Nonfarm payrolls rose less than expected in August. Monthly changes have been uneven in recent months, which is consistent with the usual noise in the data, although the underlying trend appears to have slowed this year. Job growth should slow as the job market tightens, but how much slack remains in the job market? That’s an important question for Fed policymakers as they consider what to do in September.

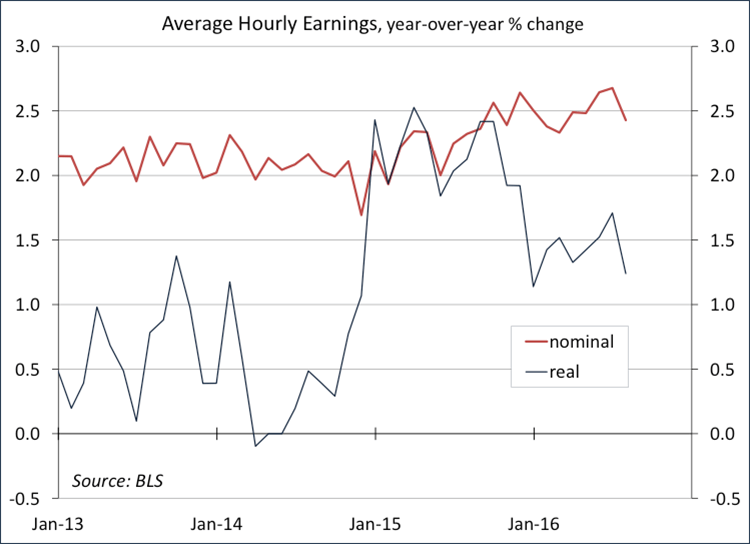

A tighter job market would normally lead to increased wages, and there are some signs of this in certain sectors (such as information technology), but wage growth has not picked up much. Luckily for consumers, inflation has remained low, leading to relatively strong gains in real hourly earnings.

For the Federal Reserve, the August employment data provide no easy answers – not strong enough to force the Fed to tighten, not weak enough to take a possible September move off the table. Slow productivity growth implies that the Fed should raise rates sooner than they would otherwise, but not by as much in total. Hence, the short-term hawkishness and long-term dovishness expressed in the last couple of weeks.

Scott J. Brown, Ph.D., is chief economist at Raymond James & Associates.

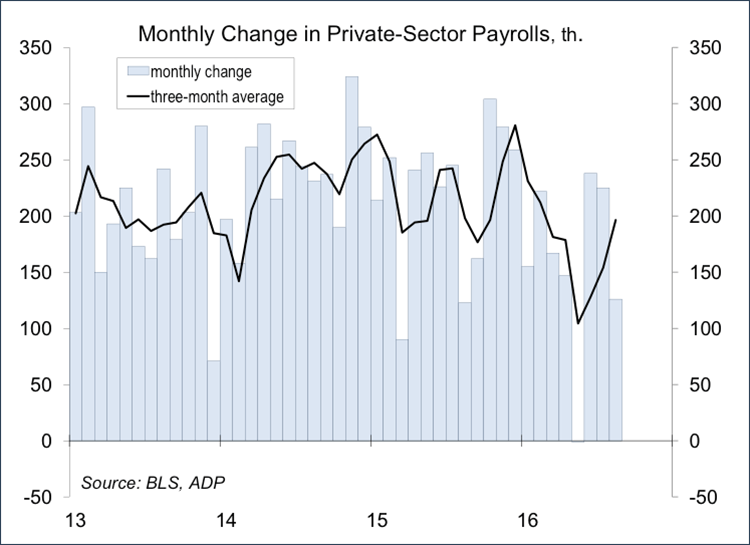

Private-sector payrolls averaged a 150,000 gain over the last six months, down from 221,000 in 2015 and 240,000 in 2014. Some of that slowing likely reflects greater business caution, particularly in the goods-producing industries, manufacturing and construction. Payrolls in service-producing industries have slowed somewhat, but remain relatively strong. Some slowing in job growth was expected this year as the job market tightens and firms find it more difficult to find qualified workers. Government jobs picked up in the last three months, mostly at the local level, and mostly in education (suggesting that there may be some issues with the seasonal adjustment).

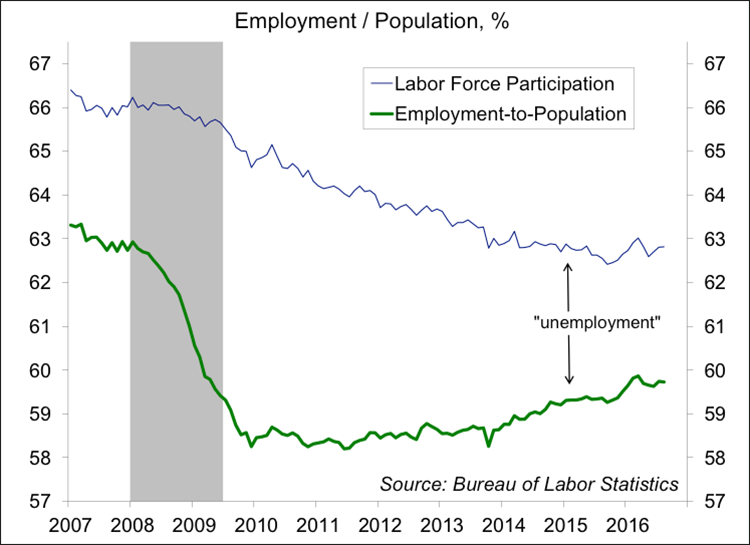

The unemployment rate held steady at 4.9% in August, down only modestly from a year ago. Normally, one would expect the unemployment rate to fall more slowly as the job market strengthens, as those on the sidelines (out of work but not officially classified as “unemployment”) are lured back into the workforce. However, labor force participation was also unchanged last month and up only slightly from a year ago. Clearly, recent retirees and stay-at-home spouse aren’t being lured back into the job market.

Last week, the government reported revised productivity figures for the second quarter. Labor productivity was revised lower, in line with expectations given the GDP data, but unit labor costs were revised sharply higher. Granted, quarterly figures tend to be erratic, but the underlying trend of slow productivity growth is disturbing. Unit labor costs, the key measure of inflation from labor, are trending at a faster pace. This should results in higher inflation (if firms can pass the higher labor costs along) or will eat into profit margins (if they can’t). At the very least, we can expect to see some adjustments in the overall economy, as some sectors will have to adapt over time.