Key Points

• Municipal bonds issued in your home state are generally exempt from state income taxes, while munis from other states are usually subject to state income taxes.

• Limiting your muni holdings to in-state issuers only may reduce your state income tax bill, but could also leave you concentrated in issuers with similar risk characteristics.

• Consider adding municipal bonds from other states for added diversification benefits and potentially higher yields.

As summer heats up, you might be thinking about traveling outside your home state. Should your municipal bond portfolio do the same? That depends on a few things.

Munis’ main attraction is that they generally provide tax-advantaged income. Interest payments on most munis are generally exempt from federal income taxes, and those from your home state may also be exempt from state income taxes (assuming your state has such a tax). Those state tax advantages generally don’t extend to munis from other states, though. While that may seem like a compelling argument against investing in muni bonds outside your home state, there are situations where national diversification makes sense.

Here are five situations in which you could consider munis from other states.

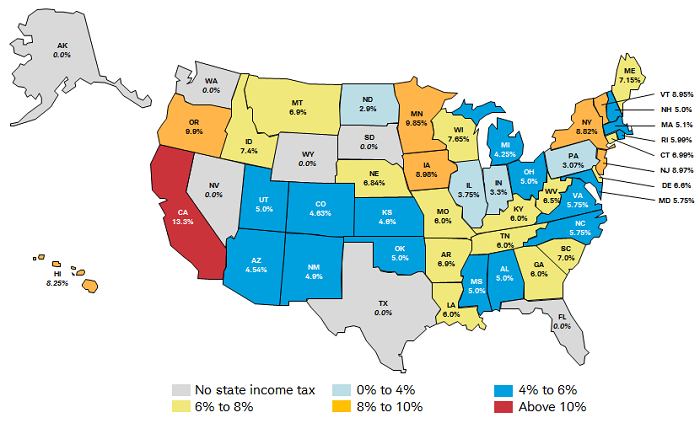

1. You live in a state with low or no income taxes. If you live in a high-tax state like California (top marginal income tax rate: 13.3%) or New York (top marginal income tax rate: 8.82%), then the tax benefits from home-state munis can be significant. However, if you live in a state with low or no state income taxes, then there is little or no tax incentive to staying within your home state.

The map below shows the maximum marginal income tax rate by state, if married filing jointly.

Top marginal income tax rates by state

Source: TaxFoundation.org, as of 2/8/2016.

Of course, even if you live in a low- or no-income-tax state, you might not be comfortable venturing into another state’s muni market. For example, an investor in Texas may not be familiar with issuers or credit conditions in other states, so it might make sense to work with a bond specialist or use a professionally managed fund to help navigate credit differences in bonds outside your home state.

2. You could earn a higher yield, even without state tax breaks. Diversifying outside of your home state could help you boost the yield on your muni bond portfolio, even after accounting for any state income taxes. And that includes residents of higher-tax states.

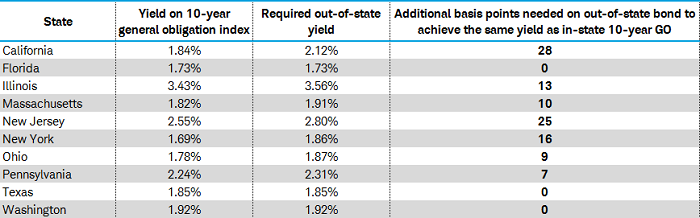

It depends on where you look, though. The table below shows how much more yield investors in certain states would have to earn on out-of-state munis compared with the yield on an index of 10-year general obligation bonds from their home state to make up for the lack of state-income-tax breaks. The investors are in their home states’ highest marginal state tax brackets, and the difference in yield is expressed in basis points (hundredths of a percentage point). Note that Florida, Texas and Washington don’t have state income taxes, so there’s no spread.

Required out of state-yield to achieve the same after-tax in state yield for select states

Source: Bloomberg, as of 5/3/2016

Note: Assumes the highest marginal state tax rate. Yields may be due to different characteristics such as credit quality and call characteristics. States are selected because they represent the top 10 largest issues in the Barclays Municipal Bond Index. For illustrative purposes only.

To call out one example, the yield on the 10-year California general obligation bond index is 1.84%. A couple in the highest marginal tax bracket would have to earn a yield of at least 2.12% on a bond from outside of California to achieve the same after-tax yield as the in-state bond. That could be possible with a bond from Illinois, New Jersey or Pennsylvania. Of course, higher yields generally also mean higher risks, so investors should keep that in mind.

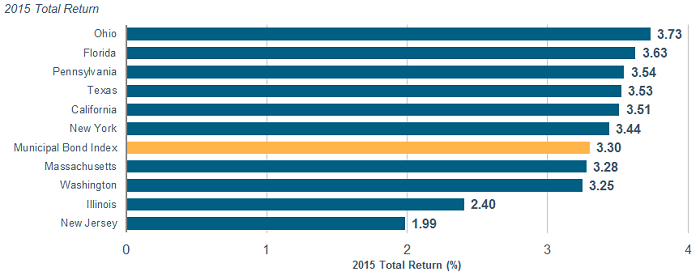

3. You could also earn higher total returns on munis from other states. If you’re investing in other states’ munis through a bond fund or actively managed account, the fund manager could identify higher-yielding and potentially undervalued securities to help drive returns. Remember, returns from actively managed muni portfolios come from two primary sources: interest payments and changes in prices.

Changes in economic conditions among the different states can affect credit conditions, which could affect bond prices in turn. Some state-specific funds—California, for example—have benefited recently from improving credit quality and higher prices. Other state-specific funds, like New Jersey, have been hurt by deteriorating credit quality and falling prices.

Returns by state

Source: Barclays, as of 12/31/2015

Note: States are selected because they represent the top 10 largest issues in the Barclays Municipal Bond Index. Performance data quoted represents past performance and does not indicate future results.

4. Economic conditions in your home state may make munis in other states more attractive. The muni market is big—there are approximately $3.6 trillion of muni bonds outstanding,1 with more than 12,400 different obligors rated by Moody’s Investors Service2—and the credit quality of each state and issuer could be impacted by different economic conditions or sources of revenue. If the conditions in your home state aren’t favorable, other states’ bonds might be more appealing.

For example, we believe it might make sense for investors living in states where municipalities all share similar political, geographic and economic risks to think about diversifying into other states to reduce these risks. Credit quality is generally stronger in areas with steadily increasing populations, skilled workforces and diverse economies. Today, we are more cautious on issuers in the aging industrial centers and areas that rely heavily on the oil and gas industry. Again, munis from a state where conditions are improving could see their prices rise, which could drive total returns. Such returns could make up for the potential loss of any state tax advantages.

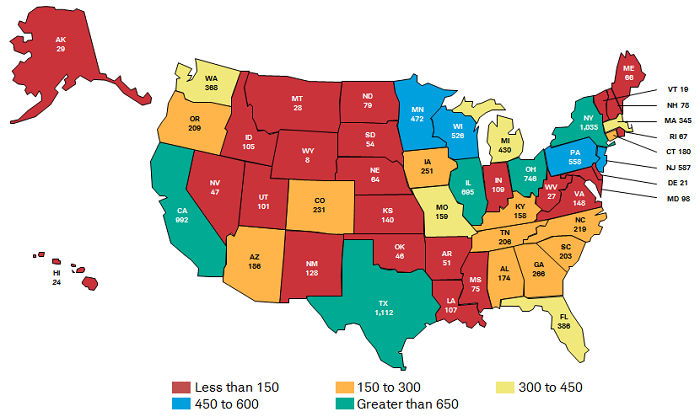

5. There may not be enough issuers in your state to build an adequately diversified portfolio. For adequate diversification, we recommend holding at least 10 different bonds from issuers that do not have similar credit characteristics. This could be difficult to achieve in a state-specific portfolio, especially if you live in a state with a relatively small number of issuers who are all exposed to similar risks. States with a large inventory of bonds from issuers with different credit characteristics, like California, may not present this problem. Achieving diversification is generally easier in states with larger inventories of bonds outstanding.

Moody's rated obligors by state

Source: Moody’s Investors Service, as of 2/8/2016.

What to do now

There are no hard-and-fast rules about where and when to invest in munis from outside of your home state. If you’re in a high-tax state, you may still be able to find attractive after-tax yields and increased diversification by looking at munis from other states. Alternatively, if you’re in a low-tax state, you may not feel confident enough about credit conditions elsewhere to make an investment.

That said, here are a few more suggestions:

• If your state has high income tax rates, consider building a portfolio of individual state-specific bonds with the help of a Schwab Fixed Income Specialist. You could also consider a state-specific bond fund from the OneSource State Tax-Free Bond Fund List. Prior to investing in a state-specific bond fund, we suggest you review the prospectus, and especially the top 10 holdings, to make sure you’re comfortable with all the municipalities represented.

• If your state has low income tax rates, consider building a portfolio of individual national municipal bonds. You could also consider a national fund from the OneSource Select List.

• Even if your muni portfolio is mostly made up of bonds from your home state, consider adding bonds outside of your home state for the diversification benefits and potentially higher after-tax yields.

1 Bloomberg, as of 5/9/2016.

2 Moody’s Investors Service, as of 2/8/2016.

Cooper J. Howard, CFA, is senior research analyst, fixed-income and income planning, at Charles Schwab & Co.

Rob Williams is director of income planning at the Schwab Center for Financial Research.