The S&P/Case-Shiller U.S. National Home Price Index posted a 4.5 percent year over year gain in January 2015 following a 4.6 percent jump in December 2014. But on a month-to-month basis, the index declined for a fifth month straight, falling 0.1 percent in January amid a harsh winter.

XHB holds homebuilders, building-materials producers, home-improvement retailers and home-furnishing retailers in a 35-stock portfolio.

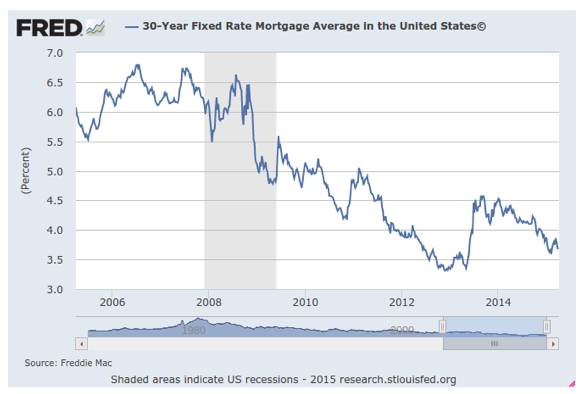

iShares US Home Construction (ITB) overlaps considerably with 37 names. The major difference between the two is that XHB is equal weighted and ITB is market-cap weighted. XHB has greater exposure to home furnishing and home improvement retail stocks than ITB. Home builders have managed to scale to the top of the leader board this year after lagging the stock market in 2014. The stars have aligned with low interest rates, pent-up demand from a harsh winter and robust job growth, fueling consumer confidence and household formation. At the same time, wage growth has been accelerating and the drop in oil prices has translated into extra dollars in the consumer’s pocket. The savings rate is currently at 5.7 percent, the highest since March of 2012. Home price increases have been moderate and lending conditions are generally easier. This all suggests the improvement in homebuilders should continue as we head into the spring selling season, which runs from April through August—the busiest months for housing.

Home builders have managed to scale to the top of the leader board this year after lagging the stock market in 2014. The stars have aligned with low interest rates, pent-up demand from a harsh winter and robust job growth, fueling consumer confidence and household formation. At the same time, wage growth has been accelerating and the drop in oil prices has translated into extra dollars in the consumer’s pocket. The savings rate is currently at 5.7 percent, the highest since March of 2012. Home price increases have been moderate and lending conditions are generally easier. This all suggests the improvement in homebuilders should continue as we head into the spring selling season, which runs from April through August—the busiest months for housing.

iShares U.S. Home Construction ETF (ITB) rallied 11 percent year to date, far surpassing the SPDR S&P 500 ETF’s (SPY) 1 percent uptick, through Apr. 2. It’s a welcome turnaround after it rose only 5 percent last year when the benchmark climbed 14 percent. SPDR S&P Homebuilders ETF(XHB) returned 9 percent year to date after rising only 3 percent in 2014. The major indexes eclipsed their pre-recession highs two years ago but homebuilder ETFs have yet to regain their former peaks, which means they have room to catch up.

In February, U.S. housing starts dropped 17 percent month on month to a seasonally adjusted annual rate of 897,000 homes partly owing to harsh winter weather. Given that home building has been lackluster the past few months, homebuilder stocks are pricing in a rebound in the months to come.

Home Builder Improvements

Publicly traded homebuilders tracked by S&P Capital IQ saw deliveries of new homes in calendar year 2014 rise 9 percent to 119,741, from 109,659 homes. The new home deliveries spiked 24 percent in 2013, the strongest growth rate since the 2007-2009 crash. S&P forecasts more subdued unit growth of 6.3 percent, to 127,300 units for calendar year 2015.

“Most publicly traded builders are in a stable competitive position after cutting costs, retiring debt and growing cash positions,” Erik Oja, a homebuilder analyst at S&P Capital IQ wrote in an equity report March 25. “Attractive property lots for future development are increasingly scarce, and homebuilders who have locked up several years supply of land, will be in a good position to develop communities and deliver homes.”

DR Horton (DHI), the largest homebuilder by market cap, increased the number of new homes delivered almost 19 percent in fiscal year 2014 to 28,670 homes. The average selling price rose 11 percent while revenues climbed 32 percent. Average selling prices climbed 7 percent year over year in Q1 for FY 2015. Delivery of new homes surged 29 percent to 7,973 while revenue vaulted 37 percent.

S&P Capital IQ analysts forecast a 14 percent hike in homes delivered in FY 15, to 32,675 along with a 3 percent price jump, translating to a 17 percent spike in revenues. They project a 7 percent increase in homes delivered in FY 2016 to 35,000 homes with a 3 percent price increase and 10 percent rise in revenue.

“Homebuilder industry revenues should grow by 12 percent to 13 percent in the next two years, supported by both price hikes and higher unit sales volume,” Todd Rosenbluth, director of ETF and mutual fund research at S&P Capital IQ Global Markets Intelligence, wrote in a report Jan. 29. “Meanwhile, home furnishing revenues should benefit from sustained economic growth and potentially new retail store openings, following peer-group consolidation, while home appliance shipments should increase at low to mid-single digit growth rates.”

Multi-family housing starts have rebounded back to 2007 levels, running at 97 percent of prerecession highs. Single-family housing starts are at just a third of the way to their previous high. Housing supplies remain tight and the rate of new orders should improve unless there’s a significant spike in mortgage rates. As of February, there was 4.6 months of supply of homes on the market, the same as January. That falls short of the six months of supply that is considered a healthy balance between supply and demand.

Investment Risks

Home builder shares are very volatile. Home builders have very thin gross margins. Higher-than-expected increases in materials and labor costs, reluctance of lenders to write mortgages and rising interest rates would reduce affordability, especially among first-time home buyers. Home prices are rising much faster than wages.

ETFs And Mutual Funds

The home building industry has very low barriers to entry and is very fragmented. The top five U.S. home builders by revenue accounted for only 18 percent of the market in 2013, according to Morningstar. I recommend investing in homebuilders through SPDR S&P Homebuilders ETF(XHB), iShares US Home Construction (ITB) or Fidelity Select Construction & Housing Portfolio (FSHOX), which returned 9 percent year to date.

UBS rolled out in March more pure plays on homebuilders with ETRACS ISE Exclusively Homebuilders ETN (HOMX) and ETRACS Monthly Reset 2x Leveraged ISE Exclusively Homebuilders ETN (HOML). But they’re very thinly traded because they’re so new.

Michael Passante is a portfolio manager at Focused Wealth Management, a registered investment advisory firm in Highland, N.Y.

Home Builders’ Stock Prices Rebound After Winter Lull

April 8, 2015

« Previous Article

| Next Article »

Login in order to post a comment