Since 1950, the United States has experienced both the worst bear market for bonds in its history—and the greatest bull market.

The bear market happened first and can be traced to that year. On the first day of 1950, a 10-year U.S. Treasury bond yielded 2.32%. The minimum wage was 75 cents an hour, and a first class postage stamp cost 3 cents. From 1950 through 1981, many investors purchased bonds with locked-in interest rates. Those who needed to sell the bonds before maturity lost value.

But by the first day of 1982, things had changed. The yield on a 10-year U.S. Treasury bond had climbed to 14.59%. The minimum wage had risen to $3.35, and a first class postage stamp cost 20 cents. From 1982 through 2013, a record decline in interest rates was a boom for investors. Many received a guaranteed rate of return on the bonds in their portfolios, and realized appreciation in the value of those bonds as interest rates fell. The greatest bond bull market for secondary investors in our nation’s history had begun, and long-term bond investors reaped the benefits for three decades.

Now times have changed again. By the first day of 2013, the yield on a 10-year U.S. Treasury bond had fallen to 1.9%. The minimum wage was $7.25, and a first class postage stamp cost 46 cents (if you even need one in the age of electronic mail). On the first day of 2015, the yield on a 10-year U.S. Treasury bond was about 1.9%. In the middle December 2015, rates started to rise but have since fallen back.

Rising rates could increase portfolio risk for many investors buying bonds today since bond values in the secondary market tend to decline in such environments.

So now investors are in a quandary.

A New Mix

Uncertainty about the future of interest rates has many advisors assessing the performance potential of different portfolio components. Are investors better off holding on to their bonds? Or can risk-adjusted performance be improved by adding equity-linked fixed-income alternatives, such as fixed-index annuities, to portfolios?

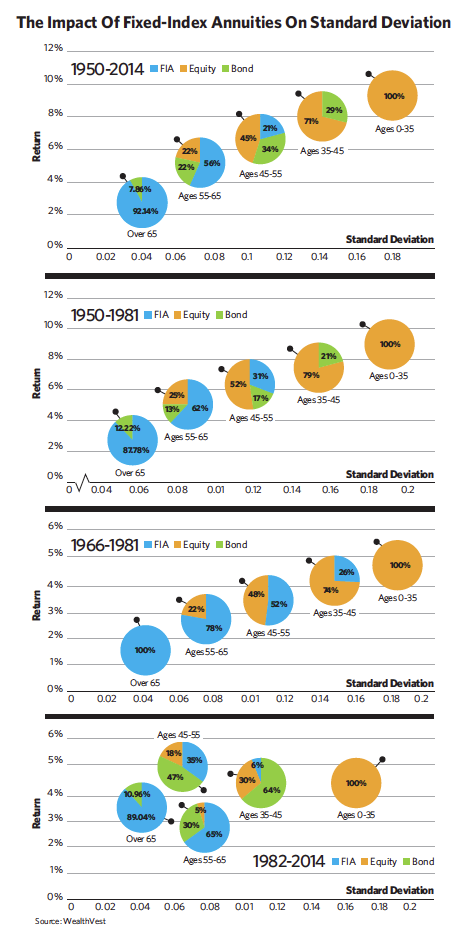

To help answer this question, we measured the performance of portfolios with different combinations of stocks, bonds and fixed-index annuities (their returns without reinvested dividends) to determine the various risk-adjusted returns. (The study used a hypothetical fixed-index annuity with an S&P 500 index-linked interest crediting method. It used a 6.25% annual point-to-point cap or 2.75% monthly point-to-point cap to approximate annuity returns for the time period between 1950 to 2013.)

Then we measured the historic performance of each of these portfolios—from 1950 through 2013, a period that encompassed a wide range of financial market conditions—by calculating their Sharpe ratios after the fact. The Sharpe ratio helps determine whether a portfolio’s performance can be attributed to wise investment decisions or excessive risks. The higher the Sharpe ratio is, the better the portfolio’s risk-adjusted performance. As a general rule, portfolios that perform well provide higher returns without taking too much additional risk.

One of our key findings was that investors who want to avoid losses in the years immediately before retirement or during retirement may be able to reduce overall portfolio risk and optimize performance by adding the fixed annuities to their portfolios. During periods of rising interest rates, adding fixed index annuities and reducing or eliminating bond exposure helped improve both Sharpe ratios and risk-adjusted performance. Particularly, it helped to add the annuities to portfolios during the period from 1966 to 1981, when interest rates were rapidly rising.

It’s important to understand that an efficient portfolio is not a constant. Different combinations of investments deliver optimal risk-adjusted performance based on different performance relationships in the underlying investments. Before proceeding, we should note that portfolio optimization techniques can produce asset allocations that many advisors and their clients would not accept. No doubt this is true with fixed index annuities. In the analysis that follows we are discussing theoretical models, not actual allocations.

The first period we measured encompassed both bear and bull markets for bonds. From 1950 to 2014, returns on the portfolios we constructed ranged from 4.18% (when the portfolio was made up of 94.3% fixed-index annuities and 5.7% corporate bonds) to 10.56% (with a portfolio of 100% equities).

The fixed-index annuities helped risk-adjusted performance during a period that included both rising and falling interest rates.

1950-1981 (a period of rising rates). Next, we identified the portfolio constructions that delivered optimal performance between 1950 and 1981. The various portfolio mixes produced returns between 3.63% (when the mix was 14% corporate bonds and 86% fixed-index annuities) to 10.08% (when the portfolio held only equities).

During this period of rising interest rates, fixed-index annuities improved a portfolio’s risk-adjusted performance. This was an important finding because periods of rising interest rates can inflict significant losses on a portfolio with bonds if an investor sells those bonds before maturity. By increasing the percentage of fixed-index annuities or equities in a portfolio, an investor may be able to reduce the negative effects of rising interest rates.

1966-1981 (when interest rates rose sharply). We also chose to measure portfolio optimization during a period of steeply rising interest rates because it appears the United States may be on the verge of a similar trend. From 1966 to 1981, our portfolio constructions provided returns that ranged from 3.12% (when corporate bonds made up 5% and fixed-income annuities contributed 95%) to 5.44% (with a portfolio of 100% equities).

During a 15-year period of sharply increasing interest rates, fixed-index annuities reduced risk and increased the Sharpe ratio of a portfolio. Adding the annuities protected the premium while preserving positive returns during a time when bond investors generally experienced negative ones. This period—when interest rates rose from a relatively modest level to double digits—proved to be the most important in our study. Fixed index annuities, which can provide a source of fixed income, may provide premium protection during periods of rising interest rates while balancing the investor’s need for return.

1982-2014 (when rates declined). Finally, we identified the portfolio constructions that delivered optimal performance between 1982 and 2014. The various portfolio mixes produced returns between 4.59% (22% corporate bond and 96.3% FIA) to 11.03% (100% equities).

During the longest and steepest period of interest rate declines in U.S. history, increasing the amount of premium in FIAs held in a portfolio reduced overall risk and optimized performance. Since falling bond yields means appreciation for bonds, we hypothesized that the FIAs would be a smaller percentage of the portfolio and that bonds would be larger.

A critical intellectual pillar of portfolio management is the study of the efficient frontier. By optimizing portfolios, advisors can deliver levels of return that are commensurate with investors’ risk tolerance. That, in turn, may help advisors address two of investors’ worst fears about retirement. But remember, the above allocations refer to theoretical models.

No 1. Losing Retirement Savings

When it comes to balancing risk and return for retirement savings, Americans tip toward the cautious end of the spectrum. During 2014, 64% of all investors participating in a national survey indicated they would prefer a secure investment even if potential for growth were low. A separate survey found that the vast majority of investors have become less comfortable with investment risk during the past 10 years. About 55% are uncomfortable with the idea of putting any of their savings at risk, and less than one-fourth indicated they could tolerate the loss of 5% of their savings.

No. 2 Outliving Retirement Savings

Not too long ago, Social Security benefits, pension plan income and personal savings provided steady income that retirees could rely on receiving throughout retirement. Today, pension plans are rapidly disappearing, and worries about inflation, high health-care costs, inadequate savings and other issues have many investors worried they will outlive their savings during retirement. In fact, the possibility of outliving their retirement savings frightens them more than the prospect of dying.

The best solution, then, is for them to optimize their portfolios so they receive the greatest potential return for the level of risk they are willing to incur. Fixed index annuities may help with this optimization.

Still, efficient frontier modeling does not take into account a product’s liquidity or other issues important to investors. Like structured notes, fixed index annuities are dependent on the underlying credit quality of the issuer or insurer. Investors should also consider the overall suitability of the annuity, such as the ability to meet liquidity needs in light of surrender charges and other restrictions, limitations and risks.

Wade Dokken is co-founder and co-president of WealthVest Marketing and the author of New Century, New Deal, a public policy analysis of the challenges facing Social Security in the coming decades.

Jack Marrion is president of a research consultancy that publishes the Index Compendium newsletter, the consumer education materials of Safe Money Places, and the Advantage Compendium research studies. He has an MBA from the University of Missouri and has conducted doctoral studies in the area of cognitive bias in decision-making.