When the Federal Reserve raised its benchmark interest rate in December, the prevailing mood music was that the move probably presaged four more increases -- one per quarter -- in 2016. But with global stock markets in a tailspin and the economic backdrop deteriorating, recent comments from European Central Bank President Mario Draghi and Bank of England Governor Mark Carney suggest Janet Yellen might end the year with a monetary policy not that far from where it started.

In the wake of the Fed's Dec. 16 quarter-point hike in the upper rate of its target rate to 0.5 percent, traders started to anticipate the Fed's next moves. By the end of last month, prices in the futures and options markets suggested a better than 50 percent chance that the central bank would raise rates again at its March 16 meeting. Here's what's happened to those expectations in the past few weeks:

Given the worsening outlook for global growth, it's no surprise that traders are scaling back expectations for how quickly the Fed might move. Here's how Carney at the U.K. central bank described the current environment in a speech on Jan. 19:

Now is not yet the time to raise interest rates. The world is weaker and U.K. growth has slowed. Due to the oil-price collapse, inflation has fallen further and will likely remain very low for longer. Further downside risks to the global outlook remain, reflecting the ongoing challenges in China, fragilities in other major emerging market economies and the potential for contagion.

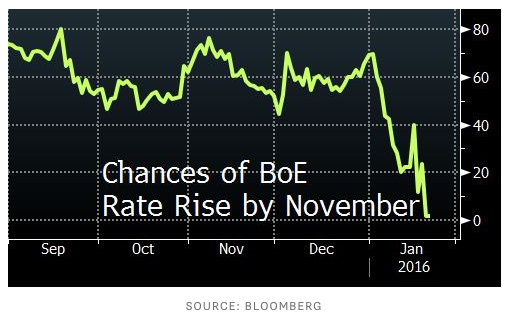

The change in the outlook for U.K. interest rates has been even more dramatic than for U.S. policy. At the start of the year, higher borrowing costs by November were a done deal, according to market prices. In the past three weeks, those expectations have been wiped out:

While traders are anticipating that the U.K. central bank won't tighten monetary policy in the coming months, the ECB is making no secret of its intention to loosen its policy even further. At his regular press conference on Thursday, Draghi said "downside risks" have increased since the start of the year, and his institution will have to consider changing its stance at its next meeting in March. "We are doing whatever is necessary to comply with our mandate," he said.

So far, though, inflation in the euro zone is drifting further away from the ECB's 2 percent target, as this chart shows: