As the real estate market continues to struggle, one bright spot has proved surprisingly robust over the last year. After a sharp downturn in 2008 and early 2009, securities issued by publicly traded real estate companies have staged a powerful recovery. As of mid-July, the Vanguard MSCI U.S. REIT Index ETF was up more than 72% for the trailing year, while the S&P 500 index was up only 25%.

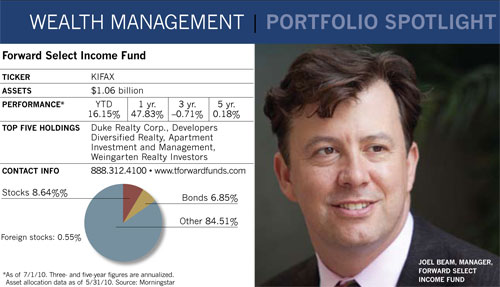

The $1.06 billion Forward Select Income Fund, which invests mainly in REIT preferred stock, has followed a similar pattern. In 2008, the fund fell 40.5%. But it was up 75% in 2009, and is outperforming the S&P 500 index so far this year. Its 30-day SEC yield was recently close to 9%.

Joel Beam, the 40-year-old manager of the fund, says that common and preferred REIT shares reached such depressed levels last year that the bargains were hard to resist. In late 2008 and 2009, when the market was scraping bottom, he loaded up on those high-quality real estate companies he felt had been too pricey before the downturn. Forward Select Income often uses leverage to magnify buying power, and Beam borrowed heavily during the trough.

Since then, many of the stocks he bought have rebounded sharply.

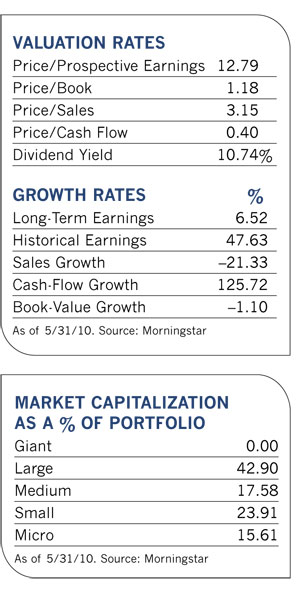

Even though preferred REIT shares are more expensive than they were early last year Beam believes they still represent a good value by several measures. Many are trading at a discount to par. (Among preferred REITs, par value refers to the traditional offering price of $25 a share.)

Another measure of value, the yield spread between risk-free ten-year Treasury notes and preferred REITs, is still fairly wide. In July of this year, the Wells Fargo Hybrid and Preferred Securities REIT Index yielded 525 basis points more than the Treasury securities, well above the long-term average of 366 basis points. "At a minimum, the wide yield spread indicates the securities are not overpriced," he says.

Preferred stocks, the fund's mainstay, are a hybrid stock-bond investment paying a specific dividend that does not change. They are higher in the securities pecking order than common stock because if a company defaults, holders of preferred shares are ahead of stockholders (though behind bondholders) for payment. Issuers must also pay preferred dividends ahead of common stock dividends.

Common stock REITs tend to have a somewhat higher total return, he says, although a larger component of total return on the preferred stocks comes from yield. From its inception in March 2001 through the end of June, Forward Select Income has produced an 8% annualized total return, much of that coming from the yield component.

Beam observes that financial advisors often tell him they have trouble wedging preferred securities into their asset allocation models. "I tell people to look at preferred shares of real estate investment trusts as an alternative income vehicle. In terms of a risk profile, I'd say they are closer to junk bonds than anything else. But their default rate is actually lower."

While the last couple of years have been highly volatile for preferred REIT shares, Beam says that they are normally a tamer security than REIT common shares and have a relatively low correlation to other investments. They have a 0.78 correlation to REIT common stocks, a 0.66 correlation to preferred stocks and a 0.18 correlation to bonds.

While Beam cautions that REIT preferred shares aren't appropriate for a retiree who can't afford to ride out the volatility in the market, "They may be worthwhile for someone who has a long time horizon and wants to get much of their total return from a fairly reliable stream of income." He says missed dividend payments are rare among portfolio companies, although a couple of hotel holdings skipped their dividend payments in late 2008 and early 2009.

To find preferred securities he likes, Beam evaluates an issuer's enterprise value, which reflects the breakup value of a business. He also looks at fixed charge coverage, which gauges the company's ability to pay bond interest and preferred stock dividends with cash flow.

"REITs are more transparent and easier to understand than most companies, he says. "Sometimes it's hard to figure out what's really going on by looking at a typical company's 10-K. But to me, commercial real estate is a very understandable business."

Beam's comfort level in evaluating REITs comes from years of experience in the real estate business. As an undergraduate student at the University of California at Berkeley, he held a clerical job at a local real estate developer, where he spent time answering phones and learning about construction and leasing contracts.

After graduation, he was responsible for the valuation and pricing of real estate limited partnership and institutional commingled investment fund securities, as well as the underlying properties, for a firm called Liquidity Financial Advisors. He moved to the securities side of the business when he joined Kensington Investment Group in 1995 as a senior analyst, and began managing portfolios of real estate securities in 1997. When Forward Management bought Kensington in 2009, he continued managing the fund under the acquirer's name.

Despite the REIT run-up since the name change, Beam sees plenty of weakness in both the commercial and residential sectors of the market. Nationally, the vacancy rate for offices is 17%, its highest levels since the early 1990s. In many parts of the country, strip malls are dominated by empty storefronts. And residential real estate continues to struggle with high foreclosures and delinquent mortgages. "But you have to differentiate by sector, property type and location," he says. "There is a big difference between trying to lease an office building in a low-demand area than downtown office space that's on top of a subway station."

As real estate investors await better days, public real estate companies are in a better position to weather the downturn than private firms, says Beam. Since they don't have access to the public capital markets, the latter must rely heavily on bank loans for expansion, which have been difficult to obtain with tougher lending restrictions. Over the next several years, the firms will need to refinance mortgages used to fund boom-time projects from the mid-2000s. "With property values way down, that's going to be a big problem," Beam observes.

By contrast, publicly traded REITs have better access to capital through the public markets. And with investors enthusiastic about their shares, many portfolio firms have successfully launched new issues over the past year.

"Access to capital means public real estate companies have the wherewithal to weather the soft operating environment and the effects of the recession," says Beam. "With double-digit vacancy rates in many parts of the country, these firms still have the means and the muscle to attract and keep tenants. They also have the capital to buy assets at today's attractive prices."

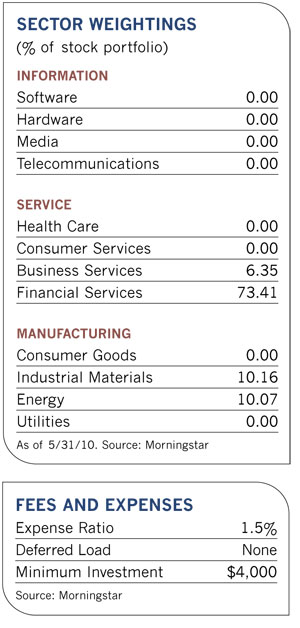

Beam likes to run a broadly diversified portfolio that spreads its bets among a variety of sectors and locations. The fund owns 135 different securities with exposure to 71 issuers.

Retail, office and specialty REITs each make up about one-quarter of the fund's assets. One of the specialty REITs is LTC Properties, which acquires properties and leases them to long-term care providers and has more than 200 nursing home and skilled care facilities spread throughout the country. Beam labels it "one of the best-performing REITs since its first public offering in the late 1990s." He also likes the company's low debt, as well as the fact that management has been buying back the company's common and preferred stock.

Another major holding, Duke Realty Corp., specializes in office and industrial properties in the Midwest and on the East Coast. Although the company has more debt than some of its competitors, and the markets it specializes in are still somewhat soft, Beam believes that the firm's financial picture will improve once it raises more equity in the public market.

CommonWealth REIT, the fund's fifth-largest holding, owns a portfolio of office and industrial properties around the country. Beam says that the firm is more protected from downside risk than some of its competitors because its leases pass expenses through to tenants and have fairly long durations.

Residential REITs represent about 9% of the portfolio. Beam likes the apartment business, since the supply of available apartments has dwindled and rents are trending up as people become disenchanted with home ownership. The fund's fifth-largest holding, Apartment Investment & Management, takes advantage of the trend by acquiring and managing affordable apartment complexes throughout the U.S.

Despite continued weakness in the real estate market, Beam sees better times ahead, though he admits they may be a few years off. "I've gone from chief grouch here to chief cheerleader," he says. "I believe the government stimulus headed off what could have metastasized into a calamitous situation.

Eventually, I think those efforts will yield great results."