same, but only if the real estate is located in the U.K. The U.S. limits the deduction to the donor’s basis for a gift to a private foundation and Hong Kong provides no deduction for non-cash contributions.

The U.S., Switzerland (at the cantonal level) and England have an inheritance tax against which bequests to charity are deductible or exempt. Hong Kong has no inheritance tax—hence no tax advantage to avoiding such tax. Similarly, Hong Kong’s relatively low tax rates mean that most charitable giving there is not primarily motivated by tax relief. Additionally, among these countries, only the U.S. allows tax relief for charitable contributions accomplished via split-interest trusts that provide a financial return to the donor or the donor’s family.

The most important consideration related to tax relief as a motivating factor in the choice of jurisdictions is that, unless the donor is willing to change residency or move income-generating activities, tax relief is only relevant if the donor has taxable income in the country against which to apply the relief or has an estate that will be subject to inheritance tax in the country that can benefit from a bequest to charity. The donor who has income and assets only in the various countries of Europe will generally not find it helpful from a tax perspective to form a grant-making charity in the U.S. or Asia. Moreover, because a charity formed in another country will most likely not be qualified in the donor’s home country, a gift to that charity may trigger a tax charge under the home country’s gift or inheritance tax, as is the case in England. This trap may also catch the unwary donor who contributes to overseas operating charities. Where charitable tax relief is immaterial to a donor, the choice of jurisdiction is considerably widened and certain “offshore” jurisdictions may be attractive to those seeking a light-touch regulatory regime.

It is possible to use a “dual-qualified” structure by which a charity formed in the U.S. creates a subsidiary in Hong Kong or the U.K. and structures the subsidiary so that it will qualify as a charity in those countries, but be treated as part of the U.S. charity for U.S. tax law. This structure is particularly beneficial where a donor is subject to tax in both the U.S. and England or Hong Kong, since this gives the donor income tax benefits in both countries. Pursuant to the effect of court cases applicable in the European Union, family members with income in other EU countries may be able to participate with tax advantage in their countries.

Helping a successful individual choose jurisdictions in which to form a grant-making charity is something like judging a figure-skating competition. Do not let the use of number rankings obscure the fact that the final choice is more art appreciation than number crunching. Reasonable minds may differ on the relative rankings contained in Figure 1. Further, no two philanthropically minded individuals will necessarily agree on what factors are relevant and will certainly weigh the chosen factors differently. Each prospective founder of a grant-making charity will award differing measures of importance to each of the factors, according to the circumstances of that individual’s situation.

Steven J. Chidester is a partner with the law firm Withers Berman LLP in Rancho Santa Fe, Calif.

Michelle Graham in the law firm's Rancho Santa Fe office; Clive Cutbill, Alana Petraske, Richard Cassell and Chris Priestley in the London office; Mimi Hutton in the Hong Kong office; and Paul Roy in the New Haven, Conn., office contributed to this article.