Despite these issues, Gabelli and his firm's longtime utility analyst Tim Winter cite a number of other reasons why the group's solid run since the beginning of the year should continue.

Reasonable stock prices. Based on estimated 2012 earnings and their attractiveness to investors in a slow-growth, low-interest-rate environment, Winter believes the stocks are "reasonably priced, if not undervalued." Currently, the group is trading at around 14.5 times 2012 earnings estimates, slightly higher than the midpoint of its historic range of 10 times to 17 times forward earnings over the last 20 years. He admits that while higher interest rates pose a threat, the market has already factored that possibility into stock prices.

The potential for modest earnings growth. Unusually hot weather, recovering industrial sales, and cost-control efforts helped utilities post unusually strong earnings growth of 8.7% in 2010.

Winter sees more modest but stable annual growth at around 4% to 6% over the next several years. "As the economy continues to recover slowly, earnings growth should be modestly higher than both GDP growth and the retail electric demand growth rate," he says.

The capacity to maintain or increase dividends. In 2010, electric, water and gas utilities raised their annual dividend rates by 4%, 3.8% and 2.8%, respectively.

"Current dividend payouts are approximately 60% of forecast earnings for 2011, which provides a comfortable margin for dividend maintenance and growth," says Gabelli. "Over the next several years, investors can expect dividend growth above recent inflation rates."

The ability to raise rates and access capital. Despite the recession, utilities have been able to raise their rates to keep pace with inflation, and federal and state authorities are likely to allow them to continue doing so to help offset the cost of investment in generation and transmission facilities. With their healthy balance sheets, solid credit ratings and rapid depreciation schedules, they shouldn't have much trouble tapping the capital markets to raise money, says Winter.

The increased use of cheap natural gas. Coal-fired generation produces roughly 45% of U.S. electricity, while natural gas generates 25%; nuclear 20%; and hydro, wind and solar approximately 10%. But the public's concern about the pollution of coal-burning plants and its wariness of nuclear power mean that facilities utilizing natural gas, a cheap fuel source over the last several years, will likely represent the majority of new building projects.

Merger and acquisition activity. Consolidation has emerged as an investment theme over the last couple of years as smaller utilities experience increased pressure to deliver cleaner energy at cheaper prices. Gabelli believes that trend will continue as utilities seek to increase scale or enter new markets. "The small companies, as well as some larger ones, are selling out at premium prices as the cost of staying in the game rises," he says. "And as policy makers understand the new economic dynamics of the industry, the lengthy merger review and approval process appears to be easing."

Even with 90 completed utility mergers and acquisitions since 1993, there are still about 60 electric utilities and 30 gas utilities. "From the standpoint of economic efficiency, that's about 50 more than we need," notes Gabelli.

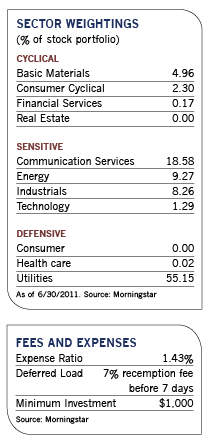

A major fund focus for several years has been financially stable, reasonably priced small-cap and midcap utilities that are likely acquisition targets for larger utilities. Some of its best performers so far this year have been acquisition targets such as Constellation Energy and Central Vermont Power Service.