The traditional approach to investment portfolios involves diversifying them with low-correlation investments to help maximize their return for a given level of risk (or alternatively, to minimize risk for a given level of return).

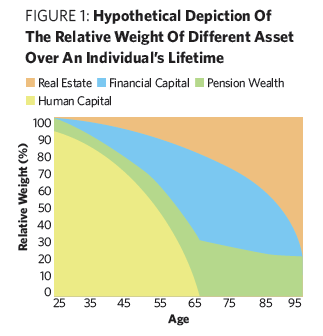

Yet from the holistic financial planning perspective, a household balance sheet is more than just the portfolio of liquid financial assets. Real estate holdings are also important, whether it’s a person’s primary residence or some other direct property holding. Also important for prospective retirees are the implied asset values of future Social Security and the lump sum equivalent of pension payments.

But for people still working, financial capital is typically not even the biggest asset. It’s often trumped by the individual’s “human capital.”

Financial And Human Capital Correlation

Human capital is simply a worker’s ability to work and generate income in the future. And for those who have many working years before them, it can be an enormous asset.

As David Blanchett and Philip Straehl of Morningstar point out in their recent paper, “No Portfolio Is An Island,” financial capital is actually a minority share of the household’s total balance sheet, which is dominated in the early years by the human capital factor (measured as the present value of our future earnings).

In fact, it may be two, five or even 10 times the value of its financial counterpart. Actually, the only moment at which financial capital briefly represents the majority of total household assets is right at the transition into retirement.

Accordingly, it’s crucial to not just view the portfolio by itself but to diversify around the human part of the equation, given the sheer size of the human capital asset. In practice, this implies that workers in conservative “bond-like” jobs might require more equity-heavy portfolios, while those in more aggressive “stock-like” jobs should invest even more conservatively.

Diversifying around job sectors matters, too. Those who work in the tech industry might want to own less of that sector in their portfolios. And that means financial advisors, who are greatly exposed to the economic and stock market cycle by virtue of their jobs, might actually want to own less in stocks (or at least far less in financials!)

It’s also notable that over time, human capital, like its financial form, is not stable—people can get raises or get fired. Their industries may benefit from more or less wage growth. The manufacturing sector, for instance, gives raises in times of growth but cuts salaries or lays off staff during recessions. Some companies go out of business altogether, and their (former) workers become unemployed.

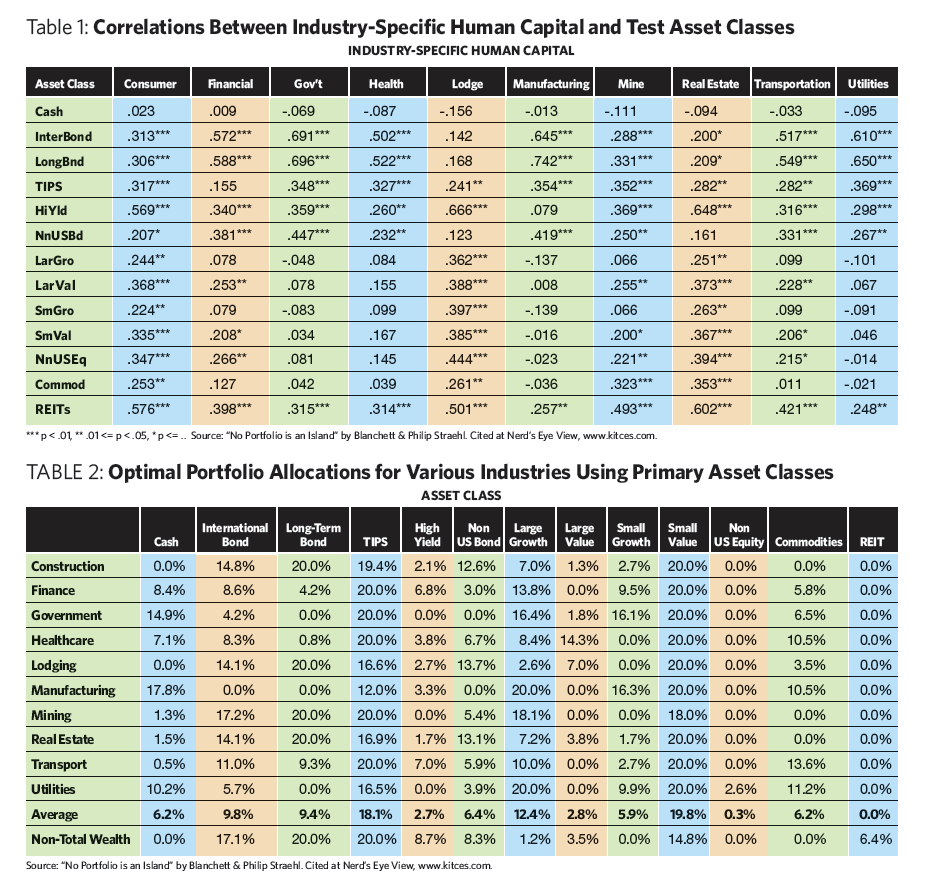

Since these economic dynamics affect the value of financial as well as human capital, Blanchett and Straehl analyzed the correlations between investments in the major asset classes and the human capital value for various industries (based on 12 industries in Kenneth French’s data library).

The correlations between the two can be quite significant, but also quite varied from one industry to the next. For instance, high-yield bonds have a 0.65 correlation to the real estate industry, but no statistically significant relationship to manufacturing. The manufacturing industry, meanwhile, shows the strongest relationship to long-term government bonds, which for their part have no relationship to the lodging industry. The lodging industry actually has the strongest correlation of any industry to all the equity asset classes (large cap, small cap, growth, value and international).

An Asset Allocation Based On Your Job

While mean-variance optimization was built primarily for available investments in a portfolio, there’s no reason it can’t be applied more broadly across both financial and human capital. In fact, given how human capital in different industries has different risk-return characteristics and thus different correlations to asset classes, it’s possible to determine what the optimal allocation should be even when diversifying across the financial and human capital.

Once the risks and volatility of human capital are considered, the “optimal” portfolio looks remarkably different. REITs, for instance, are already sensitive to both interest rates and the economic cycle, so they do not appear to add any unique diversification to a worker’s existing human capital. Also, because most businesses today are global in nature, diversification into non-U.S. equities shows almost no value in the human-capital-diversified portfolio.

On the other hand, small-cap value is an especially appealing diversifier. Why? There are more people working for large companies than small (as captured by Blanchett and Straehl’s use of cap-weighted industry indexes), which implies that most human capital already favors large cap … so small-cap value is a good diversifier. Of course, a worker already employed by a smaller capitalization company might not find owning more small-cap stocks to be as valuable, so his or her portfolio would tilt back toward more large caps instead.

In some cases, the optimal exposure and relevance of a particular asset class is very sensitive to the particular industry. For instance, high-yield bonds are most relevant as a diversifier for those working in financial services or the transportation industries, but not for government workers or those in mining or utilities. Long-term government bonds (and also international bonds) are especially good diversifiers for the construction, lodging, mining and real estate industries, but quite poor for government, health-care, manufacturing and utilities workers.

Overall, the study finds that the average allocations of a human-capital-adjusted portfolio change by 37.6%. The change is more than 50% for the most “extreme” industries: government, manufacturing and utilities (i.e., those with the most materially different risk/return and correlation characteristics).

Allocating Exposure Around Jobs

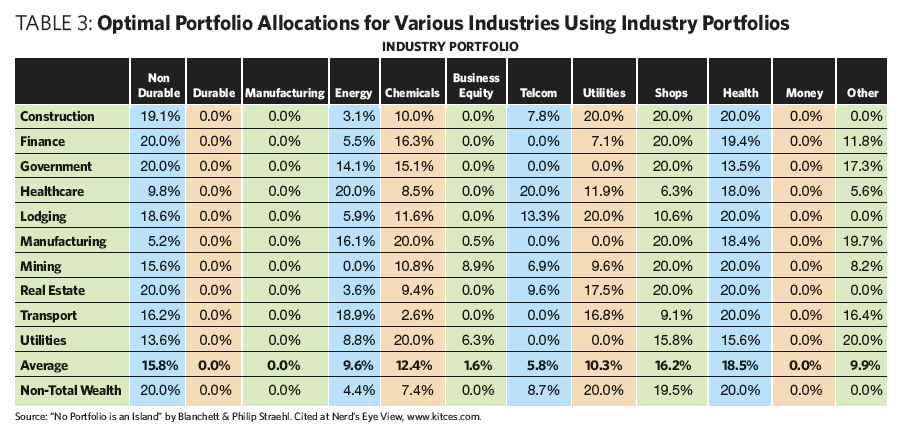

Taking these factors into account, portfolios can also be designed not only around asset classes but around specific sectors and how they relate to a worker’s existing job exposure. For instance, it probably isn’t very helpful for someone working in utilities to own utilities stocks. But those companies could be a very good diversifier for someone working in the construction industry.

The best portfolios can vary significantly, with manufacturing, utilities, government and health care showing the most significant differences from job-agnostic portfolio designs.

Notably, the results suggest that certain industries have no useful portfolio diversification value at all. The optimal allocation to the financial services industry, to durable goods and to manufacturing is 0% across the board for workers in all industries. It’s zero for business equipment as well. (But these were also zero when the workers’ industries were ignored, suggesting these sectors aren’t helpful in the first place from a portfolio optimization perspective.)

Will Future Portfolios Be Job-Specific?

While some might quibble with the particular selection of industries and data used in the Morningstar paper, the fundamental point remains that for workers still in the accumulation phase with years until retirement, human capital really does have significant value, significant risk and a significant relationship to the risk/return characteristics of other assets in a portfolio. This represents an opportunity to diversify against those risks.

So how might this approach look in practice? A starting point would be to reduce a client’s U.S. exposure to the industry he or she already works in (less in utilities for a utilities worker, less in REITs for someone who works in real estate, etc.). It also means adjusting cap-weight exposures (adding more to small-cap positions for someone who works at a large-cap company and

vice versa).

Diversifying As A Financial Advisor

Notably, this job-based approach is as relevant for financial advisors as our clients. Our jobs are especially exposed to, and correlated with, the economy and the stock market. When a recession occurs and a bear market emerges, it’s a hit to everything from our job prospects to our profits. And of course, if you are an advisory firm owner, the situation is even more extreme, as the value of your firm—based on a multiple of profits or free cash flow—is not only correlated to the markets but even more volatile.

This implies that advisors should be especially conservative with their own portfolios and even, ironically, dial down their equity exposure (especially to the financial services sector). Similarly, they should maintain larger cash allocations or emergency reserves, and more aggressively pay down any personal debt.

Risk Tolerance And Behavioral Finance

One important challenge to this approach is that portfolios with such human-capital-adjusted allocations, when viewed in isolation, may feel “extreme” or “distorted” to the investor.

For instance, a government employee has an extremely conservative “bond-like” human capital. If that employee is also young, then human capital might make up well over 90% of his or her net worth. Accordingly, such a person could invest 100% of a liquid portfolio in equities, and the investor’s total household net worth would still be in a “10/90 portfolio”—10% is in equities while 90% is in a human capital “bond.”

But while such an allocation might seem reasonable in terms of human capital, the investment portfolio is still 100% in equities, which might feel jarring to a client with a conservative risk tolerance (who cannot recognize the role “invisible” human capital is playing).

A similar problem occurs when retirees try to allocate a portfolio around the bond-like asset value of their Social Security. The allocations appear concentrated and risky when you look at the portfolio by itself.

At the opposite extreme, an aggressive entrepreneur whose human capital is extremely stock-like would ideally allocate his or her entire portfolio to bonds and cash, just to tone down and diversify a household balance sheet of what otherwise may be nearly 100% equities. From the financial planning perspective and the investor’s risk capacity, this may seem entirely reasonable—a stock-like job plus the volatile value of a business really is risky, and should be dampened down with a significant bond/cash holding and a large emergency reserve.

However, in real life an aggressive entrepreneur with a high tolerance for risk in his or her job and business probably also has a high tolerance for portfolio risk. If the entrepreneur is so risk tolerant that 100% equity exposure is OK, then both the job and portfolio would be fully invested in stocks. The latter would not be used to diversify against the former.

Even so, it’s arguably still relevant to diversify by sector and industry—to own less in financials if the entrepreneur runs a financial advisory firm (which is already the equivalent of a concentrated investment in the financial sector). This won’t run contrary to the investor’s overall risk tolerance. It’s just prudent diversification within equities.

Tools To Create Industry-Based Portfolios

Ultimately, the Blanchett and Straehl paper may create a basis for a new standard in how we invest portfolios for accumulators. But unfortunately, at this point we lack tools to actually execute the strategy. The concept of pitting jobs against stock holdings is perhaps a good starting point, but alas it’s difficult to apply consistently across a broad base of clients in a wide range of situations.

In the future, though, it wouldn’t be surprising to see a new set of investment tools evolve—perhaps software designed to take information about an investor’s human capital and come up with a more precise series of portfolio allocations that allow for better household diversification. Such an approach could be a significant value-add for “personalized” portfolio design. And notably, because the interrelationship between assets can change, and because over time a worker’s human capital declines while financial capital increases (as savings), the worker’s portfolio will need monitoring and ongoing management to be reallocated.

Such a strategy might actually benefit from the proliferation of sector-specific ETFs, which allow advisors to recreate the total equity exposure of U.S. stocks with more or less of those industries that duplicate the investor’s human capital. (TAMPs or robo-advisors might even help with implementation. Or what if asset managers came up with “target-date” style funds based not on retirement dates but industries?)

In other words, in the future it may even be far less common to own a single “core” investment position like the S&P 500 when more personalized portfolios that are better diversified around human capital can be created instead.

Michael Kitces is a Partner and the Director of Wealth Management for Pinnacle Advisory Group, co-founder of the XY Planning Network, and publisher of the continuing education blog for financial planners, Nerd’s Eye View. You can follow him on Twitter at @MichaelKitces.