Dallas’s police and firefighters are quitting in droves, wagering that financial-market losses are about to render their promised pensions too good to be true.

With the city considering benefit cuts to help close a retirement-fund shortfall that grew by $1.2 billion last year, more than 200 workers have decided to retire or leave, about double the normal rate, said Mayor Pro Tem Erik Wilson, who sits on the Dallas Police and Fire Pension System’s board. That’s threatening to put further pressure on the fund as benefits come due, including lump-sum payouts to older employees who’ve been drawing a paycheck while earning a guaranteed 8 percent return on their pensions.

“I’ve had 40 to 50 officers in my office this week asking what they should do,” said James Parnell, 52, secretary-treasurer of the Dallas Police Association and 25-year veteran. “They’re very nervous about what is going to happen, they’re fearing a run on the money.”

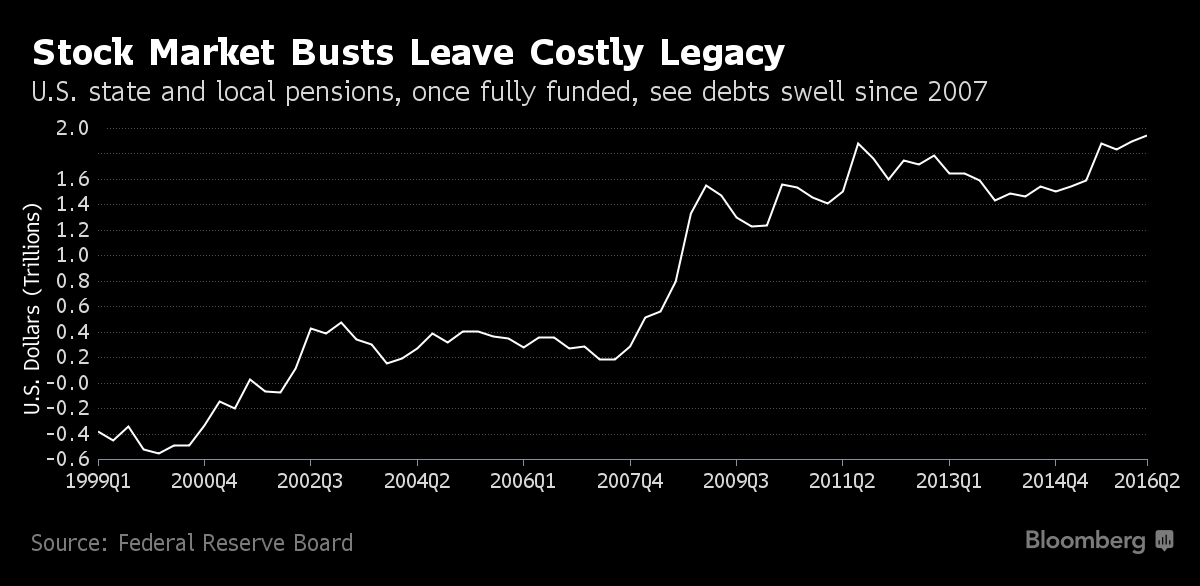

Turmoil in world stock markets and near record-low bond yields are taking a toll on pensions for cities like Dallas, which count on annual investment returns of more than 7 percent to cover promised benefits. In the year through June, U.S. state and local-government plans posted the smallest gains since 2009, leaving them with about $2 trillion less than they will eventually need, according to data from the Wilshire Trust Universe Comparison Service and the Federal Reserve.

The squeeze on Dallas’s fund is even more acute because of a decision to divert money from stocks and bonds into Hawaiian villas, Uruguayan timber and undeveloped land in Arizona, among other non-traditional investments. The strategy, put in place under prior managers, backfired. The fund lost 12.6 percent in 2015 and 0.7 percent over the past three years.

That’s left the city under pressure to boost contributions or find ways to reduce benefits to make up for the gap. In November, Standard & Poor’s downgraded Dallas’s bonds by one step to AA, the third highest grade, citing the need to address the rising liability to the 9,600-member fund. Mayor Mike Rawlings has proposed putting off a voter referendum on an $800 million bond sale for infrastructure projects until the city comes up with a fix.

On Monday, dozens of city employees and retirees packed into a meeting where officials discussed options for dealing with a possible liquidity crisis brought on by the increase in retirements.

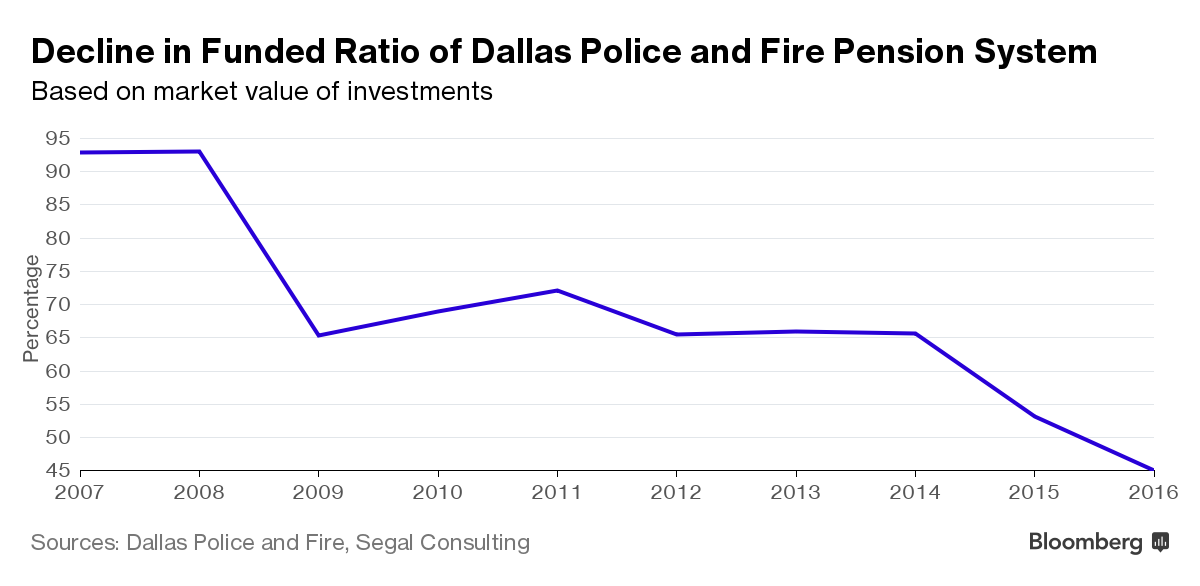

The public-safety system has just 45 percent of the assets it needs to cover benefits, down from 64 percent at the end of 2014 and half what it was a decade ago. The pension could be out of cash in 15 years at the current rate of projected expenditures, according to a Segal Consulting report in July.

City and pension officials are planing to inject more taxpayer money into the pension and may roll back some benefits, including annual cost of living increases and the program that allows workers to rack up lump-sum payouts for staying on the job after they’re eligible to retire.

“Everyone is going to have to give something for this to be successful,” said Wilson, the mayor pro tem. “We’re actively working to make sure the pension survives. We’re exhausting every option.”