The recession drumbeat has picked up tempo, which is to be expected given the signal coming from several market-based indicators, the contraction in manufacturing, and the anemic reading on (the lagging) fourth quarter U.S. gross domestic product (GDP). Notwithstanding the sharp equity market rally late last week, the market has certainly been ringing the alarm bell, with the worst January start to a year since 2009. But remember, there is an apt and famous phrase on Wall Street: “The stock market has called nine of the past five recessions.”

Apocalyptic forecasts abound

I was the final keynote speaker at the Inside ETFs Conference in Hollywood, FL last week; and although I wasn’t present for their sessions, there were several notable bears who took the stage before me, generally pointing to the risk we were in the midst of another 2008 (or worse).

I want to do several things in this report. One is to caution investors not to dwell on the past; and why the most ferocious bears often get the most attention. Another is to highlight why leading indicators are more important than lagging indicators when trying to assess the economic (and market) landscape. Finally, I want to remind investors that better or worse typically matters more to markets than good or bad.

Growling bears

We do not think we are in the midst of a repeat of 2008, but the apocalyptic forecasts are garnering a lot of attention. I understand and sympathize with the concerns, but my glass is at least half full. I often wonder why extreme pessimism often sounds more intellectual than optimism. I recently saw a great quote from Matt Ridley’s book The Rational Optimist:

“If you say the world has been getting better you may get away with being called naïve and insensitive. If you say the world is going to go on getting better, you are considered embarrassingly mad. If, on the other hand, you say catastrophe is imminent, you may expect a McArthur genius award or even the Nobel Peace Prize.”

Speaking of the Nobel Prize, Daniel Kahneman won it for showing that people respond more forcefully to loss than gain:

“Organisms that treat threats as more urgent than opportunities have a better chance to survive and reproduce.”

I was intrigued by a note put out by Cornerstone Macro this morning which noted that, “the extreme outcomes pitched last year by various folks have now evolved into a base case scenario for today’s investors.”

Recency bias

Investors are likely attuned to the apocalyptic case partly due to “recency bias” which is the tendency to think that trends and patterns observed in the recent past will repeat in the near future. The financial crisis and attendant brutal bear market is still fresh in investors’ minds and they are determined not to get sucked into the next market vortex.

I try to be objective in my analysis and don’t anticipate Armageddon—or a full-blown recession in the near term—largely because of what the leading indicators are saying.

How we drive is a great analogy when discussing leading and lagging indicators. Who is more likely to reach their destination swiftly and safely?

The driver who looks at the road ahead—both immediately ahead, but also far ahead—while taking periodic glances in the rear-view mirror for perspective.

Bingo. In other words, focus on the leading indicators; but observe the lagging indicators for perspective. By the way, the now-consensus thinking that the Fed may have erred in raising rates in December is interesting to consider in this context given that the Fed’s focus on employment means they have a tendency to key off one of the more lagging of economic indicators—the unemployment rate.

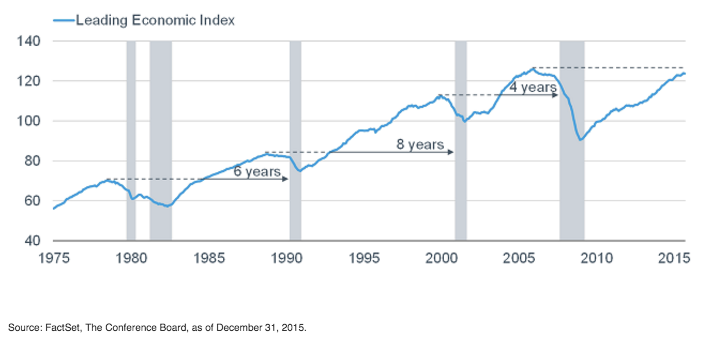

No meaningful rollover in the LEI

The chart below illustrates that the Conference Board’s Index of Leading Indicators (LEI)—the most popular and well-tracked of several leading indexes—have not yet experienced the rollover nearly always seen well in advance of a recession (gray bars).

In fact, the LEI hasn’t even “roundtripped” and taken out its prior (2006) high. Prior roundtrips are denoted by the dotted lines on the chart above. The subsequent solid lines (and years markers) represent the length of time between the roundtrip and the next recession. So, a glance at the history of this data suggests the next major bump in the road for the economy is more likely still ahead of us than upon us.

Better or worse

The key to the health of both the stock market and the economy will be the direction of the leading indicators from here.

Remember, rate of change often matters more than level. In other words, the market tends to move based more on better or worse than good or bad. Market turning points don’t necessarily need a major change in fundamentals—they sometimes just need to see the inflection point.

As I often discuss with our Windhaven Investment Management investors, the markets are complex “non-linear systems” in which the slightest change in the fundamentals (perceived or actual) can trigger disproportionate movements in price. As BCA Research recently noted:

“Such disproportionate price effects leave many strategists and analysts scratching their heads in bewilderment, wondering: what was the catalyst? The answer is there was no fundamental catalyst. The market turned because, like all complex non-linear systems, it reached a periodic point of internal instability, leading to a natural tipping point.”

The opposite works as well, of course—where markets swiftly reverse to the upside, as we saw late-last week.

BCA went on:

“But what causes internal instability in a financial market or individual investment? The answer is excessive groupthink. A financial market is most stable when it includes a wide spectrum of investment horizons—because the different interpretation of the same information allows the long-term and short-term investors to buy and sell to each other in large volume without violently moving the price. The trouble arises when invests engage in groupthink.”

Groupthink has gelled around the worst-case scenario. Our view is less apocalyptic, but cautious nonetheless. We are maintaining our “neutral” rating on U.S. stocks, which means investors should not take any risk above their normal equity allocation. But we would caution against positioning at the extreme for the Armageddon scenario many prognosticators are painting.

Liz Ann Sonders is chief investment strategist at Charles Schwab & Co.