First quarter earnings results will not be very exciting, but the earnings trajectory may be at a trough. We would love to say that this earnings season, which begins on April 11, 2016 (unofficially), will bring better results than recent quarters, but that appears very unlikely. In fact, consensus estimates are calling for a 7% year-over-year decline in S&P 500 earnings for the quarter, the worst decline since the Great Recession and the third straight quarterly decline based on Thomson data (based on FactSet data, it’s the fourth). By most definitions, corporate America is in the midst of an earnings recession. Hardly something for investors to get excited about.

But on a brighter note, this quarter may mark an inflection point regarding the trajectory of earnings because the pressure on earnings from oil weakness and U.S. dollar strength is starting to abate. But that also means management teams’ popular excuses for explaining shortfalls won’t work anymore.

No More Excuses

In 2015, the combination of oil weakness and U.S. dollar strength wiped away high-single-digit S&P 500 earnings growth. Oil fell from over $100 per barrel in 2014 to as low as $26 in February 2016; while the U.S. dollar’s gains, which erode profits earned overseas, reached 20% during the second quarter of 2015. These two factors provided excuses for management teams whose results came up short.

But these drags have already begun to abate and are poised to potentially stage powerful reversals. The reversal has begun quicker for the dollar [Figure 1]. After annual increases between 12% and 20% during each of the four quarters of 2015, which delivered estimated 3–6% hits to S&P 500 earnings, the U.S. Dollar Index gained just 2% during the first quarter of 2016. If the dollar stays flat between now and year-end, 2–3% year-over-year declines will be an earnings tailwind during the remaining three quarters of the year.

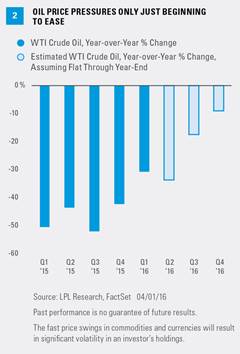

The oil reversal should take longer to play out, but the annualized declines have started to moderate and could reverse during the second half of the year if oil prices move reasonably higher from current levels. Figure 2 shows that if oil prices remain at current levels the rest of the year, year-over-year declines in average oil prices would continue through 2016. However, should oil prices return to the mid- to high $40s as we expect, oil may potentially begin to experience annual gains during the third quarter of this year. Consensus estimates are already reflecting energy’s return to year-over-year earnings gains in the fourth quarter of 2016, and oil prices are currently up about 40% off of their February 2016 lows, so the wait for better earnings news from the sector may not be too far off.

Corporate America has already lost its ability to use currency as an excuse, while the oil excuse is beginning to lose credibility. Hopefully, less reliance on these excuses will enable markets to get more useful, and better, information about business conditions.