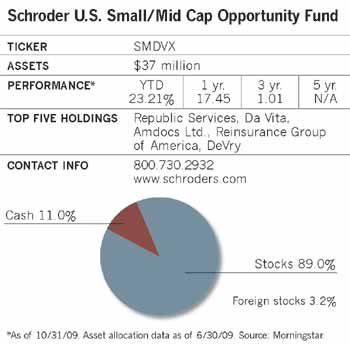

The beginnings of most bull markets are marked by a strong rally in lower-quality small company stocks, and this one has been no different, says Jenny Jones, who manages the Schroder U.S. Small/Mid Cap Equity Fund. But, she adds, investors who expect more of the same next year are likely to be disappointed.

"So far, the rally in small caps has been strongest among the tiniest, lowest-quality companies," she says. "While that's fairly typical coming out of the recession, I've been somewhat surprised by the strength and quickness of the move." According to her firm's research, stocks with the lowest public value rose an astounding 193% through the third quarter of 2009, while stocks of companies with no earnings have shot up 46%. By comparison, the Standard & Poor's 500 index was up 19.3% over the same period.

But Jones expects a shift as investors reassess the economy and take stock of market valuations. "If we are indeed in the midst of a recovery, then market leadership will likely shift toward higher-quality companies next year," she says.

The improvement in earnings that Jones anticipates from now through 2010, particularly in areas driven by improving consumer demand, could give stocks more running room. Some of that demand will likely come from dormant consumers whose portfolios are perking up again thanks to the stock market rebound. "The fact that the wealthiest 10% of consumers are feeling a lot better about their financial situation these days has been largely overlooked by both analysts and the media," she observes.

Although valuations are not nearly as attractive as they were at the market bottom in March, Jones believes that stocks "are not egregiously priced" based on long-term averages. At the same time, she is troubled by the rebound in commodity prices. Since stock and commodity returns typically go separate ways, rising commodity prices are usually not a good harbinger for equities.

Assuming the stock market rally stays on track, small-cap stocks should do well relative to large caps in the coming months, she says. Stocks of smaller companies typically race ahead for the first 12 to 18 months after the beginning of a market rally. Since the market appears to have hit bottom in March, their relative outperformance could persist over the next few months.

Jones is particularly enthusiastic about both large and small companies that derive a substantial portion of their revenues from exports, since they stand to benefit from what she believes will be a continued weakening of the U.S. dollar. Many of the companies in the portfolio, whose market capitalizations range from $750 million to $7 billion, fall into that category. "It's a common misperception that small- and mid-cap stocks benefit less from a weaker dollar than large caps," she says. "In fact, there is no evidence that a weak dollar leads to outperformance by large-company stocks."

Covering The Bases

To cover a range of different stock market scenarios, the fund's 70 to 90 holdings fall into one of three categories. The mispriced growth portion of the portfolio concentrates on stocks whose prices understate the growth potential of a company. These usually represent 50% to 60% of the fund's assets. While they tend to earn the highest returns for the fund in rising markets, they are less resilient in negative market environments. Steady eddies, which make up 20% to 50% of the fund, are companies with recurring revenues and strong cash flows. While their growth rates are typically not as high as those of the mispriced growth stocks, they tend to have more consistent earnings and hold up well in declining markets. Turnarounds, which account for up to 20% of fund assets, are stocks of companies that have suffered some type of misfortune but have a catalyst for improvement.

Their performance is less predictable than that of the other two groups relative to overall market conditions, but they can pep up performance if a turnaround materializes.

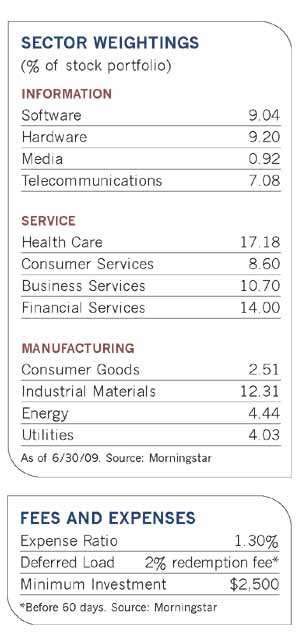

In addition to spreading its bets among stocks with different fundamental characteristics that prosper in different market cycles, the fund employs a number of other strategies that both smooth out returns and keep it at the more conservative end of the small/mid-cap investment spectrum. Each stock can account for no more than 5% of fund assets, and sector weightings can deviate no more than 10 percentage points from the weightings in the fund's benchmark, the Russell 2500 Index. Analysts set exit prices before purchasing a stock, though that target may change at some point, and maintain a typical holding period of between two and three years. The cash balance typically ranges from 5% to 10% of assets.

The proportional mix of categories at any given time reflects Jones' views of which companies will do well in a particular market environment. Throughout 2008, the percentage of the portfolio invested in steady eddies increased as consistency of earnings and high free cash flows trumped high growth as desirable attributes. One steady eddie company, Pactiv Corp., fell less in a declining market because of the consistent demand for its products, which include plastic containers for prepackaged meals and plastic trash bags. It also benefited from lower prices for oil, a component of plastic resins. Jones pared back the position this year as the stock reached its pricing target as part of an overall reduction in materials sector stocks from 10% of assets at the beginning of the year to 6% by the end of the third quarter. Energy was another area of interest earlier in the year. Jones used price drops to revisit names the fund held in 2008, but sold in the summer of that year as the stocks hit all-time highs and valuations became excessive.

In the spring of 2009, she began picking up bargains in mispriced growth stocks, which were selling at what she considered unusually attractive prices. Fund holding NBTY Inc. falls into this category. The company, better known as Nature's Bounty, manufactures and sells nutritional supplements, diet aids, sports nutrition products and vitamins under brand names such as GNC, Ester-C and Rexall. Jones says the firm's acquisition of U.K.-based Julian Graves, a chain of 350 food and confectionary stores, has helped expand NBTY's geographic reach and improve its profits. It recently traded at about $40 a share, somewhat lower than the fund's $55 target selling price.

DeVry, another component of the mispriced growth group, operates for-profit educational institutions around the country that focus on post-high-school career training. Although its enrollment numbers dropped a few years ago after the tech bubble burst and the school's tech-oriented curriculum subsequently became less attractive to prospective students, DeVry's new push into health care training has successfully boosted enrollment, revenues and profits. Jones points out that the school's graduates have higher employment rates than either high school or community college grads, despite the recession. And government funding should remain steady as President Obama continues to push for broader access to higher education.

At the end of the third quarter, stocks in the mispriced growth category accounted for 52.8% of the fund. Steady eddies weighed in at 43.7% and turnarounds at 4%. Now, as the bull market matures, Jones is moving money back into steady eddies. Many of these companies have not participated in the market rally as much as others even though they've done nothing wrong. But because they have lagged this year, their valuations are still relatively attractive, she says.

Burger King is a recent steady eddie addition to the portfolio. Five years ago, the company began a rigorous campaign to renovate its restaurants, diversify its menus and revamp its marketing strategy, which is helping it improve same-store sales and profit margins. Although higher unemployment and increased frugality have dissuaded consumers from eating out, the low-cost menu has proved appealing in tough economic times. Long-term franchisee royalties provide a steady stream of revenues, which stabilizes cash flow. The stock, which recently traded in the midteens, has a pricing target in the low 30s. At its current price, Jones estimates it is selling at just 11 times 2010 earnings.

Republic Services, the holding with the largest public value, made its fund debut in September. Republic's acquisition of Allied Waste earlier this year has helped the company realize significant cost savings, which proved critical as lower construction held down waste production. Republic, the second largest waste management firm after Waste Management, has been able to increase prices despite revenue declines and has a steady stream of business from regional contracts for waste disposal in areas with high population growth such as Las Vegas, California and Florida.