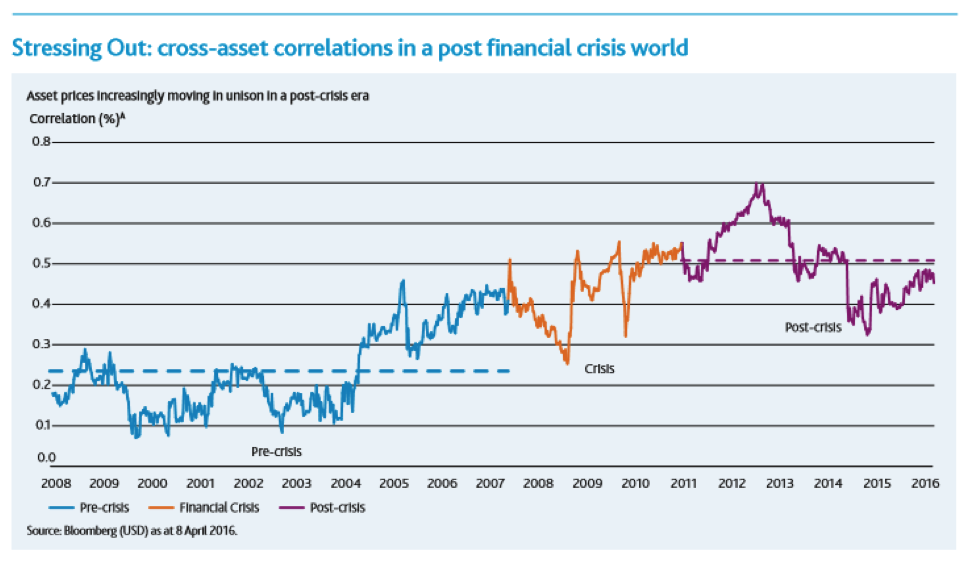

The first quarter of 2016 proved to be a serious challenge for investors. Anxiety about the outlook for the Chinese economy, falling oil prices and more downward pressure on commodities sparked weakness in risk assets and sent equity markets down sharply. In January alone, the US stock market fell 5.3%, Japan fell 7.6% and the Pacific region ex Japan declined 6.6%. Oil and resources dependent markets were hit hardest. Central banks kept policy loose or even expanded their support as was the case with the European Central Bank’s (ECB) extension to quantitative easing in March. Yet the alarm about recession remained heightened through to the end of the quarter. Prices across asset classes increasingly moved in unison leaving few places to shelter.

Since the end of the first quarter, investor sentiment has reversed. The riskiest equity and bond markets, such as oil dependent Russia, have rebounded sharply along with emerging markets equities, high yield debt and commodities. Several indices and sectors recovered most of the ground lost in the previous three months. During the first quarter period, our view was that the fundamental macro-economic trends and business conditions had not deteriorated to the extent that market behaviour suggested. As news flow proved that the world economy was not slipping into recession and that central banks remained accommodative, risk assets recovered. But why the increase in correlation between asset classes? How can it be explained and will it be a persistent feature?

In October 2015 and again in April 2016, the International Monetary Fund (IMF) addressed these questions in their World Financial Stability Reports. They point out that the tendency for global asset prices to move together is at its highest level since the 2008 Financial Crisis (FC). The report identifies low liquidity as a feature of the post FC world caused by shrinkage of the banking sector and the impact of new regulation. Other factors affecting cross-asset correlation include the rise of high frequency trading, benchmarking and the increased use of derivatives and exchange traded funds. The IMF paper argued that the “decline in market liquidity and the increasing use of derivatives are associated with higher asset pricing correlations over the past five years.” For investors, the result of this trend is particularly acute during periods of market stress, such as the one we have just experienced.

The rise in the tendency for asset prices to move in unison (i.e. higher levels of correlation) has yet to be fully understood. However, there is mounting evidence pointing to the involvement of structural shifts, both temporary and long-lasting. Aberdeen’s Global Investment Strategy team conducted their own research on cross-asset correlation and the outcomes are shown in the chart above and table below. The chart illustrates that average asset correlations across both developed and emerging markets have increased from 2010 and remained inflated compared to pre-crisis levels. We believe that a combination of short and long term structural issues is to blame.

Short term Market Changes

Following the global financial crisis, expansionary monetary policies enacted by central banks appear to have led investors to lower levels of risk aversion and the pursuit of higher yields. When investors become less discerning in terms of their holdings this translates into higher correlations amongst assets and implies a greater resemblance to equity returns. Although this situation is transitory, it is likely to carry on for some time in developed countries.

Long term Structural Changes

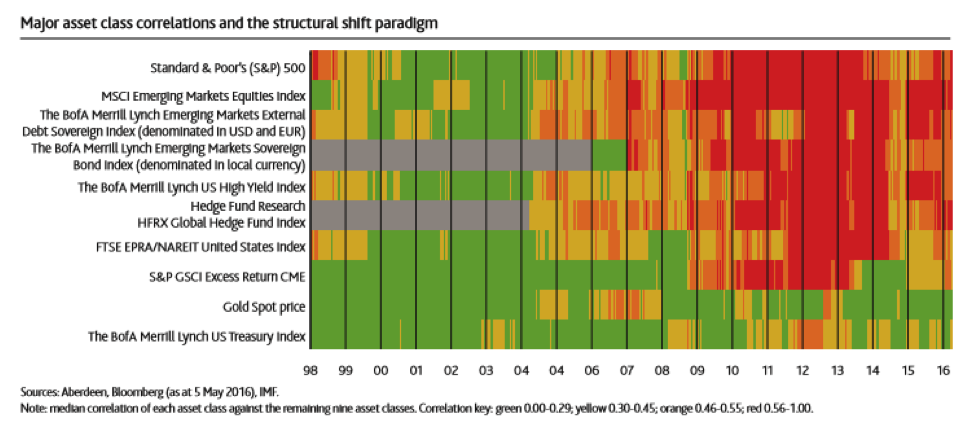

The rise in the tendency for asset prices to move in unison (i.e. higher levels of correlation) has yet to be fully understood. The fragility of market liquidity and more benchmarking appear to be the other explanation associated with the rise in asset price correlations since 2010. Traditional market makers have reduced their level of activity on claims of trading restrictions and tightening regulation. Meanwhile, the rise of algorithmic and high-frequency trading strategies has led to lower pools of liquidity available to stabilise markets during risky conditions. Elsewhere, the drive towards benchmarking by investing in indices or underlying baskets of securities has also reduced the liquidity for assets outside the benchmark index. We think this effect is further magnified by the increase in trading of index-based derivatives and exchange-traded funds. This can be viewed in the below correlation heat map where we compare how each asset relates to the others. It indicates an unprecedented shift since 2010 where a growing number of assets move in parallel.

For investors the conclusion is that cross-asset correlations have changed since the 2008 financial crisis. For both short and long term reasons. Less liquidity in a post financial crisis banking system along with technological change, new regulation and investment innovation are all contributing to the trend and it’s unlikely to reverse soon. The IMF along with regulators and monetary authorities has been looking at a number of policy changes to address illiquidity and stability spill overs with work ongoing. Meanwhile, investors need to hold onto their long term principles of seeking well diversified portfolios and investing in good quality assets. And use times of market stress to identify the undervalued opportunities that these highly correlated markets throw out.

Investment Strategy

Our views in May marked a departure over those seen in April, prompted by our quantitative analysis framework which favoured riskier assets, driven by some reversal in the negative trends observed the previous month. This resulted in an upgrade of equities to overweight from underweight, balanced by a slight reduction in bonds. This move was supported by a greater allocation to European equities (excluding the UK) where abundant liquidity, attractive long-term funding conditions by the European Central Bank and investor sell-offs in recent weeks should all be constructive going forward. We have also noted the pickup in both earnings revisions and price momentum across Pacific equities (excluding Japan), which warranted a reduction in our underweight position. However, we remain mindful of latent problems in the local property market and ongoing terms of trade issues. We reduced our exposure to high yield bonds given less attractive valuations combined with concerns surrounding US leverage conditions and our continued more cautious view of energy markets. This asset’s correlation to the oil price is also shared by global inflation-linked government bonds, which prompted us to trim our overweight stance. Our view on this asset class was also reinforced by the recent rally in real yields and break-even rates (implying persistence of positive drivers to be less likely). Elsewhere, we maintained our positioning this month.

Ken Adams is head of global strategy at Aberdeen Asset Management.

Global Investment Outlook

June 8, 2016

« Previous Article

| Next Article »

Login in order to post a comment