Rebalancing plays a crucial role in portfolio management, both to ensure that the overall risk of a portfolio doesn’t drift higher (since risky investments can out-compound conservative ones in the long run), and to potentially take advantage of sell-high, buy-low opportunities. But it’s not entirely clear how often a portfolio should be rebalanced to meet these goals.

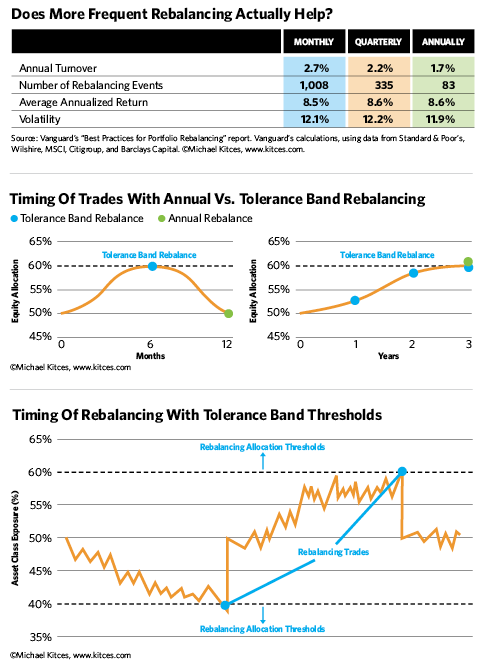

The conventional wisdom is to rebalance at least once per year, and possibly even more frequently. But more frequent rebalancing on average has little impact on risk reduction, even less benefit from a return perspective, and just racks up unnecessary transaction costs along the way.

Research suggests a superior rebalancing methodology is to allow portfolio allocations to drift slightly, and trigger a rebalancing trade only if a target threshold is reached. If the investments grow in line and the relative weightings don’t change, no rebalancing trade occurs. However, if these “rebalancing tolerance bands” are breached, the investment—and only the investment—that crosses the line is then bought or sold to bring it back within the bands.

This, however, requires ongoing active monitoring of the portfolio so you know when a threshold has been reached. Fortunately, a growing number of rebalancing software tools are available to help advisors track each investment and its rebalancing thresholds, and even to automatically calculate and queue up the rebalancing trades necessary to bring the portfolio in line again.

Optimal Rebalancing Time Intervals

In the long term, rebalancing serves an important function in keeping a portfolio targeted to the appropriate level of risk, since otherwise higher-risk investments that have higher long-term returns would become overweight by outperforming the lower-risk, lower-return investments.

In the short term, though, rebalancing presents the opportunity to generate better returns, because selling what’s overweight and buying what’s underweight typically is the same as selling high and buying low. In essence, the goal is to find investments that have moved to extremes, and trigger a rebalancing trade that buys/sells the investment just before it “snaps back” and reverts to its long-term average. If the investments are never rebalanced before the snapback occurs, the opportunity is lost.

Still, rebalancing can be done too frequently. For instance, if an investment is about to go on a huge run of outperformance for the year, rebalancing monthly would trigger a significant number of sales before the year’s gains have occurred, and thus the investor has missed a lot of the upside. Similarly, if an investment is about to decline in a yearlong crash, rebalancing monthly will have the investor repeatedly buying into a decline.

Very frequent rebalancing can also grind down its own long-term benefits as the transaction costs mount. The rule, then, is “often enough, but not too often.”

Which raises the question: How often?

Monthly rebalancing would appear to be too frequent. What about quarterly? Annually? How often do asset class returns shift their direction, and how would an investor optimize the timing of the rebalance?

Unfortunately, even with relatively “simple” asset classes like stocks and bonds the timing of market cycles is not consistent. It would be easier if bull markets always lasted the same amount of time—five years, for instance. But that’s not the case. Some bull markets are long with few or no corrections, while others are more volatile or shorter.

And bear markets tend to occur more quickly, so the optimal bear-market rebalancing cycle may be different.

Furthermore, as the number of asset classes expands, so too does the number of potential investment cycles to optimize, and they will virtually never be fully in sync with one another.

A study by Vanguard basically found no material differences in outcomes for rebalancing frequencies varying from monthly to annually, when they were measured over rolling periods. Using a 60/40 portfolio going back to 1926, the researchers found that rebalancing quarterly or monthly produced no improvement in the long-term risk or returns; it simply drove up the turnover rate and the number of rebalancing events (and potential transaction costs).

Allocating With Tolerance Bands

Conceptually, the goal of rebalancing is to sell an investment after it has fully (or at least mostly) had its favorable run, and similarly to buy an investment after it has fully (or at least mostly) declined. Yet as noted, because a diversified portfolio has a wide range of investments, which do not necessarily peak and trough over the same intervals, it’s difficult to find an optimal rebalancing frequency.

An alternative, however, is to change the process, rebalancing not on a time table, but according to how “out of whack” an investment or an asset allocation has become.

For instance, a portfolio targeted at 50% equities and 50% bonds might rebalance whenever the total equity exposure grows above 60% (a threshold signaling a significant outperformance of stocks over bonds, implying that they might have become overvalued).

It doesn’t matter if it takes six months or three years, the rebalancing wouldn’t occur until the equities reached the 60% threshold. This ensures that the stocks are not sold “too early” while they’re still rising.

Conversely, there would be a “buy” trigger if equities were to decline—say, if the equity exposure started at 50% but fell below 40% in a bear market. The purchase, again, depends on the threshold—and doesn’t happen until the stock weighting passes under the 40% mark, whether that takes six months or 24 months (even during a bear market).

Thus, with “allocation tolerance bands,” a portfolio targeting 50% in equity exposure would now trigger a rebalancing trade if the equity allocation fell below 40%, or above 60%. Anywhere in between those thresholds and the portfolio simply remains a buy-and-hold strategy.

It is important to note that the allocation bands are based not on dollar amounts nor appreciation but only on portfolio allocation percentages. The distinction is important, because investors shouldn’t be rebalancing simply because investments decline or appreciate in value. In a portfolio where everything is up by 15%, the weightings would be the same, and no rebalancing trade should occur. In other words, it’s not favorable investment performance but relative outperformance that should trigger a rebalancing trade.

That approach in a portfolio with multiple asset classes will also help to reduce the volume of rebalancing trades (and therefore save on transaction costs). For instance, if there are five investments in the portfolio and only one of them dramatically outperforms—enough to reach the threshold and become overweight—only that investment will be sold and rebalanced. An investor, on the other hand, who simply rebalances every investment in the portfolio annually—even if it only needed a 0.1% trade—would be accruing wasteful transaction costs.

Setting Thresholds For Rebalancing Bands

While the concept is relatively straightforward, the question still arises, what exactly would the optimal threshold levels be for those tolerance bands? Investors must still apply a uniform rule, as they do with time-based rebalancing. Making the tolerance bands too wide or too narrow can also have deleterious effects.

For instance, should an investment or asset class only be rebalanced when its allocation moves more than 10 percentage points from its original target (e.g., an investment with a 50% allocation gets thresholds at 40% or 60%)? Or should it be set even wider, at 15%, to allow more room for favorable investment performance to be extended (and for a declining market to “finish” its decline)?

But absolute allocation bands become problematic in certain instances. If the portfolio is diversified across 10 different investment positions, each one has only a 10% allocation in the first place, so plus or minus 10% would be a range between 0% and 20%, which would require very extreme portfolio changes to ever trigger a trade (the investment would actually need to generate more than double the returns of its peers to generate a 10 percentage point overweight, or would have to crash to zero to be 10 percentage points underweight).

Of course, the target allocation bands could be made smaller for such portfolios—for example, an investor could set the targets at only 3%. Moving from 10% to 13% would still be a very big relative move—but it works well when all the positions in the portfolio have similar allocations.

For instance, if the portfolio is a “core-and-explore” approach with 50% in a core equity position, and a series of five satellites with 10% each, the 3 percentage point band would trigger the satellites to rebalance at 7% or 13%, but the core equity position will rebalance at 47% or 53% (which, given the relative size of the position, will be triggered far more often). Which means the satellites would have to outperform or underperform enough to change their weighting by 30% to be rebalanced, while the core would need far less relative under- or outperformance for a trade to occur.

An alternative approach is to simply scale the allocation bands relative to the size of the portfolio positions in the first place. For instance, rebalancing might occur anytime the investment’s weighting moves more than 20% from its original target weighting. So if the investment’s original allocation was 50%, and 20% of that is 10%, then the portfolio would be rebalanced when the investment’s weighting moves up to 60% (50% + 10%) or down to 40% (50% - 10%). On the other hand, if it was only a 10% allocation, the rebalancing trade would occur at thresholds that are 20% of the 10%, which means rebalancing would occur at 8% or 12%. Either way, the investment must effectively outperform all the others by approximately 20% on a relative basis to cause its relative weighting to drift above or below the thresholds (regardless of the weighting it started at).

That means any one particular investment moving to a high or low extreme will be sold or bought accordingly, because its performance is so different than everything else. The time-rebalanced portfolio, on the other hand, forces a rebalancing transaction for all investments in the portfolio, whether or not these investments need it. The new way allows you to “trim” an investment in the midst of a strong run, and purchase one that has just crashed (relative to the others).

Which Thresholds?

The key is to set the thresholds wide enough that they don’t trigger an excessive volume of trades (which rack up costs), don’t repeatedly curtail positive momentum, and don’t amplify a crash. At the same time, they must not be set so wide that no trades are triggered at all (the point of rebalancing would be lost).

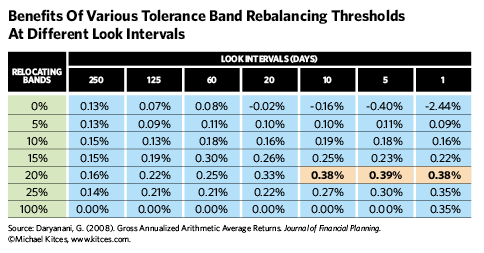

A 2007 study in the Journal of Financial Planning by Gobind Daryanani entitled “Opportunistic Rebalancing” studied rolling five-year periods from 1992 to 2004 and found that the optimal rebalancing threshold was at a relative threshold of 20% of the investment’s original weighting. Setting the thresholds narrower, at only 10% or 15% bands for example, produced less favorable results, as did setting the bands at 25%.

The goal, again, is to set a threshold that is “far enough out” to allow investments to run near extremes, but not so far that they run to extremes and bounce back again, without ever triggering a buy or sell trade.

The 20% relative rebalancing bands in the Daryanani study, which was based on a 60/40 portfolio (using five asset classes, including large-cap U.S. stocks, small-cap U.S. stocks, REITs, commodities and intermediate-term bonds), was sufficient to ensure that total equity exposure never drifted more than 5% from the original 60/40 allocation.

If fact, Daryanani ultimately found that this threshold-based rebalancing was so effective that the best strategy was to “look constantly” to see if there were any rebalancing opportunities (i.e., if the thresholds had been breached), even if it might be weeks, months or years without actually triggering a trade. Checking less often—particularly any less frequently than once every two weeks (every 10 trading days)—resulted in diminished rebalancing benefits. By looking often, investors can even increase overall returns, despite the fact that doing so curtails the long-term compounding of equities over time.

The Vanguard study also found that threshold rebalancing can slightly help returns, though it used narrow bands with a 5% absolute threshold (from a baseline 60/40 portfolio).

The caveat is that it’s necessary to do regular checks for rebalancing opportunities, which means using tools like iRebal, tRx (Total Rebalance Expert) or Tamarac (or perhaps a robo-advisor that employs a similar threshold-based rebalancing approach).

For those with the technological means, the tolerance threshold approach appears to be a more effective rebalancing strategy, both in terms of the timing and execution of trades.