"Stocks beat gold in the long run!" is a 'rallying cry' to buy stocks we have heard lately that gets me riled up. It’s upsetting to me for two reasons: first, an out of context comparison, in my opinion, misguides investors. It might be the wrong assertion in the short to medium term.

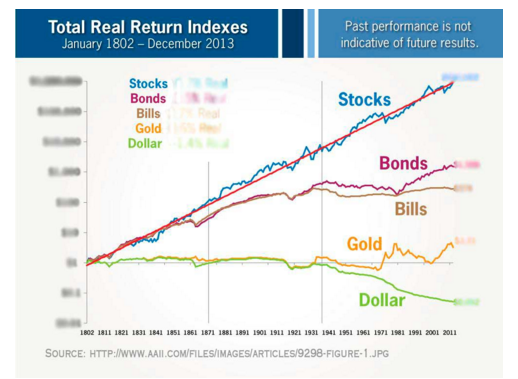

As background, Wharton School Professor Jeremy Siegel is author of the book Stocks for the Long Run, first published in 1994. I have heard Siegel, who is also the public face of a major ETF sponsor, frequently present the bullish case for stocks. Siegel had yet another bull-speech at a recent conference, in a follow-up discussion on gold that was on the outperformance of stocks versus gold. According to Siegel’s work, stocks returned a real rate of return of 6.7% from 1802 to 2013; in comparison, gold had a real rate of return of 0.6%. This provides the appearance that stocks beat gold hands down; assuming this is correct, why would this misguide investors? First, let’s clarify that these numbers are said to be real rates of return, not nominal rates (real rates of return are after inflation). Here is a publicly accessible chart of Siegel's theme; note that I intentionally obfuscated the specific numbers as I have concerns with the methodology used that go beyond the scope of this analysis (they are available at this 2014 interview with Siegel):1)

Gold as a diversifier?

Keep in mind that gold is a brick, albeit a shiny one. It's not meant to outperform stocks in the long run; the reason we use bonds and cash is not because we think they'll outperform stocks in the long run, but because they may be valuable diversifiers.

The chart shows the dollar started to underperform after the Fed was introduced in the early part of last century, then in earnest during the Great Depression. We also read into this chart that the credit driven super cycle that started at the end of the Great Depression was at the expense of the dollar.

The dollar was linked to gold for most of the period that chart shows. The link persisted until 1971; the outperformance of gold versus cash prior to 1971 is attributed to official debasements of the dollar. Let’s have a closer look at the performance of bonds from the end of the Great Depression until Paul Volcker became Chairman of the Fed (that was in August 1979). That negative performance has a good reason: we experienced an environment of financial repression as real interest rates were negative. It’s that sort of environment that we believe is favorable to gold as receiving no interest is better than negative real rates. However, gold couldn’t react at the time, because of the link between the dollar and gold. The 'gold window' closed because the U.S. could no longer sustain the link; not surprisingly, the period after 1971 was rather volatile and distortions (the boom/bust of 1980) were a side effect.

We believe that similar to the Great Depression, we are near the end of a debt super cycle. That means, after decades of credit expansion, it’s time to reduce the relative debt in the economy; the ways to achieve this are through growth, default or inflation; hedge fund manager Ray Dalio has been very outspoken on this of late. If our analysis is correct, then odds are high that the era of financial repression may well persist for some time, as the huge debt overhang is worked through. In that context, gold, these days no longer pegged to the dollar, may perform favorably compared to bonds and the dollar. As such, gold may be a good diversifier to a stock portfolio, in the right circumstances.

It’s in this context that I perceive Jeremy Siegel’s touting of stocks may be doing a disservice to investors. Very few advisers recommend a 100% stock allocation; the reason we diversify our portfolios is because most of us are looking to maximize risk-adjusted returns. Diversification is the one free lunch that Wall Street offers. This doesn’t mean gold, or any one specific asset is the ideal diversifier; but it strongly suggests that touting gold or any asset class as the single best investment may be problematic, unless accompanied by a litany of disclaimers/qualifiers.

Gold to outperform?

If stocks have done so well over 200 years compared to gold, is it possible for gold to outperform stocks over a shorter horizon, say 2 years, 10 years or 20 years? The challenge with historical comparisons is that one can always cherry pick to choose what suits one’s argument. One can choose the price of gold at the peak of 1980 to see how long it has languished; or one can pick the top of the Nasdaq bubble, just as gold bottomed out a few years later to see how gold might do versus stocks for many years. Ultimately, what matters to investors is what the price of gold is going to do going forward. We like to show the price of gold since 1971 (when it de-coupled from the U.S. dollar) in relation to past bear markets in equities. During this period from 1970 through 2015, gold had an annual return of 7.70% with a correlation to equities of zero: