• Global growth looks increasingly sluggish.

• Countries that are not dependent on commodity exports are well positioned.

• We expect sustainable growth from Eastern Europe, Mexico and India.

Global emerging markets have faced significant headwinds over the last few years, primarily as a result of the slowdown in Chinese growth and significant falls in commodity prices. More recently the expectation of US rate hikes has also negatively affected sentiment. However, as global growth looks increasingly sluggish, monetary conditions in developed countries are likely to remain accommodative for a prolonged period of time.

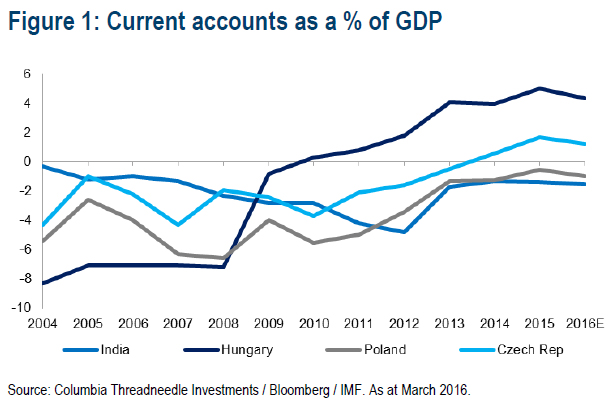

We believe the current tightening cycle in the US is likely to be very shallow, alleviating pressure on emerging market countries as the cost of attracting foreign capital remains low. In particular, those countries that are not dependent on commodity exports and have shown improvement in their external accounts over the last few years will be well positioned to benefit from domestic-led growth.

In our portfolio, we have recently increased exposure to consumer stocks in such countries, which include Eastern Europe, India and Mexico. We believe that for this group macro imbalances have largely dissipated, so growth can move forward on a sustainable path.

Latin America has been particularly hard hit given the region's heavy dependency on commodity exports, so we are encouraged to see that Argentina has begun the implementation of an ambitious reform agenda since the election of a new government in November 2015 under the leadership of President Macri. Initiatives enacted include the removal of capital controls, allowing the currency to float more freely and the ending of agricultural export taxes. Argentina has also reached a provisional agreement over the long-running dispute with some of its creditors (subject to the approval of its Congress), which should pave the way for it to access international bond markets. The reforms have been well received by investors, with the Argentinian equity market performing strongly to date in 2016. However, the road to reform in Brazil is likely to be a much longer one and requires the necessary political will to embark on the difficult and painful process of structural economic reform.

But emerging markets investors are, of course, still looking to China, which faces two key problems. First, the pace of fixed asset investment (FAI), which accounts for half of Chinese GDP, is decelerating. The main components of FAI are real estate investment, infrastructure and corporate capital expenditure, and it's the first of these that we consider to be the most problematic area. We do not believe there will be enough demand over the long term to sustain China's current rate of property build and any slowdown will also hit infrastructure investment. If we combine investment in real estate, related infrastructure and auxiliary industries (e.g. steel or cement manufacturing), something close to a quarter of China's GDP is at risk of a slowdown and possibly negative growth.

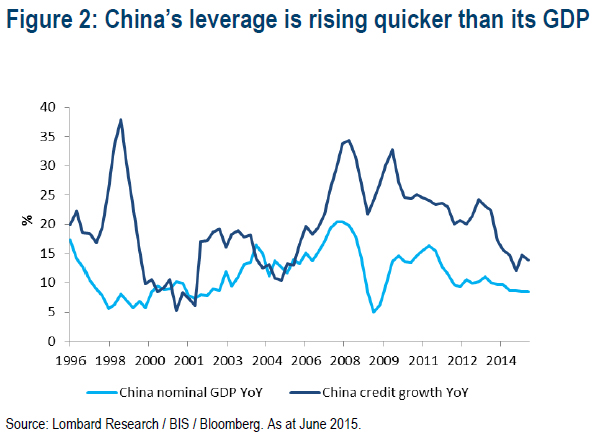

The second problem China faces is a rapid build-up of debt in its economy. Fixed asset investment-led growth resulted in debt accumulation both by the corporate sector, as well as by provincial governments, which were at the forefront of infrastructure investment . Now, as the investment cycle is decelerating, heavily indebted companies find that their cash flow is not sufficient to repay debt and in some cases doesn't even cover interest payments. Whether China tries to tackle its debt problem and has the resolve to go through a painful process of shutting down idle capacity in a number of industries remains a key question. However, first steps towards addressing the overcapacity problems in the steel and coal mining industries have been made with the government creating a RMB 100bn fund to cover lay-offs in those sectors.

China has a long-term goal to increase consumption as a share of GDP, but we have doubts whether consumption can grow at the double digit rate of the past in an environment where construction and associated industries are under pressure and will possibly start shedding jobs. Therefore, we believe that China will have to revert to relying more heavily on export-oriented industries for job creation. To that end, following years of rapidly rising wages in China and an appreciating currency, the competitiveness of Chinese exporters has been somewhat eroded. A weaker RMB could help restore the position of Chinese exporters, though sluggish global demand will pose a constraint. Unfortunately, competitive currency devaluation globally looks like an increasingly likely scenario with China joining the game.

In this context both the commodity exporters to China, as well as the economies which compete with China in export markets (e.g. Korea and Taiwan) will be affected negatively and will suffer from the weaker RMB. While there is still a significant amount of capital that would like to exit China, and Chinese corporates still have outstanding debt in FX, ultimately the weakness of the currency is not a problem in itself. Once the currency adjusts to a more competitive level, the country's significant trade surplus will help stabilise capital outflows. The question in my mind is whether, in the shorter term, capital flight could prick the debt bubble, leading to a disorderly credit unwind.These indicators point to continued caution. We are watching for stability in oil prices, credit spreads, and currency markets (China in particular) before we will regard this volatility storm to have passed.

The second approach to profiting in a sideways market explores opportunities from a cross-sectional perspective. If we can identify a strong relative preference between two investments, then we can pair them off, one against the other, and extract returns from their relative performance. In a market environment that features heavy influence from macro factors, like central bank tightening, and a preponderance of index-based trading, the likelihood of individual securities becoming mispriced rises.