Given the ongoing advances in medical research, a client considering a retirement plan should prepare for the possibility of a retirement that could last 30 or 40 years. Over this lengthy span of time, the steady erosion of purchasing power due to the effects of inflation should be of more concern to retirees than shorter-term market volatility.

Purchasing power is the value of a dollar in correlation to the amount of goods or services that it can buy at a given time. This is very important to retirees because, all else being equal, inflation can steadily erode the amount of goods and services that a dollar can purchase over time.

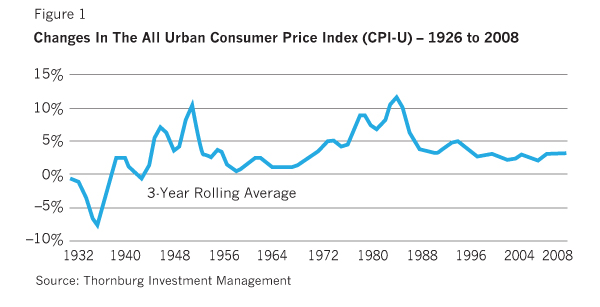

Inflation is typically measured by changes in the consumer price index (CPI) maintained by the U.S. Bureau of Labor Statistics (BLS). Although there are several indices maintained, the one most commonly referred to is the CPI-U, which measures the inflation for all urban consumers. For the 83-year period of 1926-2008, average annual inflation has been 3.15%. However, as illustrated in Figure 1, inflation for shorter periods can be quite different.

Recently, the BLS has begun compiling an experimental index for elderly consumers (65 years of age and older), referred to as the CPI-E. This index is designed to better reflect the spending habits of elderly consumers. For the 25 years covered by the CPI-E, the average annual increase has been 3.33% versus 3.11% for the CPI-U Index, which seems to indicate that elderly consum-

ers are affected more by inflation than the average consumer.

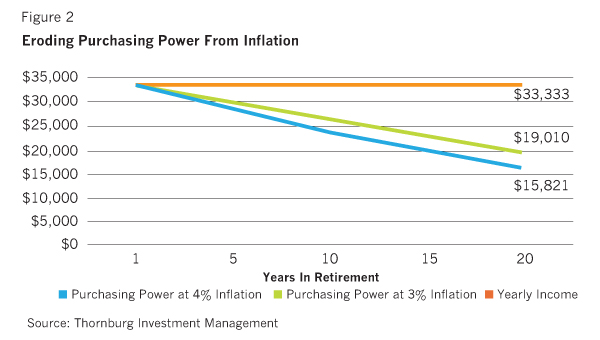

Baby-boomer retirees may be particularly susceptible to the eroding effects of inflation, given that they will be less likely than past generations to have some form of pension that could be indexed for inflation. This generation is relying more on savings accumulated in 401(k), 403(b), IRA, and after-tax savings accounts to support them in retirement. Unless these savings are prudently invested during retirement to allow the income stream to grow at a pace comparable with the increase in inflation, purchasing power will be diminished. To illustrate this concept, let's use a simple hypothetical case of a retiree who has $1 million in retirement savings and has decided to spend the amount evenly over a 30-year period ($33,333 per year). The retiree also decides not to invest the money to ensure safekeeping. Over the next 20 years, at an average annual inflation rate of 3%, purchasing power drops by 42% to the equivalent of $19,010 per year, and if inflation runs at 4% annually, purchasing power declines by 52% to $15,821. Imagine retiring at age 62 and by age 82 only being able to spend the equivalent of $15,821 per year in today's dollars!

For retirees, risk should be viewed as the probability of not providing for a sustainable 30-year retirement. In the example in Figure 2, the retiree believes that they are being risk averse by not being invested, and is completely exposed to the steady eroding effects of inflation. Therefore, under this scenario the only option for keeping pace with inflation is to spend a little more of the savings each year to cover the increase in the cost of living, which will result in the retirement savings being depleted earlier than planned.

The typical Baby Boomer who is looking to retire in the coming years will more than likely want to use a higher initial spending rate than 3.33% ($33,333 divided by $1 million in retirement savings), used our example. Often, retirees will choose a withdrawal rate of 4% to 5% with an annual cost of living adjustment to account for inflation. One key factor that retirees should consider is how much investment return will be needed to support their desired withdrawal level. Knowing what minimum return will be required to achieve a retirement plan is a key piece of information that every retiree should know. We will refer to this minimum return required as the "real return hurdle", which is the minimum return, after accounting for fees, expenses, and taxes, needed to provide the time frame, spending level, and legacy amount chosen for the retirement plan.

To calculate the real return hurdle, there are three basic variables that a retiree needs to factor: the length of time to be spent in retirement; the initial spending rate desired; and a legacy, if any, that the retiree wishes to leave. Each of these variables is described below.

Time Frame: The longer a retiree plans for their retirement to last, the more investment earnings are needed to sup-

port it. For retirement planning purposes, most advisors will use a minimum of 30 years, but in some instances 40 years

may be even more realistic.

Spending Rate: This is the first year's after-tax spending amount (say $40,000) divided by the total retirement savings (say $1 million) for a 4% initial spending rate.

Legacy: How much of the initial retirement savings account is desired to be left as a gift to family members or charity

upon the end of the retirement period?