The day after the market crashed on October 19, people began to worry that the market was GOING to crash. It has already crashed and we’d survived it (in spite of our not having predicted it), and now we were petrified there’d be a replay. Those who got out of the market to ensure that they wouldn’t be fooled the next time as they had been the last time were fooled again as the market went up.

The great joke is that the next time is never like the last time, and yet we can’t help readying ourselves for it anyway. This all reminds me of the Mayan conception of the universe.

In Mayan mythology the universe was destroyed four times, and every time the Mayans learned a sad lesson and vowed to be better protected—but it was always for the previous menace. First there was a flood, and the survivors remembered it and moved to higher ground into the woods, built dikes and retaining walls, and put their houses in the trees. Their efforts went for naught because the next time around the world was destroyed by fire.

After that, the survivors of the fire came down out of the trees and ran as far away from woods as possible. They built new houses out of stone, particularly along a craggy fissure. Soon enough, the world was destroyed by an earthquake. I don’t remember the fourth bad thing that happened—maybe a recession—but whatever it was, the Mayans were going to miss it. They were too busy building shelters for the next earthquake.

Two thousand years later we’re still looking backward for signs of the upcoming menace, but that’s only if we can decide what the upcoming menace is. Not long ago, people were worried that oil prices would drop to $5 a barrel and we’d have a depression. Two years before that, those same people were worried that oil prices would rise to $100 a barrel and we’d have a depression. Once they were scared that the money supply was growing too fast. Now they’re scared that it’s growing too slow. The last time we prepared for inflation we got a recession, and then at the end of the recession we prepared for more recession and we got inflation.

. . . This ‘penultimate preparedness,’ is our way of making up for the fact that we didn’t see the last thing coming along in the first place . . .

One Up On Wall Street, Peter Lynch, formerly of Fidelity-Magellan Fund

Well, this time around you can take your pick about the “upcoming menace” from: A) Recession; B) Banking Crisis; C) War in the Middle-East; D) Inflation or Deflation; E) Presidential race; F) All of the Above, and more. The consensus pick is obviously “F” All of the above, and more. Indeed, most investors believe in their hearts that we haven’t seen the stock market low, or that we are not even in a bull market. More importantly, they are also guarding their investment pocketbooks because they can’t understand how the stock market can make a real bottom before resolving the various “menaces.” What they fail to appreciate is that the Wall Street financial markets are a discounting barometer. In other words, that is what the Dow Dive from last November’s nearly 18000 “print” to the mid-January 2016 “print low” (~15450), approximately 2500 intraday points, was all about!

The problems have been so widely publicized in the financial media that they have become popular fare in the network TV circles, in the print media with everyday columnists articulating those problems, and even my 85-year old Aunt Doris called to ask if the world is coming to an end? She called asking if the banks are safe, is real estate going to crash, is ISIS going to take over the world, will there be war with North Korea or in the Middle East, etc. I reassured her that her bank was not going broke, that her house value is not going to zero, that ISIS is not taking over the world, that if there is a war it wouldn’t be anything like WW II . . . even with a new offensive option against ISIS.

My point is, if all the popular media venues know all the negatives, and the negatives are the new media feature, then 90%+ of our problems are already baked into stock prices. So, anyone waiting for the resolution of all the negatives before buying is completely ignoring the stock market’s historical role as a discounting barometer, not to mention the confirmation from my Aunt (bless her)! Speaking to this point was none other than Julieta Yung, an economist in the research department at the Fed Bank of Dallas, and Michael Antonelli. To quote them, as written in Pensions & Investments:

“Short-term fluctuations in equity prices come too fast and furious and are caused by such a multitude of inputs that assuming they’ll directly translate into changes in real economic output is an error,” Ms. Yung wrote. Michael Antonelli, a trader at Robert W. Baird & Co., says “Big swings often just reflect human emotions. The two can disconnect in the short-term because of the immediate effect sentiment has on stocks. Then that nervousness wanes, and people capitulate, and that’s when you see the market come back.”

Indeed, “Short-term fluctuations in equity prices come too fast and furious,” and that was certainly the case last week as the D-J Industrial Average (INDU/17535.32) whipsawed its way through the week with Monday – Friday gains/losses like these: -35, +222, -217, +9.38, -185, which drove the day-trading crowd nuts. By week’s end the Doleful Dow had lost more than 200 points, and in the process broke below its May and April reaction lows. That action leaves the Industrials in negative territory for the year once again, and the S&P 500 (SPX/2046.61) darn close to doing the same. While the SPX has not violated its respective May/April reaction lows, it did break below its 10-day moving average (DMA) that we worryingly wrote about in last Friday’s Morning Tack. It also broke below its 50-DMA, which suggests it has “eyes” for its 200-DMA at 2012. Of course that would fit nicely with our model, which telegraphed a decline into last week (∓ 3 sessions), with a target of 1990 – 2000, when the SPX did not follow the S&P 500 Total Return Index to new all-time highs four weeks ago.

Within the “bookends” of the week the retail sector got slammed, leaving the retail indices down some 20% YTD. In the past this has been a modest warning signal for the overall stock market. Yet the real star for the week was the energy complex with crude oil up 3.66%, natural gas better by 5.98%, and gasoline soaring some 6.23%. Surprisingly, most energy stocks did not dance higher with the surge in energy commodities. Indeed, last week was a pretty weird week, but should have come as no great surprise given what our model has been telegraphing.

The call for this week: The stock market’s recent manic depressions have been centered on the word “recession.” I have repeatedly written that I see NO signs of an impending recession. In Barron’s over the weekend, my friend Sam Stovall (S&P Capital IQ and son of the legendary keeper of the GM indicator Bob Stovall), wrote:

“Granted the current [economic] expansion is the forth longest since 1900 and lasted more than twice the median duration of the prior 21. Yet we think this worry is premature, and put the likelihood of slipping into a recession during the remainder of President Barack Obama’s second term in office at 15% to 20%.”

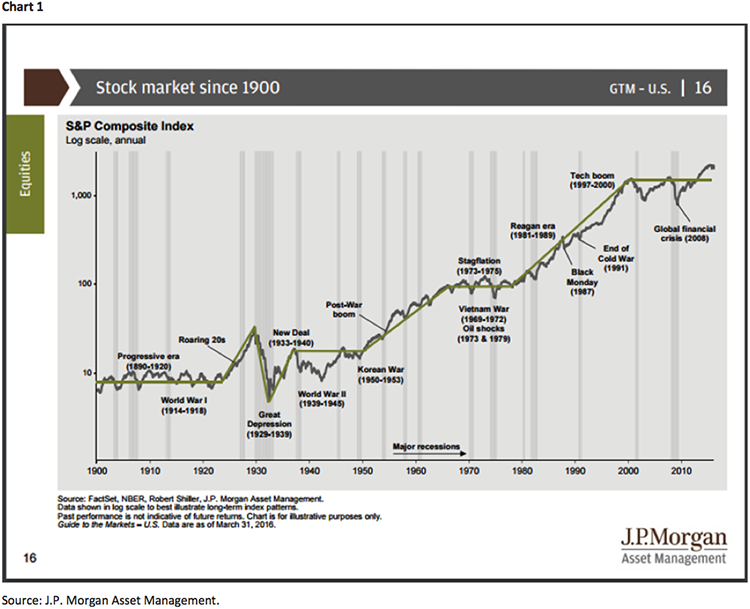

Plainly we agree! Worth noting is that in the past three years, paycheck income has increased by a 4.3% annualized rate, far better than the real GDP growth rate. Moreover, every other semi-truck I see has a sign on the back saying “drivers needed” (buy the trucking stocks recommended by our analyst); and, every other fast food restaurant my grandkids want to stop at has a sign reading “Help Wanted.” These are not the kind of things you see in front of a recession. Clearly, Andrew and I attempt to “call” the near-term wiggles in the equity markets. However, we have NEVER wavered in our belief that the secular bull market remains alive and well. Just look at the attendant chart on the next page and observe that every market peak has subsequently been surmounted with higher prices. We have no doubt that will be the case this time. Our model was looking for a meaningful “low” last week, or early this week (∓ 3 sessions), so stay nimble on a trading basis. Longer-term, this is still a secular “bull market.”

Jeffrey D. Saut is chief investment strategist at Raymond James.