Most people won't be prepared for retirement at age 65, but they will be by age 70, largely because of increased Social Security payments, concludes a report by the Center for Retirement Research at Boston College.

Written by Alicia H. Munnell, Anthony Webb, Luke Delorme and Francesca Golub-Sass, the report, National Retirement Risk Index: How Much Longer Do We Need To Work? finds more than 85% of households would be prepared for retirement by age 70. "Many people will need to work longer than their parents did, but they will still be able to enjoy a reasonable period of retirement, especially as health and longevity continue to improve," the report says.

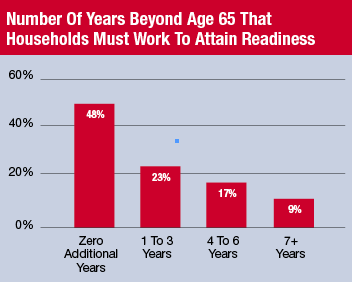

The authors reached their conclusion by constructing a "national retirement risk index" measuring the share of American households that may not be able to maintain their previous standard of living after retirement. Using 65 as the age for retirement, the NRRI shows that 51% of today's working households would not be able to maintain a preretirement standard of living in the wake of the Great Recession and financial crisis.

Note: An additional 2.8% of households in the sample would not be ready by age 90.

Source: Center for Retirement Research at Boston College

The center builds the index by projecting the rate at which a sample of U.S. households would be able to replace their income in retirement, constructing a target replacement rate to maintain a preretirement standard of living and comparing the projected and target rate to find the percentage of households "at risk."

The authors acknowledge that people don't need as much income to maintain their standard of living in retirement because more of it can be devoted to spending-once people stop working they pay less in taxes, no longer need to save for retirement and often have paid off their mortgage.

The index shows that only about 30% of households are ready for retirement when the retirees are age 62, the earliest age at which they can take Social Security. "The steep improvement in readiness from ages 62 through 70 and the leveling off thereafter reflect the importance of Social Security and the pattern of benefits payments," the report says. Social Security increases by about 8% per year between ages 62 and 70, after which benefits remain constant in real terms.

The report also shows how important Social Security is for low-income households, which derive the bulk of their income from the benefits payments. At age 62, 38% of high-income households are financially ready to retire compared with 20% of low-income ones. By age 70 though, low-income households are nearly as prepared for retirement as high-income ones (82% versus 88%).

Another notable finding: Households with younger people are less prepared for retirement than those with older ones. In 2007, households headed by individuals from 50 to 59 years old were projected to be twice as likely to be able to retire at 62 than those headed by 30- to 39-year-olds (40% versus 20%). At age 70, the gap closes, but is not eliminated: 89% of 50- to 59-year-olds would be ready while 82% of 30- to 39-year-olds would be.

Why are younger people less prepared? The report cited three main reasons: They'll need more assets in retirement since they are expected to live longer; they face a higher full-retirement age for Social Security; and fewer are covered by defined benefit plans and don't appear to be saving more in 401(k) plans relative to their income than older people.