The Fed took out an insurance policy in order to stay on a rate hiking path. A shallower path of rate hikes should temporarily ease pressure on the U.S. dollar and help improve financial conditions.

Bond investors should take cues from the TIPS and credit markets. The Fed wants to see tighter credit spreads and higher inflation expectations before raising rates much more.

We view investment-grade corporate bonds and commercial mortgage-backed securities as attractive sources of income in this environment.

The Federal Reserve took a distinctly dovish turn at last week’s FOMC meeting, reducing its expected rate increases for 2016 from 1% to 0.5%. This reduction came alongside a more cautious outlook for both growth and inflation in the U.S. It looks like the Fed took out an insurance policy in order to stay on a hiking path. This reminds us a lot of the FOMC meeting last September at which the Fed delayed its expected rate hike in response to recent market volatility. A shallower path of rate increases should temporarily ease pressure on the U.S. dollar and help improve financial conditions. In a global context, however, positive-yielding government assets are quickly evaporating (Exhibit 1).

Officially, the Fed serves a dual mandate of maximum employment and price stability. On the surface, an unemployment rate of 4.9% and core CPI inflation rate of 2.3% (which, ironically, was published merely hours before the FOMC statement) would indicate that the Fed ought to have a more normal policy rate. Since embarking on rate hikes, however, the Fed seems to have adopted an explicit third mandate of fostering stable financial conditions. This mandate is a bit harder to pin down, but essentially reflects the impact of volatile markets on the ability and willingness of companies and consumers to borrow and spend. Fed Chair Janet Yellen and New York Fed President William Dudley have frequently referred to many observable elements of financial conditions, including stock prices and currency values. However, we think there are two bond market metrics that provide the clearest view.

Bond investors should take cues from the TIPS and corporate bond markets. The prices of TIPS, or Treasury Inflation-Protected Securities, allow us to measure the market’s expected future inflation rate, known as the breakeven rate of inflation. In mid-February, inflation expectations implied by the TIPS market collapsed to levels not seen since early 2009. Previous declines of this magnitude have historically induced the Fed to use an easy policy. Similarly, credit spreads in the corporate bond market also provide a helpful guide to financial conditions. Credit spreads measure the additional yield of corporate bonds compared to Treasuries, and represent the market’s assessment of credit risk. Spreads on investment-grade corporate bonds exceeded 2% earlier this quarter, a level typically only seen during recessions. Each of these metrics exhibited volatility so extreme that, despite more recent improvement, the Fed decided to revisit its game plan. In our view, the Fed wants to see tighter credit spreads and higher inflation expectations before raising rates much more.

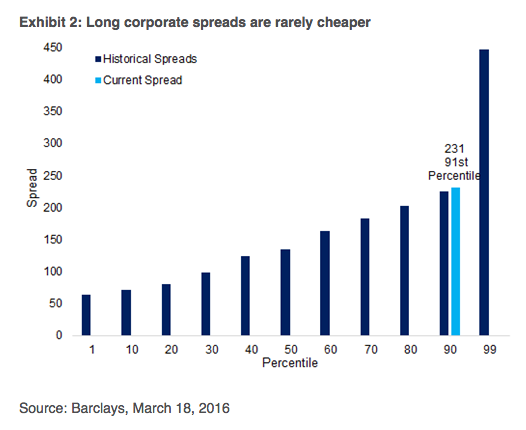

In our view, the combination of low risk-free rates globally, a domestic central bank targeting tamer financial conditions, and a strong household balance sheet all support an increasing portfolio allocation to domestic credit. Investment-grade corporate bonds offer attractive spreads, particularly on longer maturity bonds (Exhibit 2). We believe both corporate fundamentals, as well as Fed policy, will be supportive of IG credit markets. We also think commercial mortgage-backed securities, or CMBS, look more attractive than they have in several years. Commercial mortgages benefit from an improving domestic real estate sector, with very limited impact from swings in international factors, currency volatility, or commodity prices. Also, yields on investment-grade commercial mortgages have increased to attractive levels.

Gene Tannuzzo CFA, is senior portfolio manager at Columbia Threadneedle Investments.

At the March FOMC meeting, the Fed decided to err on the side of caution. The committee members scaled back their expectations on the number of interest rate increases to twice this year, down from four times projected in their December meeting when they raised rates for the first time since 2006. This should bode well for the bond market near term, and we believe investors in need of income have an attractive entry point to invest in many areas of the bond market at higher yields.