In Part 2 of our Federal Reserve (Fed) rate hike playbook, we assess how municipal bonds have fared during periods of Fed rate increases. In the first full week of trading for 2016, Fed rate hike expectations declined in response to another bout of Chinese economic concerns and a benign message from the Fed meeting minutes, which appeared to cast doubt on whether the Fed would ultimately follow through on its forecast of roughly four rate increases in 2016. Still, a strong employment report late last week kept Fed rate hikes in play as a factor in 2016, even if market participants began to express doubt.

History does not always repeat and a closer look may reveal whether history may rhyme or take a different path.

Municipal Bonds & Rate Hikes

The Barclays Municipal Bond Index has underperformed the taxable Barclays Aggregate Bond Index, on average, during the subsequent 6, 12, and 18 months following a first interest rate hike [Figure 1]. However, the broad Municipal Index is more interest rate sensitive than the taxable Aggregate Bond Index. The average duration, a measure of interest rate sensitivity, for the taxable bond market is 5.5 years versus 6.2 for the Barclays Municipal Index (Barclays data, as of January 8, 2016). Over time, average interest rate sensitivity of each index has varied, but the broad municipal bond market index has consistently maintained a longer duration.

Performance relative to taxable bonds improves using the Barclays 10-year Municipal Index, which has an average duration of 5.8 years, very similar to that of the taxable benchmark, which makes for a more relevant comparison [Figure 1]. Using the 10-year index, municipal bonds outperformed over the first 6 months before lagging slightly after 12 months, and underperforming taxable bonds after 18 months.

The performance disparity of municipal bonds relative to taxable bonds is relatively small, however, and generally follows the broad bond pattern of a difficult first 6 months, followed by modest improvement, and then price strength after 12 months, as Fed rate hikes slowed the economy and lowered inflation risks. The greater performance disparity occurs after the 18-month period, which is not uncommon as municipal bonds have often lagged Treasuries during periods of price strength and declining yields.

Distinguishing Cycles

A closer look at each of the three past rate hike cycles shows mixed and inconclusive results. Municipal bonds lagged during the Fed’s aggressive 1994 campaign, were roughly in-line with taxable bonds during the 1999 campaign, and outperformed notably during the 2004 campaign.

We, and most market participants, do not expect an aggressive rate hike campaign, which would make a repeat of 1994 unlikely. Conversely, municipal bonds entered the 2004 rate hike campaign more attractively valued as the implementation of tax cuts pressured municipal bonds in 2003. Municipals began the 2004 rate hike campaign, on better footing, which helped offset the impact of rate hikes. In fact, municipal bonds thrived during the 2004 campaign enjoying returns in excess of 5% during the 6, 12, and 18 months after the first rate hike (Barclays Index data). Municipal bonds benefited during that period from the presence of institutional investors who purchased intermediate- and long-term municipal bonds with borrowed funds, creating strong demand. This source of demand is unlikely to repeat in the current cycle as leveraged investors have failed to return.

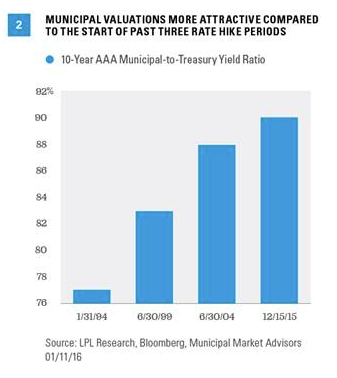

However, municipal bonds enter the current rate hike period more attractively valued compared with any of the prior three rate hike cycles, including 2004. Average municipal-to-Treasury yield ratios are higher now compared with those prevalent at the start of interest rate hikes in 1994, 1999, and 2004 [Figure 2]. The higher the ratio, the more attractive municipal bonds are relative to Treasuries, and vice versa.

Valuation differentials alone will not ensure municipal bond resilience in the current rate hike cycle, but two additional factors may lend support to municipal bonds:

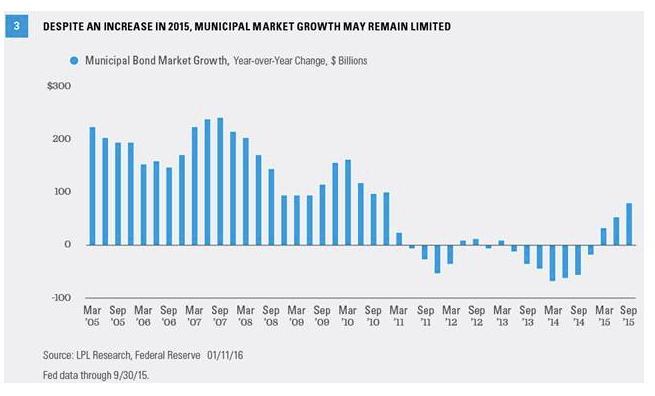

· Limited supply. Net growth of outstanding municipal bonds remains anemic. While the overall market for municipal bonds began to grow in 2015 [Figure 3], the growth rate remains very modest at 2% as of September 30, 2015. Tight supply—a factor that has supported municipal bond performance in recent years, and is responsible for a strong start to 2016—is likely to be a factor again in 2016 and beyond. State revenue has rebounded notably from the recession but has only slightly outpaced expenses, constraining capacity to take on new debt.

· Higher taxes. Unlike the early 2000s when lower tax rates posed a threat, higher tax rates may continue to support municipal bonds. Federal tax rates are unlikely to increase, but localized tax increases—such as those recently enacted in Chicago to help meet pension obligations and California’s tax increase in 2013—may boost the allure of municipal bonds. The tax exemption for municipal bonds may also continue to come under fire in Washington, as it has for decades, but until a viable substitute for municipal debt is workable (which remains far away), the tax treatment of municipal bonds is unlikely to change.

Anthony Valeri is investment strategist for LPL Financial.