Derek Jeter, undoubtedly soon to be a first-ballot Hall of Famer, never forgot the fundamentals. Regardless of how many records he broke, of how many World Series rings he wore, and of how successful the New York Yankees were under his captaincy, Jeter routinely practiced baseball fundamentals during every spring training. He realized that success was based on mastering basic fundamentals.

It seems as though investors have forgotten about the basic fundamentals of investing. Metaphorically, they seem to be forgetting to cover first base on a grounder to the right side of the infield, to hit the cutoff man on an outfield throw, and to never pitch to a batter’s sweet spot on an 0-and-2 pitch.

The stock market is behaving exactly as fundamentals suggest it should, but investors’ recent range of emotions suggest they have taken their eye off the ball.

Profits Fundamentals

In 1995, I wrote a book called “Style Investing – Unique Insight into Equity Management”, which demonstrated the relationship between corporate profits and style rotation. Several conclusions from the book:

1. Profits cycles, not economic cycles, drive stock markets and style rotation.

2. Investors should focus on GAAP reported earnings because that definition of earnings skews analyses in investors’ favor. Other definitions of earnings hide important information.

3. There is typically a tug-of-war between interest rates and earnings. Rising interest rates are not a death knell for the stock market unless their negative effect is stronger than the positive effect of profits. Similarly, falling rates are not necessarily a boost to the stock market if earnings are too weak.

Twenty years later, investors still seem unaware of the book’s conclusions. Investors pay much more attention to GDP than to profits. A recent New York Times article pointed out the use and pitfalls of “adjusted” earningsі. General consensus is that the current bull market must end if the Fed raises rates.

Investors apparently have not learned the importance of practicing basic fundamentals, and continue to make the same infield errors. “Score that E6 for those of you keeping score at home.”

Earnings And Interest Rates

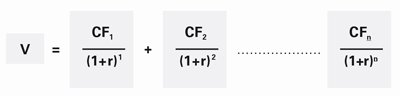

Basic finance says that there are two, and only two, variables that affect equity prices: earnings and interest rates. Consider the basic valuation formula for a stock:

Where,

V = value or price of a stock,

CF = dividends, earnings, or cash flows expected into the future,

r = interest rate used for comparison.

Consider all the variables to which investors pay attention that are not in that formula. Just to name a few, geopolitics, politics, GDP and other macroeconomic variables, and fund holdings may provide more noise and distraction than useful investment information if one doesn’t directly connect them to earnings and interest rates.

Of course, the formula incorporates a risk premium into the interest rate variable (i.e., a hurdle rate or required rate of return), but if one knew the correct risk premium for a security with certainty, then all other analyses would be superfluous because the reassessment of inaccurate risk premiums is basically what drives financial markets.

We pointed out last month, that a basic fundamental analysis of earnings and interest rates helps to explain why the stock market has recently gyrated. The Fed is “threatening” to tighten interest rates, while the US is in a profits recession. Within the context of the basic valuation formula, interest rates might rise while earnings forecasts are being revised downward. The numerator in the formula is going down, while the denominator is expected to soon increase.

If one thinks the Fed will wait to raise rates (as we do) and if one thinks that the profits cycle will trough by year-end 2015 (as we do), then it follows that 2016 might be a good year for US stocks. However, if one thinks the Fed will raise rates sooner and the profits cycle will trough later, then the basic formula suggests that stock market volatility could continue.

However, it all comes down to the basic fundamentals: earnings and interest rates.

Taking Grounders In Spring Training

Practicing basic fundamentals is critical to one’s success in any endeavor. In baseball, it means the mundane and repetitive task of taking ground balls in spring training. Successful baseball players are typically willing to go through the monotony in order to hone their skills.

Investors too often forget their practicing the fundamentals is critical to their success, too. For equities, it’s all about the basics of earnings and interest rates, and ignoring the ever present distractions. It isn’t very sexy to invest in equities using this commonplace approach, but no one gets to the Hall of Fame without mastering the basics.

© Copyright 2015 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $3.1 billion collectively under management and advisement as of September 30, 2015. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund, the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and the Eaton Vance Richard Bernstein Market Opportunities Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial Renaissance® ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS, Merrill Lynch, Morgan Stanley Smith Barney and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.