We are supposedly living in the Golden Age of television. Maybe yes, maybe no (my view: every decade is a Golden Age of television!), but there's no doubt that today we're living in the Golden Age of insurance commercials. Sure, you had the GEICO gecko back in 1999 and the caveman in 2004, and the Aflac duck has been around almost as long, but it's really the Flo campaign for Progressive Insurance in 2008 that marks a sea change in how financial risk products are marketed by property and casualty insurers. Today every major P&C carrier spends big bucks (about $7 billion per year in the aggregate) on these little theatrical gems.

W. Ben Hunt, Ph.D., is chief risk officer at Salient Partners.

This will strike some as a silly argument, but I don't think it's a coincidence that the modern focus on entertainment marketing for financial risk products began in the Great Recession and its aftermath. When the financial ground isn't steady underneath your feet, fundamentals don't matter nearly as much as a fresh narrative. Why? Because the fundamentals are scary. Because you don't buy when you're scared. So you need a new perspective from the puppet masters to get you to buy, a new "conversation", to use Don Draper's words of advertising wisdom from Mad Men. Maybe that's describing the price quote process as a "name your price tool" if you're Flo, and maybe that's describing Lucky Strikes tobacco as "toasted!" if you're Don Draper. Maybe that's a chuckle at the Mayhem guy or the Hump Day Camel if you're Allstate or GEICO. Maybe, since equity markets are no less a financial risk product than auto insurance, it's the installation of a cargo cult around Ben Bernanke, Janet Yellen, and Mario Draghi, such that their occasional manifestations on a TV screen, no less common than the GEICO gecko, become objects of adoration and propitiation.

For P&C insurers, the payoff from their marketing effort is clear: dollars spent on advertising drive faster and more profitable premium growth than dollars spent on agents. For central bankers, the payoff from their marketing effort is equally clear. As the Great One himself, Ben Bernanke, said in his August 31, 2012 Jackson Hole speech: “It is probably not a coincidence that the sustained recovery in U.S. equity prices began in March 2009, shortly after the FOMC's decision to greatly expand securities purchases.” Probably not a coincidence, indeed.

Here's what this marketing success looks like, and here's why you should care.

This is a chart of the S&P 500 index (green line) and the Deutsche Bank Quality index (white line) from February 2000 to the market lows of March 2009.

Now I chose this particular factor index (which I understand to be principally a measure of return on invested capital, such that it's long stocks with a high ROIC, i.e. high quality, and short stocks with a low ROIC, all in a sector neutral/equal-weighted construction across a wide range of global stocks in order to isolate this factor) because Quality is the embedded bias of almost every stock-picker in the world. As stock-pickers, we are trained to look for quality management teams, quality earnings, quality cash flows, quality balance sheets, etc. The precise definition of quality will differ from person to person and process to process (Deutsche Bank is using return on invested capital as a rough proxy for all of these disparate conceptions of quality, which makes good sense to me), but virtually all stock-pickers believe, largely as an article of faith, that the stock price of a high quality company will outperform the stock price of a low quality company over time. And for the nine years shown on this chart, that faith was well-rewarded, with the Quality index up 78% and the S&P 500 down 51%, a stark difference, to be sure.

But now let's look at what's happened with these two indices over the last seven years.

The S&P 500 index has tripled (!) from the March 2009 bottom. The Deutsche Bank Quality index? It's up a grand total of 10%. Over seven years. Why? Because the Fed couldn't care less about promoting high quality companies and dissing low quality companies with its concerted marketing campaign — what Bernanke and Yellen call "communication policy", the functional equivalent of advertising. The Fed couldn't care less about promoting value or promoting growth or promoting any traditional factor that requires an investor judgment between this company and that company. No, the Fed wants to promote ALL financial assets, and their communication policies are intentionally designed to push and cajole us to pay up for financial risk in our investments, in EXACTLY the same way that a P&C insurance company's communication policies are intentionally designed to push and cajole us to pay up for financial risk in our cars and homes. The Fed uses Janet Yellen and forward guidance; Nationwide uses Peyton Manning and a catchy jingle. From a game theory perspective it's the same thing.

Where do the Fed's policies most prominently insure against financial risk? In low quality stocks, of course.

It's precisely the companies with weak balance sheets and bumbling management teams and sketchy non-GAAP earnings that are more likely to be bailed out by the tsunami of liquidity and the most accommodating monetary policy of this or any other lifetime, because companies with fortress balance sheets and competent management teams and sterling earnings don't need bailing out under any circumstances. It's not just that a quality bias fails to be rewarded in a policy-driven market, it's that a bias against quality does particularly well! The result is that any long-term expected return from quality stocks is muted at best and close to zero in the current policy regime. There is no "margin of safety" in quality-driven stock-picking today, so that it only takes one idiosyncratic stock-picking mistake to wipe out a year's worth of otherwise solid research and returns.

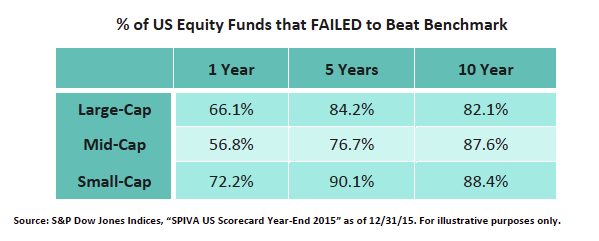

So how has that stock-picking mutual fund worked out for you? Probably not so well. Here's the 2015 S&P scorecard for actively managed US equity funds, showing the percentage of funds that failed to beat their benchmarks over the last 1, 5, and 10 year periods. I mean ... these are just jaw-droppingly bad numbers. And they'd be even worse if you included survivorship bias.

Small wonder, then, that assets have fled actively managed stock funds over the past 10 years in favor of passively managed ETFs and indices. It's a Hobson's Choice for investors and advisors, where a choice between interesting but under-performing active funds and boring but safe passive funds is no choice at all from a business perspective. The mantra in IT for decades was that no one ever got fired for buying IBM; today, no financial advisor ever gets fired for buying an S&P 500 index fund.

But surely, Ben, this, too, shall pass. Surely at some point central banks will back away from their massive marketing campaign based on forward guidance and celebrity spokespeople. Surely as interest rates "normalize", we will return to those halcyon days of yore, when stock-picking on quality actually mattered. 1 Year 5 Years 10 Year Large-Cap 66.1% 84.2% 82.1% Mid-Cap 56.8% 76.7% 87.6% Small-Cap 72.2% 90.1% 88.4%

Sorry, but I don't see it. The mistake that most market observers make is to think that if the Fed is talking about normalizing rates, then we must be moving towards normalized markets, i.e. non-policy-driven markets. That's not it. To steal a line from the Esurance commercials, that's not how any of this works. So long as we're paying attention to the Missionary's act of communication, whether that's a Mario Draghi press conference or a Mayhem Guy TV commercial, then behaviorally-focused advertising — aka the Common Knowledge Game — works. Common Knowledge is created simply by paying attention to a Missionary. It really doesn't matter what specific message the Missionary is actually communicating, so long as it holds our attention. It really doesn't matter whether the Fed hikes rates four times this year or twice this year or not at all this year. I mean, of course it matters in terms of mortgage rates and bank profits and a whole host of factors in the real economy. But for the only question that matters for investors — what do I do with my money? — nothing changes. Stock-picking still won't work. Quality still won't work. So long as we hang on every word, uttered or unuttered, by our monetary policy Missionaries, so long as we compel ourselves to pay attention to Monetary Policy Theatre, then we will still be at sea in a policy-driven market where our traditional landmarks are barely visible and highly suspect.

Here's my metaphor for investors and central bankers today — the brilliant Cars.com commercial where a woman is stuck on a date with an incredibly creepy guy who declares that "my passion is puppetry" and proceeds to make out with a replica of the woman.

What we have to do as investors is exactly what this woman has to do: get out of this date and distance ourselves from this guy as quickly as humanly possible. For some of us that means leaving the restaurant entirely, reducing or eliminating our exposure to public markets by going to cash or moving to private markets. For others of us that means changing tables and eating our meal as far away as we possibly can from Creepy Puppet Guy. So long as we stay in the restaurant of public markets there's no way to eliminate our interaction with Creepy Puppet Guy entirely. No doubt he will try to follow us around from table to table. But we don't have to engage with him directly. We don't have participate in his insane conversation. No one is forcing you keep a TV in your office so that you can watch CNBC all day long!

Look ... I understand the appeal of a good marketing campaign. I live for this stuff. And I understand that we all operate under business and personal imperatives to beat our public market benchmarks, whatever that means in whatever corner of the investing world we live in. But I also believe that much of our business and personal discomfort with public markets today is a self-inflicted wound, driven by our biological craving for Narrative and our social craving for comfortable conversations with others and ourselves, no matter how wrong-headed those conversations might be.

Case in point: if your conversation around actively managed stock-picking strategies — and this might be a conversation with managers, it might be a conversation with clients, it might be a conversation with an Investment Board, it might be a conversation with yourself — focuses on the strategy's ability to deliver "alpha" in this puppeted market, then you're having a losing conversation. You are, in effect, having a conversation with Creepy Puppet Guy.

There is a role for actively managed stock-picking strategies in a puppeted market, but it's not to "beat" the market. It's to survive this puppeted market by getting as close to a real fractional ownership of real assets and real cash flows as possible. It's recognizing that owning indices and ETFs is owning a casino chip, a totally different thing from a fractional ownership share of a real world thing. Sure, I want my portfolio to have some casino chips, but I ALSO want to own quality real assets and quality real cash flows, regardless of the game that's going on all around me in the casino.

Do ALL actively managed strategies or stock-picking strategies see markets through this lens, as an effort to forego the casino chip and purchase a fractional ownership in something real? Of course not. Nor am I using the term "stock-picking" literally, as in only equity strategies are part of this conversation. What I'm saying is that a conversation focused on quality real asset and quality real cash flow ownership is the right criterion for choosing between intentional security selection strategies, and that this is the right role for these strategies in a portfolio.

Render unto Caesar the things that are Caesar's. If you want market returns, buy the market through passive indices and ETFs. If you want better than market returns ... well, good luck with that. My advice is to look to private markets, where fundamental research and private information still matter. But there's more to public markets than playing the returns game. There's also the opportunity to exchange capital for an ownership share in a real world asset or cash flow. It's the meaning that public markets originally had. It's a beautiful thing. But you'll never see it if you're devoting all your attention to CNBC or Creepy Puppet Guy.

My Passion Is Puppetry

April 7, 2016

« Previous Article

| Next Article »

Login in order to post a comment