Key Points

• Markets have recovered quickly from the Brexit shock, and pro-EU sentiment seems to have strengthened.

• Global economic growth appears to be stable, and there are signs governments may be warming to fiscal stimulus to keep things moving.

• International stocks provide diversification benefits that can help reduce downside risks during times of market turmoil.

What a difference a few weeks can make. After the U.K. voted in late June to leave the European Union in the so-called Brexit vote, global stock markets plunged and concerns about anti-EU sentiment spreading to other countries were rampant. Now many stock indexes are at or near historic highs.

So what happened? Was this a case of much ado about nothing?

Here's what we know: Sentiment hasn't turned decisively against the EU elsewhere in Europe, and global economic growth hasn't suffered as much as previously feared. And one unexpected effect of the Brexit vote may be that policymakers are now more willing to ramp up government spending to help fend off political threats, which could actually reinforce growth. Let's take a closer look.

Enduring appeal

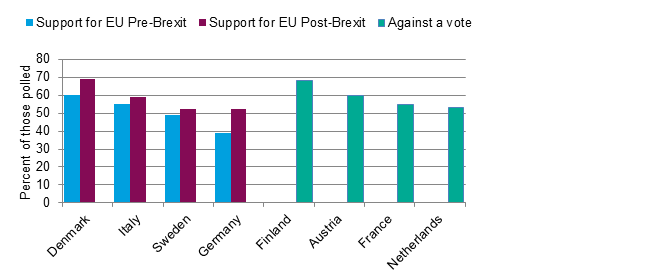

The British may have wanted to make a statement about the EU when they voted to leave, but it doesn't appear to have resonated. If anything, support for the EU actually appears to have strengthened in some countries, as you can see in the chart below.

Post Brexit vote, support for the EU and against a vote on EU membership has grown

Source: Charles Schwab & Co. Denmark is represented by the Voxmeter for 6/16/2016 and 7/4/ 2016; Italy is represented by the IFOP 11/2014 and 7/2016; Sweden is represented by Statistics Sweden 6/2/2016 and TNS Sifo 7/26/2016; Germany is represented by the Infratest dimap ARD in 5/2016 and 7/2016. Data measuring sentiment toward an EU vote come from the following: Finland is represented by Iltalehti newspaper polls in 3/2016 and 7/2016; Austria is represented by Gallup in 7/2016; France is represented by the CSA in 7/2016; and the Netherlands is represented by polling by Maurice de Hond in 7/2016. Chart compiled on 8/11/2016.

That doesn't mean there aren't still some calls to follow the U.K.'s lead. Opposition parties in the Netherlands and France have called for referendums on their respective countries' EU membership. Elections in the Netherlands in March 2017 and in France in April-May 2017 will demonstrate how much support such parties have, though polling indicates voters in these countries oppose even holding a vote on the countries' EU membership.

Meanwhile, a constitutional referendum in Italy could test markets in late October or early November. While not explicitly related to the EU, the vote could still provide a sense of how strong local anti-European forces are. At issue here is a plan to reduce government gridlock by shrinking the senate and curtailing some of its powers. The man behind the plan, Prime Minister Matteo Renzi, has promised to step down if voters reject the proposal. Such a failure and the resulting political turmoil could end up benefiting local populist parties, such as the Five Star Movement, which welcomed the Brexit vote but is generally more anti-euro than anti-EU.

However the vote goes, any volatility could be tempered by the European Central Bank's ability to purchase assets. It's also worth mentioning that Italy would face many more structural obstacles to cutting itself off from Europe than Britain did, so an "Italexit" seems unlikely.

Global growth appears stable

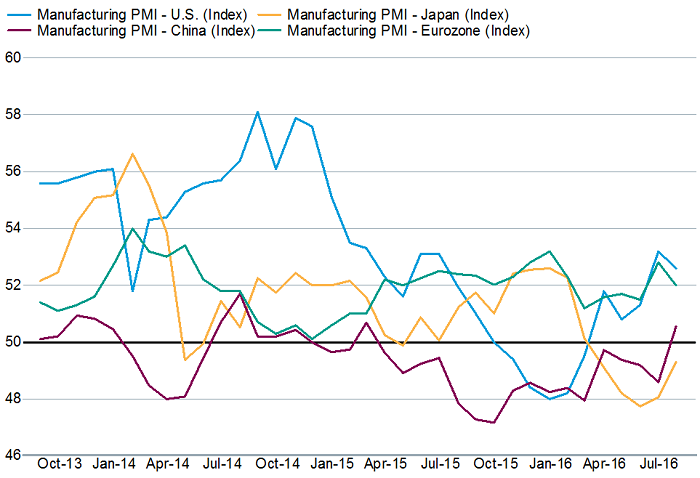

Economic indicators in the wake of the Brexit vote suggest that global growth has been stable despite the unexpected outcome. Growth appears to have improved in Asia in July, and continued to grow, if at a slower pace, in the eurozone and the U.S. Encouragingly, global manufacturing, as measured by purchasing manager index (PMI) surveys—which track information from businesses about new orders, inventory levels, production, supplier deliveries and employment—appear to have bottomed in recent months, as you can see in the chart below. Manufacturing tends to lead overall economic growth, and the PMI data, combined with gains in new manufacturing orders, could mean conditions are set to improve in the coming months.

Manufacturing looks healthy

Source: FactSet, Markit, Institute for Supply Management, as of 8/10/2016. The PMIs are represented by Markit's purchasing manager index surveys, with the exception of the U.S., which uses the Institute for Supply Management (ISM). A reading above 50 means manufacturing activity is expanding.

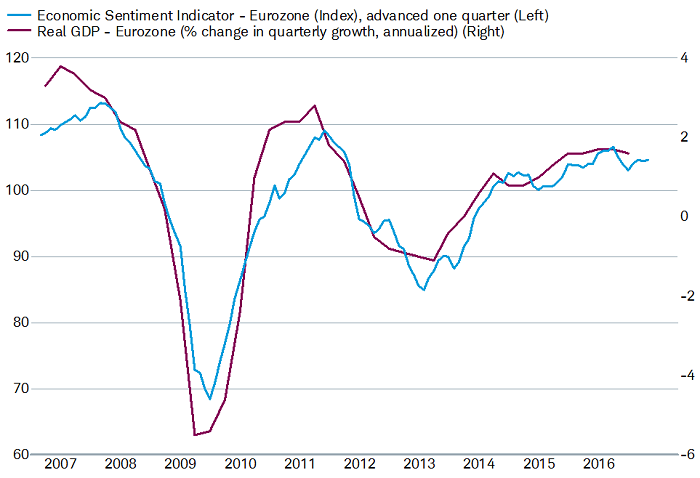

The European Commission's Economic Sentiment Indicator for the euro zone, which covers both business and consumer confidence and also tends to lead economic growth, improved in July, as shown in the chart below. Areas of strength included business sentiment in Germany, France and Italy. While consumer confidence in the eurozone dipped modestly, major purchase intentions rose to a nine-year high.

Brexit doesn't appear to be tripping up the Eurozone

Source: FactSet, European Commission, Eurostat, as of 8/10/2016.

The uncertainty caused by the Brexit vote could still reduce growth outside of the U.K. in the coming months, as the U.K.'s economy will gradually have to prepare for its withdrawal from the EU. And anti-EU sentiment could still increase again and highlight the region's vulnerability. However the current outlook for Europe appears stable, in our opinion.

Fiscal responses

The movement toward more fiscal stimulus had been stirring before the Brexit vote, but could kick into higher gear in the coming months. Persistently slow economic growth has governments rethinking the merits of austerity, and questions about relying on monetary stimulus alone and the pull of populism are adding to the pressure.

The allure of government spending got a boost after a pledge to spend more on infrastructure appeared to help secure a win for Canada's new prime minister. The U.K. came next, abandoning its balanced budget target after the Brexit vote. Japan could be next, potentially moving toward coordinating its fiscal and monetary policies as part of a two-pronged effort to boost growth. In the U.S., both presidential candidates have said they support an increase government spending, particularly on infrastructure, and China said it increased its fiscal deficit as a percentage of gross domestic product this year to a multi-year high, which should help support growth.

All this increased spending could provide another leg of support for economic growth, at least in the short-to-intermediate term. Spending more on infrastructure has been a common theme globally, but the long-term benefits should also be weighed against the potential costs. Reducing logistical bottlenecks and opening new markets can boost growth, but higher taxes and the potential for corruption can undermine the benefits.

Key takeaway

The way stocks bounced after the Brexit vote was a reminder that investors should think twice before making drastic moves in response to the news. A long-term perspective is a prerequisite for investing in stocks.

It's also worth noting that the apparent short-term turbulence overseas shouldn't undermine the case for including an allocation to international stocks in a diversified portfolio. The worst 10-year period for the global stock markets over the past 50 years was from February 1999 to February 2009. During that period, U.S. stocks on their own fared far worse than foreign stocks. The MSCI USA Index fell about 40%, while international stocks as represented by the MSCI EAFE Index fell only about 10%. Having an allocation to both would have helped cushion some of the losses.

Michelle Gibley is director of international research at the Schwab Center for Financial Research.