Looking More Broadly

When building or rebalancing the “value” slice of portfolios, advisors may start where most valuation-conscious investors begin: the price/earnings (P/E) ratio. P/E ratios are a straightforward way to identify stocks whose share prices are moderate relative to the level of profitability the company is able to record. Advisors typically also consider the average P/E of a mutual fund’s holdings with that of a benchmark index.

When building or rebalancing the “value” slice of portfolios, advisors may start where most valuation-conscious investors begin: the price/earnings (P/E) ratio. P/E ratios are a straightforward way to identify stocks whose share prices are moderate relative to the level of profitability the company is able to record. Advisors typically also consider the average P/E of a mutual fund’s holdings with that of a benchmark index.

However, P/E is a blunt metric that’s best considered only a starting point when evaluating value. A useful tool that goes deeper is a less-understood valuation measure, the Enterprise Multiple, which is often expressed as Enterprise Value (EV)/EBITDA.

The Enterprise Multiple shouldn’t be employed without context about a company’s management, business model, financial soundness and potential catalysts. Nonetheless, it’s a useful tool that helps go beyond the sometimes misleading simplicity of the commonly used P/E.

Understanding The EV/EBITDA Calculation

The Enterprise Multiple is the ratio of the following two terms:

• Enterprise Value = Market Capitalization + Debt and other liabilities – Cash and Cash Equivalents

• EBITDA = Earnings Before Interest, Tax, Depreciation and Amortization

By incorporating both the debt a company has incurred and the cash it has on hand, Enterprise Value reflects a company’s assets as well as its liabilities, and suggests the approximate price it would take to acquire the company as a whole. The price used in establishing P/E, in contrast, simply indicates the company’s share price.

Similarly, while the earnings figure used in P/E is calculated after all expenses, cash and non-cash, are deducted, EBITDA reflects the actual cash flow a company generates from operations. Thus, it provides a somewhat different perspective.

To get a picture of just how EV/EBITDA helps to clarify whether a company genuinely represents an attractive value, let’s consider the example of two companies in the same industry, facing essentially the same challenges and looking toward similar opportunities.

Omnicare Inc. (OCR) and Pharmerica Corporation (PMC) both operate institutional pharmacies that primarily serve residents in skilled nursing facilities. Omnicare is the larger of the two, but together the pair controls the majority of their market. Both companies have capable management teams, are positioned to benefit from the demographic trend of an aging population and could gain further market share as their industry continues to consolidate. In short, these are two very similar companies in terms of their operations.

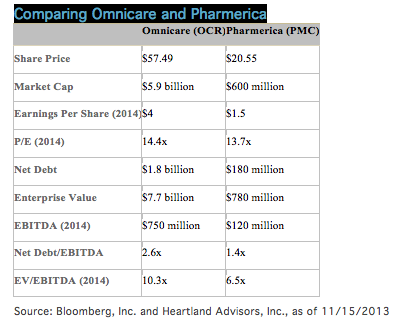

So how do their valuations stack up? For starters, Omnicare’s share price (as of 11/15/2013) was $57.49, while Pharmerica’s was $20.55. This puts Omnicare’s market capitalization near $5.9 billion and Pharmerica’s just above $600 million. Estimates for Omnicare’s 2014 earnings per share stand near $4, meaning its current stock price reflects a forward P/E of 14.4x. Pharmerica is expected to produce earnings of about $1.50 per share in 2014, giving it a forward P/E of 13.7x.

In looking at these stocks purely on a P/E basis, the two appear to be about evenly—and reasonably—valued.

Digging A Little Deeper

What this perspective doesn’t take into account, however, is the different levels of debt carried by the two companies. Omnicare has about $1.8 billion in net debt which, when added to its market cap, gives it an Enterprise Value of about $7.7 billion. Pharmerica’s net debt is approximately $180 million, leading to an Enterprise Value of about $780 million.

With respect to EBITDA, Omnicare is expected to generate about $750 million in 2014, while estimates for Pharmerica run at about $120 million. Thus the EV/EBITDA ratios for the two companies vary widely:

• Omnicare: $7.7 billion EV/$750 million EBITDA = 10.3x Enterprise Multiple

• Pharmerica: $780 million EV/$120 million EBITDA = 6.5x Enterprise Multiple

By this measure, Pharmerica is revealed to be significantly cheaper than Omnicare. There’s still more to the story: Omnicare’s net debt is 2.4 times its EBITDA, while Pharmerica’s is just 1.5 times. In theory, this means that Pharmerica could pay off its debt in about a year and a half, while Omnicare would need about two and a half years to do so, assuming no decline in EBITDA. In our view, this higher level of debt raises the risk associated with the stock.

The question that logically follows is this: Why pay a higher multiple for a riskier asset? This examination revealed Omnicare to have become quite pricey compared to the relatively bargain-priced Pharmerica.

This way of examining a stock’s valuation is consistent with the way private-equity buyers or other companies seeking an acquisition would look at it. (Indeed, Omnicare put in a bid to acquire Pharmerica in 2011, only to have the deal blocked over antitrust concerns.) Compared with multiples we’ve seen for acquisitions in this space, Pharmerica appears more attractive—and thus more likely than Omnicare to attract potential buyers at its current Enterprise Multiple. A stock’s ability to draw this kind of attention can serve as a catalyst to help the market as a whole recognize its full intrinsic value.

Bradford A. Evans, CFA, is senior vice president, director of equity research and portfolio manager for the Heartland Value Plus Fund and Value Fund. He also has portfolio management responsibility for two separately managed account strategies: Small Cap Value and Small Cap Value Plus.

Looking Beyond P/E Ratios For Value

January 8, 2014

« Previous Article

| Next Article »

Login in order to post a comment