Findings

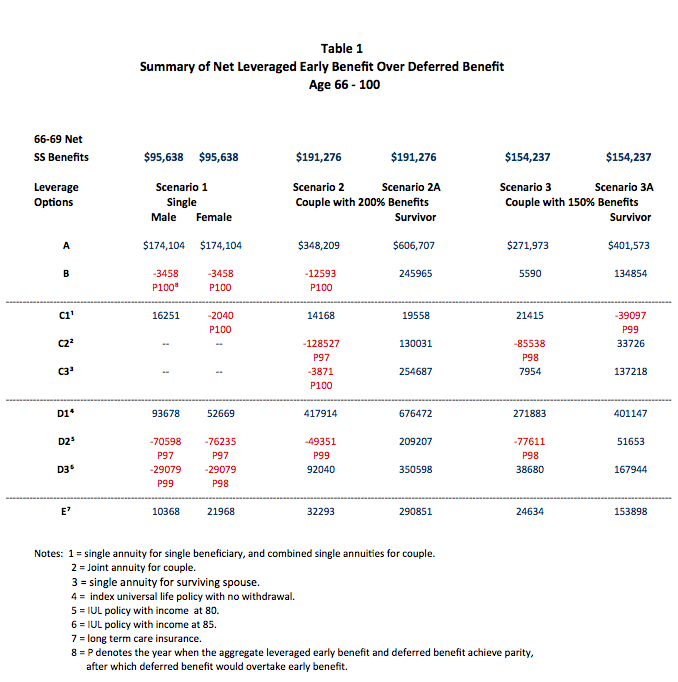

The results of the study are summarized in Table 1, which displays 50 potential outcomes. Thirty-six (72 percent) of the outcomes, marked in blue, indicate positive support for the strategy to age 100 and beyond. Fourteen (28 percent) of the outcomes, marked in red and P, show that leveraging the net benefits at age 66 in some cases would produce the same benefit as deferred Social Security benefits up to age 97. The overall result suggests that this leverage strategy unequivocally provides greater benefits to the beneficiaries until they are in the high nineties, and confirms that it would mitigate both mortality and longevity risks.

Not only does the strategy offer greater benefits, it in fact offers significantly greater benefits, depending on the leverage option selected. Twenty of the 36 positive outcomes register net benefits that exceed $100,000, ranging from $130,031 to $676,472.

The best outcomes are found in Scenario 2A, where the strategy consistently shows positive results across all leverage options. Since Scenario 2A denotes a survivor scenario, the result means that frontloading Social Security is actually highly beneficial to the surviving spouse, and is contrary to the conventional belief that delaying Social Security to 70 would ensure that the surviving spouse would get more income.