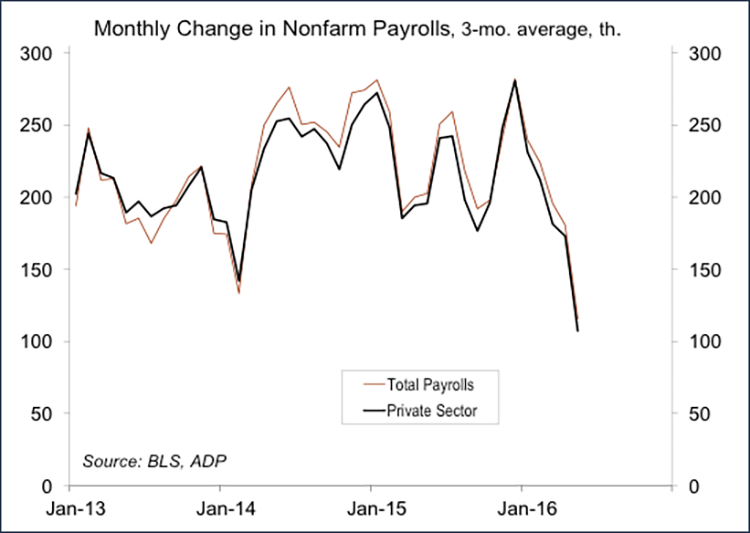

While the Brexit vote and initial reaction (over-reaction?) is behind us, there will be a lengthy and uncertain process of disentanglement from the European Union. Brexit has dominated the market action, but we should be seeing greater interest in the U.S. data. Recent figures suggest a pickup in economic growth in 2Q16. Running contrary to this strength, growth in nonfarm payrolls appeared to slow significantly in the first two months of the quarter. The question is why? This Friday, we should get answers. The July Employment Report will be the key driver for the near-term economic outlook.

Growth in payrolls was already expected to slow this year as the unemployment rate declined. We only need about 100,000 jobs per month to be consistent with the growth in the working-age population and much of the slack generated from the financial crisis has been taken up. Still, wage growth, while higher than in 2013 and 2014 (+2.0%), has remained relatively lackluster (+2.5% y/y). Anecdotally, firms report difficulty in finding qualified workers (that is, workers willing to work for what the firm wants to pay). With minimum wages moving higher, wage growth should pick up over time.

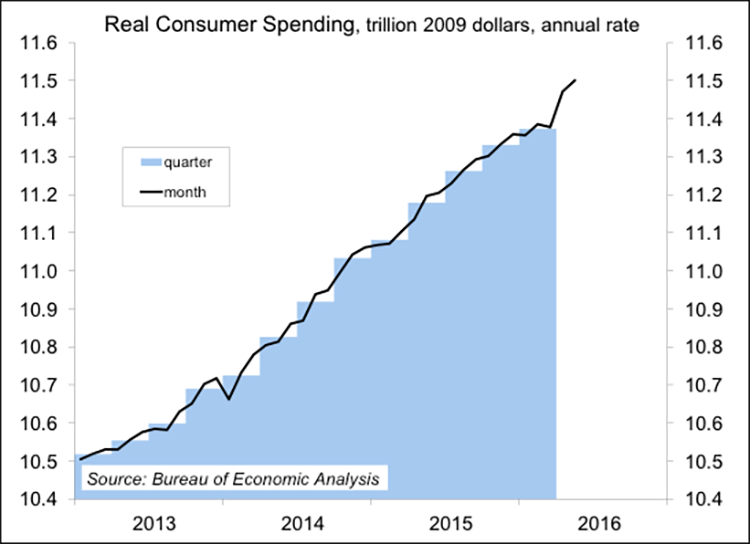

Capital spending rises and falls over the business cycle, but for the economy as a whole, the consumer drives the bus. Better wage growth ought to offset a slower trend in job growth and keep consumer spending on a moderately strong path.

Scott J. Brown, Ph.D., is chief economist at Raymond James & Associates.

Recall that nonfarm payrolls rose far less than expected in May (private-sector jobs up 25,000), while figures for March and April were revised lower. A strike at Verizon subtracted about 35,000, and while those workers will return in the June payroll total, payroll growth was still lower than expected. Mild weather may have pulled forward seasonal job gains. The soft May figure could represent statistical noise (the monthly change in payrolls is reported accurate to ±115,000). There could be issues with the seasonal adjustment (perhaps an earlier end to the school year). Amid uncertainty about Brexit and the presidential election, firms may have slowed their hiring, or perhaps firms have had a more difficult time finding qualified workers as the job market has tightened.

The early Easter shifted some spending from March to April. The May figures were moderately strong, suggesting a robust pace in second quarter spending. Granted, this follows a soft first quarter, but averaging the two quarters, inflation-adjusted spending growth is likely to have been close to a 3% annual rate in the first half of the year. Take that with a grain of salt. The upcoming annual benchmark revisions could alter that view.

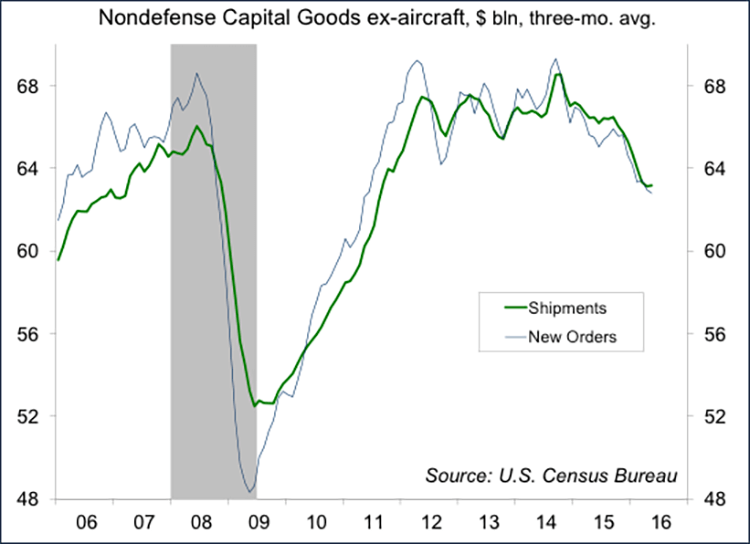

The one area of clear weakness in the economy has been in capital investment. Much of this weakness has been concentrated in energy exploration, which won’t fall forever (hence, will no longer be a drag on overall growth). Yet, ex-energy, business fixed investment has been relatively soft, consistent with a soft global economy and a slow patch in manufacturing, not an outright recession.