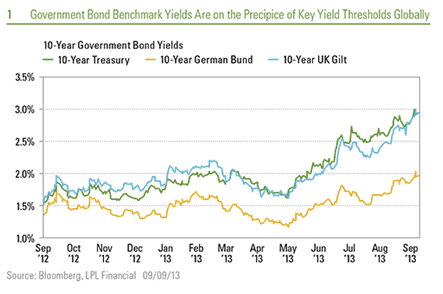

Several global bond benchmarks, led by the U.S. 10-year Treasury yield, attempted to breach key barriers last week as the bond market sell-off entered its fifth month. The U.S. 10-year Treasury yield touched 3.0 percent, as did 10-year government yields in the United Kingdom, and the 10-year German yield broke above 2.0 percent briefly [Figure 1]. A below-forecast August employment report, released last Friday, September 6, 2013 sparked a late-week turnaround in high-quality bond prices globally but not nearly enough to offset another week of higher yields and lower prices. Price gains continued on Monday, September 9, 2013 but look tentative ahead of this week’s bond market tests.

Auction Tests

Corporate bond issuance will compete with Treasury bonds for investor demand with the largest investment-grade rated corporate bond issue expected mid-week from Verizon. Verizon’s multi-part debt sale is expected to exceed Apple’s record $17 billion debt sale in April of this year and comes at a time when high-quality bond prices are not far from the lows of the sell-off. Similar to the Treasury auctions, demand for longer-term issues will provide a good snapshot of investment demand.

The company names mentioned herein are for educational purposes only and are not a recommendation to buy or sell that company nor an endorsement for their product or service.

Not to be left out, foreign bond sales will also be of interest this week. Although much smaller amounts, intermediate- to long-term government bond auctions in the United Kingdom, Germany, and Italy Tuesday through Thursday of this week will test investor demand globally.

Strong demand may be a sign that the recent rise in yields has gone far enough to compensate for a possible reduction in bond purchases that may be announced at the conclusion of next week’s Federal Reserve (Fed) meeting. Conversely, weak demand would indicate the current level of yields does not fully compensate for potential Fed uncertainty, not only regarding tapering, but also for the timing and degree of future interest rate hikes. In this latter case, the break of key yield thresholds, such as 3 percent on the 10-year, may undermine sentiment in the bond market and lead to additional weakness.

As mentioned in last week’s commentary (Bond Market Perspectives: Summer Fling), market expectations over the timing and degree of Fed interest rates increased dramatically as a result of the bond pullback. According to fed fund futures, a first 0.25% rate increase by the Fed was fully priced in by December 2014, well ahead of Fed guidance and the most aggressive pricing since the sell-off began until the soft jobs report caused expectations to recede. Still fed fund futures reflect a bias the Fed will hike interest rates by the fourth quarter of 2014. While the bond market has braced for a more aggressive Fed, any strength may be limited until the market receives additional clues at the conclusion of next week’s Fed meeting.

The 30-year Treasury Holds Its Ground Government bond benchmarks globally have reached key psychological barriers that may help stabilize high-quality bond markets or usher in additional weakness.

Government bond benchmarks globally have reached key psychological barriers that may help stabilize high-quality bond markets or usher in additional weakness.

A full slate of new issuance may shed light on investor appetite for still-higher yields and may help determine the near-term course of the bond market.

Global bond yields moved in response to better economic data. Despite the U.S. jobs report, which showed a slower-than-anticipated pace of job growth, economic data globally was generally upbeat. In the United States, both the Institute for Supply Management (ISM) manufacturing and services survey indexes soundly exceeded forecasts and pointed to better economic growth. In Europe, August Purchasing Managers’ Index data, similar to the ISM in the United States, surpassed expectations even in the depressed economies of Spain and Italy. While the economies of both countries have a long road ahead to recovery, the reports were another sign the worst may be behind Europe. Finally, better data from China helped round out the theme of an improving global economic backdrop, which pressured yields higher.

Bond market focus falls on new bond sales this week amid relative quiet on the economic front. Demand for new bonds may help determine whether recent barriers will hold or prove only to be a speed bump in the global bond sell-off. The main event occurs domestically with another round of 3-, 10-, and 30-year Treasury auctions, which kick-off Tuesday, September 10, 2013. The 10-year Treasury auction Wednesday and the 30-year auction on Thursday will be the focus. Investor demand for longer-term, more interest rate sensitive bonds is usually one of the better tests of market demand.

While short- and intermediate-term Treasury yields increased to new highs last week, the 30-year Treasury did not [Figure 2]. The fact that the 30-year Treasury did not break out to a new yield high last week is a preliminary sign investors may not require still-higher yields, at least in this segment of the market. If it holds, stabilization among longer-maturity bonds may spread to other parts of the bond market. Even beaten down municipal bonds were more resilient last week and outperformed Treasuries for the first time since early July, a sign that investor interest is returning.

However, these signs of stabilization are very tentative and while signs of value are present in the bond market, more is needed to signal that the bond sell-off is over. This week’s debt sales may provide directional cues ahead of next week’s Fed meeting.

Anthony Valeri has been with LPL Financial since June 1993. As Senior Vice President and Market Strategist, Valeri is a member of the Research department’s tactical asset allocation committee and is responsible for developing and articulating fixed income and general market strategy.

Reaching Barriers

September 11, 2013

« Previous Article

| Next Article »

Login in order to post a comment