Convertible securities have not been immune from the volatility that has roiled risk assets in 2016. However, we believe the volatile start to the year has set the stage for longer-term opportunities. A convertible bond can be thought of as a corporate bond (credit) with an embedded call option (equity). (For a primer on convertible valuation, please see our guide.) Because of its stock and bond characteristics, a convertible’s valuation can be influenced by forces in both the credit and equity markets, as well as by dynamics that are specific to the convertible market.

In this post, we’ll take a look at some factors that we believe can support convertibles going forward. More specifically, credit spreads have widened dramatically, equities have declined significantly, and convertible valuations have cheapened. A reversal in any one of these factors could provide a tailwind to convertibles, and if all three reverse, convertibles may be poised for a potentially powerful “trifecta.”

Convertibles can benefit from an eventual narrowing of spreads. Since the Federal Reserve began quantitative easing in 2008, the vast majority of convertibles have been issued by companies with below investment grade credit ratings. Only about 20% of the convertible market carries an investment grade rating and as a result, we’d expect performance in the convertible market to reflect what’s happening in the high yield market.

This most recent round of risk-off sentiment has taken a toll on the high yield asset class, with spreads topping 800 basis points over comparable U.S. Treasury bonds in February. As we noted in a recent high yield review, spreads have reached the 800 basis-point threshold just three times over the past 20 years: in the months following 9/11, in the midst of the financial crisis, and during the telecom meltdown. After reaching the 800 basis-point level, the one-year forward return from the initial month of crossing over was positive each time (4%, 8%, and 19% respectively).

Spreads have since narrowed to 782 basis points, and we expect continued narrowing as investors become more confident that a U.S. recession is not imminent. Inflation is low, unemployment is down, wages are rising, and the Fed has given every indication that it will remain patient in raising short-term interest rates. Alongside high-yield nonconvertible debt, we believe convertibles are poised to receive a boost as spreads tighten.

The underlying equities of convertibles could be positioned for a comeback, making the embedded option of convertibles more valuable. At its lowest point year-to-date (February 11), the BofA Merrill Lynch All U.S. Convertibles Index (VXA0) had fallen -10.56%. However, the underlying stocks in the VXA0 fell far more steeply, declining -19.89%. This difference is significant for a number of reasons. First, it indicates that the convertible structure is continuing to provide considerable relative downside resilience.

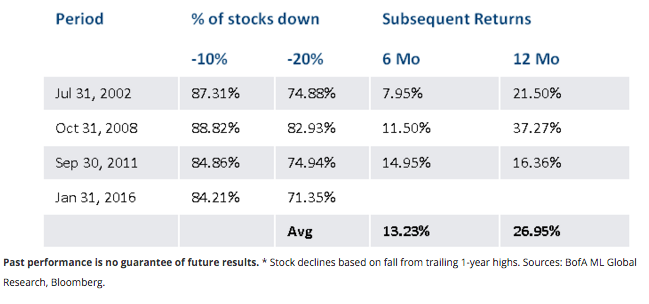

Second, this level of decline in the underlying stocks of the VXA0 has also been a precursor to healthy rebounds during the following six-month and 12-month periods. In its February 2016 global convertible research report, BofA Merrill Lynch noted that 71% of the VXA0’s underlying stocks have fallen more than 20% below their trailing 1-year highs. Since 1999, this has only happened three times (the 2002 tech bubble, the 2008 global financial crisis, and the 2011 European sovereign crisis/U.S. credit downgrade). In each of these periods, returns were positive for the subsequent six-month and 12-month periods (up an average of 13.23% and 26.95%, respectively).

AFTER STEEP DECLINES, THE UNDERLYING EQUITIES OF CONVERTIBLES HAVE TENDED TO POST SOLID RETURNS*

Convertible-securities-performance-after-steep-declines

Past performance is no guarantee of future results. * Stock declines based on fall from trailing 1-year highs. Sources: BofA ML Global Research, Bloomberg.

Convertible valuations are attractive. We can look at the theoretical fair value of a convertible bond as the sum of its bond and call option (the right to convert into the underlying stocks) components. In 2016’s risk-off environment of higher volatility, falling stocks and widening spreads, convertibles have been cheapening, according to BofA Merrill Lynch’s “% cheap” statistic, a measure of the relative valuation of the convertible universe. At the February 11 low, the convertible index was trading at 3.55 “% cheap,” a level reached only three times since 1995. And in each case, healthy returns followed. Of course, past performance can’t predict future results, but we believe this historical data is certainly worth noting—especially given our view that a U.S. recession is not imminent and that stocks may be able to stabilize near recent lows.