The choice between a conservative and aggressive investment strategy is often difficult. Should advisors recommend a conservative strategy in order to achieve a modest financial goal when a client's assets are modest, or an aggressive strategy that promises to increase those assets? Alternatively, should they recommend a conservative strategy to achieve ambitious goals when assets are ample, or aggressive strategies promising to achieve even greater goals?

In competitive sports, a team falling behind in a contest often becomes more aggressive in order to defeat its opponents, while a team well in the lead becomes more conservative to preserve the lead and minimize the risk of injury to its players. Can this analogy be applied to investment situations when achieving specific financial goals is critical?

In last September's Financial Advisor, we described a household balance-sheet approach that matches clients' financial resources to the future liabilities implied by those goals in order to construct portfolios that meet them. For example, if the client needs to meet mortgage payments, then investments in zero-coupon bonds with equivalent maturities could be used to match those payments. If a client's resources are inadequate to meet his retirement income goal, then he might be advised to extend his working years beyond those initially planned.

We did not consider this approach controversial. Yet some readers took exception, and said a more aggressive strategy should be adopted for a client, even if it means assuming greater risk and the possibility of failing to achieve critical life goals.

Meeting The Challenge

In order to determine the efficacy of the two approaches (household balance-sheet matching versus more aggressive strategies) we ran additional tests that confirmed our position.

In general, the household-balance-sheet approach provides optimal portfolios for clients across a broad demographic spectrum, irrespective of their resources and capital market performance. Specifically, we find that the approach has the following advantages:

1. It provides a holistic view of investors' resources and goals, which results in more reliable portfolio construction and asset allocation. Rather than an asset-only approach aiming to beat some arbitrary benchmark, it first identifies client goals, then inventories their resources and finally develops an optimal strategy to most efficiently fund those goals.

2. It yields asset allocations more resilient to the vagaries of future asset returns, which no one can predict with consistent accuracy.

3. It quantifies the margin of safety between a client's resources and commitments rather than using a psychological risk questionnaire to assess the client's aversion to risk.

4. It is robust and flexible enough to accommodate various wealth levels, from average to affluent, resulting in portfolio recommendations tailored to each client's life situation.

5. It ensures that investors will continue to meet necessary life goals, irrespective of the performance of the capital markets, by prioritizing goals, starting with those that are necessary and then moving along to those that are merely desirable.

Methodology

To generalize the results over a wide range of investors, three demographic groups were selected: younger single persons, middle-aged couples with family responsibilities, and older couples approaching retirement. The groups were then each further divided into those who were "average" and those who were "affluent." The financial characteristics used to define each demographic are income, asset levels, household value, mortgage and living and retirement expenses. The life goals and risk tolerances are given realistic parameters for each of the six investor demographics. Each is evaluated under "strong" and "weak" capital markets scenarios, as defined by market experience over two different ten-year periods.

A portfolio was constructed for each of the three demographics, with two types of resources, in two different market scenarios-and together these yielded 12 different portfolios. They were evaluated according to whether the targeted goals were likely to be met. The weak and strong scenarios were then used to determine whether the ex post performance of the asset/liability matching versus aggressive approaches met the demographics' necessary goals.

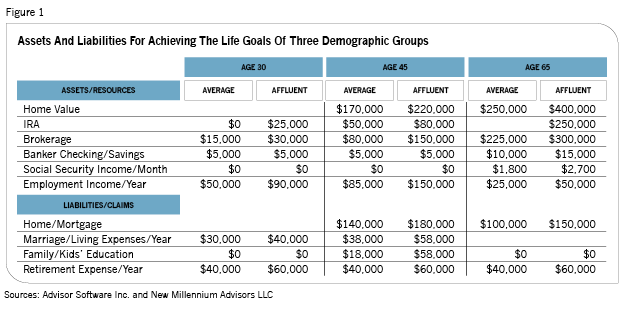

Two investors in each of the three demographics (ages 30, 45 and 65) were assumed to have the household financial assets and future liabilities implied by their life goals displayed in Figure 1.

The first demographic is young, single persons, age 30. Their retirement is about 35 years away, with most of their earnings years ahead of them. Their goals are likely to be financing a home or condo close to their work, marrying in the future, raising a family and retiring. We sought the most suitable portfolios for two young investors. The average one is assumed to have $20,000 in brokerage and bank accounts and an annual income of $50,000. The affluent one has assets of $60,000 and an annual income of $90,000. For simplicity, both are assumed to have similar retirement goals.

The second demographic is middle-age couples, age 45. Their retirement is about 20 years away and they have 25-year life expectancies beyond that. They have two children whom they want to give college educations. The average couple has assets of $305,000 and income of $85,000, and the affluent couple has assets of $455,000 and a second salary. Both couples are assumed to have similar retirement goals.

The third demographic is older couples, age 65, with 25-year life expectancies. Their children have grown and left them empty nesters. They have downsized their primary residences and wish to leave a bequest to their heirs. The average couple has assets of $485,000 and an annual Social Security income of $20,600, and the affluent couple has $965,000 and Social Security income of $32,400.

Selecting Weak And Strong Capital Market Scenarios

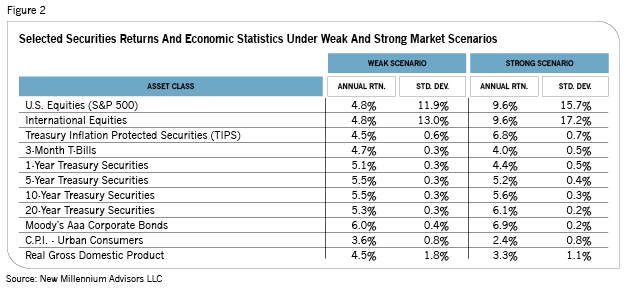

Two ten-year periods over the last 60 years were chosen, one whose below-average equity returns were half those of the above-average second period. The S&P 500's compound annual return over the 60 years from 1950 to 2010 was 7.2%. The ten-year period from February 1999 to February 2009 had below-average annual return of 4.8%. This period is defined as the weak one. In the ten-year period from December 1988 to December 1998, the S&P 500 had an above-average return of 9.6% (the strong scenario).

Figure 2 compares the stock and bond market returns and standard deviations against the economic background over those two distinct periods.

Analytical Results

A number of factors are generally known to influence asset choices. Affluent investors exhibit a marked preference for equities due to the greater returns relative to fixed income and the fact that they can afford taking greater risk. In contrast, average investors generally exhibit a preference for fixed income since they cannot afford the additional risk equities represent. Capital market assumptions also influence the choice of asset classes; greater returns in strong market projections favor equities while the lower returns in weak market projections favor fixed income. In addition, as investors age, their preference for fixed income increases as their risk tolerance decreases. Our study results are consistent with these views.

Figure 3 contains the estimated returns of optimized goal-based portfolio allocations if the weaker scenario in Figure 2 wins out. Each investor's goals are divided into "necessary" and "desired" priorities. For the purposes of this study, 80% of the expenses are defined as necessary, and the remaining 20% as only desired. Not surprisingly, average investors have smaller margins of safety in weak markets, indicating that their life goals are less affordable than affluent investors'.

Fixed income and inflation-protected Treasurys (TIPS) appear in all three average investor portfolios. However, TIPS do not appear in the affluent portfolios. Differences in the returns between the average and affluent portfolios are the result of the 3.57% annual inflation rate, which increases TIPS' returns.

"Without goals" asset allocations are provided to contrast the goal-driven solutions. These portfolios hold only fixed-income allocations that result in lower estimated returns, as shown in the figure.

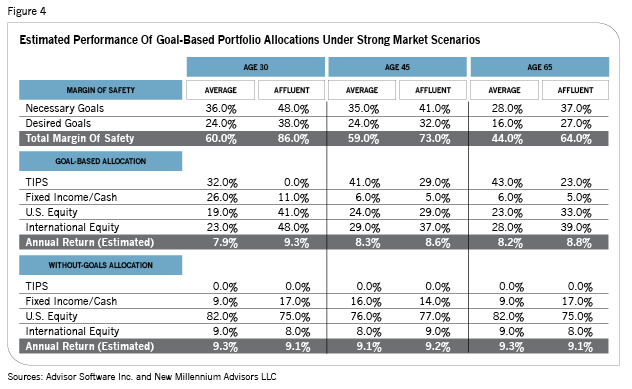

Figure 4 contains the estimated returns of optimized goal-based portfolio allocations in line with the strong scenario projections in Figure 2. Greater allocations for U.S. and international equities in the affluent portfolios are due to their greater expected returns, resulting in their high margins of safety. Equity allocations in the average portfolios are smaller, which accounts for their lower returns and margins of safety. However, their fixed income and TIPS allocations serve to cover necessary life goals with less risk. As might be expected, without-goals portfolios are heavily concentrated in equities, which accounts for their greater returns.

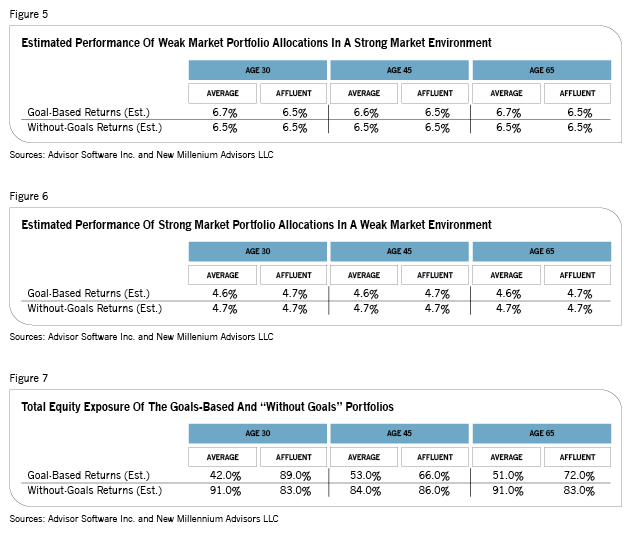

A more interesting situation develops in Figure 5. Portfolio allocations are optimized using weak market scenario projections, but then there's a strong market. The asset weightings in these portfolios are the same as shown in Figure 3, but the returns are those of the strong projections in Figure 2. The TIPS allocations in the average investors' portfolios provide slightly greater returns than the fixed-income and cash allocations in the portfolios of the affluent investors and those without goals.

The opposite situation is described in Figure 6, where portfolio allocations are optimized according to strong scenario projections but there is a weak market. The asset allocations in these portfolios are the same as those in Figure 4, but the returns are those related to the weak scenario in Figure 2. This is equivalent to adopting an aggressive strategy just before a weak market. All portfolios exhibit similar returns despite considerably different asset allocations. The results are due to the similar returns in equities (4.8%), TIPS (4.5%) and fixed income (4.2%).

However, the higher standard deviations of U.S. and international equities make the goals-based affluent portfolios and "without goals" portfolios more vulnerable to losses in weak equity markets than the goals-based average portfolios.

The total equity exposures in these portfolios appear in Figure 7. Equity exposures in the average goals-based portfolios range from 42.0% to 53.0% with residual allocations in TIPS and fixed income reducing their volatility. Equity exposures in the affluent, goals-based portfolios range from 53.0% to 89.0%, and the age 30 investors have the greatest exposure. Equity exposures in the portfolios of the middle-aged and retiring couples are considerably less than those in the without-goals portfolios, which range from 83.0% to 91.0%. Clearly, portfolios for those without goals are considerably more vulnerable to losses when equity returns fall below 4.8% for extended periods, leading to the likelihood that life goals will not be met.

Summary And Conclusion

In conclusion, the balance-sheet approach of matching a household's financial resources against liabilities for necessities or life goals appears to be a superior alternative to adopting more aggressive strategies in search of greater returns, irrespective of risk. The approach has the following advantages:

It provides a holistic view of investors' resources and goals, resulting in a more reliable asset allocation,

It results in portfolios that are resilient to market vagaries, which no one can accurately predict.

It quantifies a margin of safety to help assess a client's aversion to risk.

It accommodates a full spectrum of wealth levels and demographics tailored to specific clients.

It provides a coherent plan for investors to meet necessary and desired life goals.

C. Michael Carty is principal of New Millennium Advisors LLC, an investment advisor in New York City. The late Julia M. Carty was a marketing communications professional specializing in financial media, product and brand management, and research.